Global| Jul 21 2009

Global| Jul 21 2009Chicago Fed Index Indicates ThatEconomic Activity Improved Further

by:Tom Moeller

|in:Economy in Brief

Summary

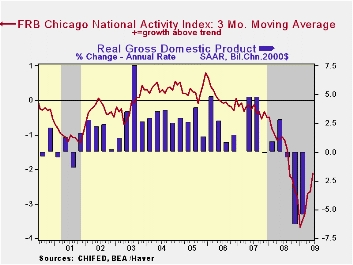

The Chicago Federal Reserve Bank reported that its June National Activity Index rose further to the highest level since July of last year. The reading of -1.80 was up from May and both figures were higher than the series' low of -3.99 [...]

The Chicago Federal Reserve Bank reported that its June

National Activity Index rose further to the highest level since July of

last year. The reading of -1.80 was up from May and both figures were

higher than the series' low of -3.99 reached this past January. Since

1970 there has been a 74% correlation between the level of the index

and the q/q change in real GDP.

The Chicago Federal Reserve Bank reported that its June

National Activity Index rose further to the highest level since July of

last year. The reading of -1.80 was up from May and both figures were

higher than the series' low of -3.99 reached this past January. Since

1970 there has been a 74% correlation between the level of the index

and the q/q change in real GDP.

The three-month moving average of the index also improved to its highest level since August.

An index level at or below -0.70 typically has indicated negative U.S. economic growth. A zero value of the CFNAI indicates that the economy is expanding at its historical trend rate of growth of roughly 3%. The complete CFNAI report is available here.

The production and income components made the largest positive contributions to the JUnel CFNAI. Twenty-two of the index components had a positive influence while 63 made a negative contribution.

The CFNAI is a weighted average of 85 indicators of economic

activity. The indicators reflect activity in the following categories:

production & income, the labor market, personal consumption

& housing, manufacturing & trade sales, and inventories

& orders.

The CFNAI is a weighted average of 85 indicators of economic

activity. The indicators reflect activity in the following categories:

production & income, the labor market, personal consumption

& housing, manufacturing & trade sales, and inventories

& orders.

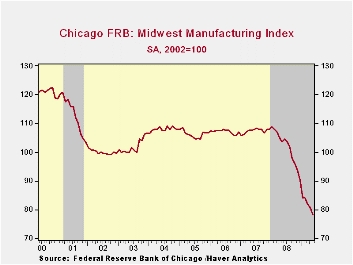

In a separate survey, the Chicago Fed indicated that its Midwest manufacturing index fell during May to its lowest level since 1994. Indicators for the auto, steel, and machinery each fell. The Chicago Federal Reserve figures are available in Haver's SURVEYS database.

Today's testimony by Fed Chairman Ben S. Bernanke is available here.

| Chicago Fed | June | May | June '08 | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| CFNAI | -1.80 | -2.30 | -0.98 | -1.76 | -0.35 | 0.05 |

| 3-Month Moving Average | -2.12 | -2.65 | -1.07 | -- | -- | -- |

by Tom Moeller July 21, 2009

Recession in the U.S. economy prompted a lower retail price

for gasoline last week. The pump price for regular gasoline fell

to an average $2.46 per gallon, down twenty-three cents from last

month's high. Nevertheless, prices remained up by eighty-five cents

(53%) from the December low. In the cash market, gasoline prices

yesterday continued to rally off last week's low. At $1.75 per gallon

the price was up from the low of $1.60. The figures are reported by the

U.S. Department of Energy and can be found in Haver's WEEKLY

& DAILY databases.

Crude oil prices also fell last week, but not by as much as gasoline costs. Light sweet crude oil prices (WTI) fell to $61.27 per barrel, off nearly ten dollars from last week's high of $70.83. Yesterday the one-month futures price for light sweet crude oil recovered and moved up to $63.98 per barrel. Prices had reached a daily high of $72.68.

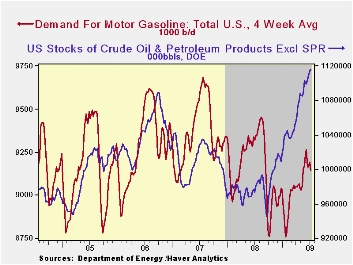

The ongoing recession lowered the demand for motor gasoline by 2.2% y/y during the last four weeks. The rate of decline has moderated from the 4.8% shortfall this past autumn. Demand for distillate also is off by a sharp 21.5% though residual fuel oil demand has moved higher. Finally, oil remains plentiful as evidenced by a 13.7% y/y rise in inventories of crude oil & petroleum products. The figures on crude oil inventories are available in Haver's OILWKLY database.

The weakening of natural gas prices stabilized last week at the seven-year low. Last week's average price of $3.28 per mmbtu (-70.8% y/y) was down by three-quarters from the high reached in early-July of $13.19/mmbtu.

| Weekly Prices | 07/20/09 | 07/13/09 | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Retail Regular Gasoline ($ per Gallon, Regular) | 2.46 | 2.53 | -39.4% | 3.25 | 2.80 | 2.57 |

| Light Sweet Crude Oil, WTI ($ per bbl.) | 61.27 | 61.48 | -54.7% | 100.16 | 72.25 | 66.12 |

by Tom Moeller July 21, 2009

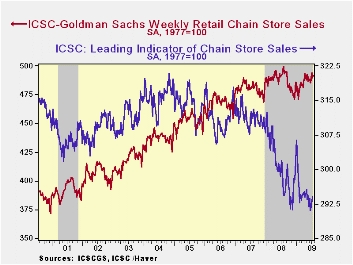

The strengthening of chain store sales around the July 4th holiday faded as the month progressed. During the latest week, chain store sales rose 0.5% but that recovered just half of the prior week's decline. So far in July sales have increased 0.7% since June after that month's 0.3% decline and a 0.2% May downtick.

During the last ten years there has been a 69% correlation between the year-to-year growth in chain store sales and the growth in general merchandise sales. The weekly figures are available in Haver's SURVEYW database.

The ICSC-Goldman Sachs retail chain-store sales index is constructed using the same-store sales (stores open for one year) reported by 78 stores of seven retailers: Dayton Hudson, Federated, Kmart, May, J.C. Penney, Sears and Wal-Mart.

Prospects for improvement in sales seems limited. The leading indicator of sales ticked up 0.3% (-2.4% y/y) during the latest week and it has been flat-to-lower all this year.

Exit Strategies for the Federal Reserve from the Federal Reserve Bank of St. Louis can be found here.

| ICSC-UBS (SA, 1977=100) | 07/18/09 | 07/11/09 | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|

| Total Weekly Chain Store Sales | 491.7 | 489.4 | -0.3% | 1.4% | 2.8% | 3.3% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.