Global| Jan 10 2006

Global| Jan 10 2006Chain Store Sales: A Firm Start to the New Year

by:Tom Moeller

|in:Economy in Brief

Summary

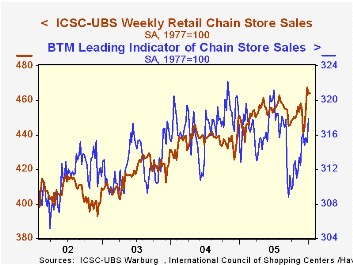

Chain store sales rose a slight 0.1% to open the new year according to the International Council of Shopping Centers (ICSC)-UBS survey. The up tick followed a 0.8% decline during the closing week of 2005. Solid increases earlier in [...]

Chain store sales rose a slight 0.1% to open the new year according to the International Council of Shopping Centers (ICSC)-UBS survey. The up tick followed a 0.8% decline during the closing week of 2005.

Solid increases earlier in December followed a very weak start to the month. As a result, sales in December fell 0.3% m/m but January sales started 2.2% above the prior month.

During the last ten years there has been a 51% correlation between the y/y change in chain store sales and the change in non-auto retail sales less gasoline, as published by the US Census Department. Chain store sales correspond directly with roughly 14% of non-auto retail sales less gasoline.

The leading indicator of chain store sales jumped 0.9% in the latest week and pulled December average up 0.2% from November.The ICSC-UBS retail chain-store sales index is constructed using the same-store sales (stores open for one year) reported by 78 stores of seven retailers: Dayton Hudson, Federated, Kmart, May, J.C. Penney, Sears and Wal-Mart.

Now is the Time to Strengthen Our Economic Foundation from Federal Reserve of Atlanta Bank President Jack Guynn is available here.

| ICSC-UBS (SA, 1977=100) | 01/07/06 | 12/31/05 | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Total Weekly Chain Store Sales | 464.3 | 464.0 | 3.7% | 3.6% | 4.7% | 2.9% |

by Tom Moeller January 10, 2006

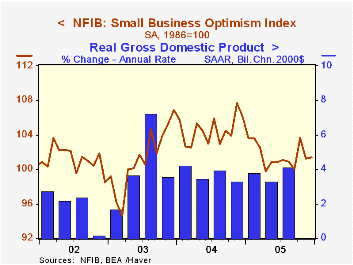

The index of small business optimism from the National Federation of Independent Business (NFIB) in December recovered a marginal 0.2% of the prior month's 2.4% drop. For the fourth quarter as a whole, optimism did improve 1.4% from 3Q but sharp declines early in the year pulled the 2005 levels down 2.8% from averaged during 2004, the first annual drop since 2001.

The marginal m/m improvement reflected fewer firms (22%) firms with one or more job openings and fewer firms (21%) expecting higher real sales in six months offset by slightly more expecting the economy to improve and slightly more expecting higher earnings.

During the last ten years there has been a 70% correlation between the level of the NFIB index and the two quarter change in real GDP.

The percentage of firms planning to raise average selling prices backup off sharply from the November high to 27%. The percentage of firms actually raising average selling prices also fell sharply to 18%. During the last ten years there has been a 60% correlation between the change in the producer price index and the level of the NFIB price index.

About 24 million businesses exist in the United States. Small business creates 80% of all new jobs in America.

The latest press release from the NFIB is available here.

The National Economy and Monetary Policy in the New Year from Kansas City Federal Reserve Bank President Thomas H. Hoenig can be found here.

| Nat'l Federation of Independent Business | Dec | Nov | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Small Business Optimism Index (1986=100) | 101.4 | 101.2 | -4.4% | 101.6 | 104.6 | 101.3 |

by Tom Moeller January 10, 2006

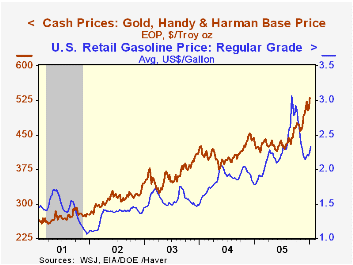

The rise yesterday in gold prices to $540 per ounce was to a level not attained in twenty five years. It underscored several concerns over the potential for future inflationary price pressure including 1) speculation of an end to Fed tightening with GDP growth strengthening worldwide, 2) the coming change in leadership at the Fed and 3) still high energy prices, up one third to one half from last year.

Gasoline prices rose nine cents last week to a retail average $2.33 per gallon. Yesterday, the strength diminished somewhat as the spot price for regular unleaded gas fell a nickel.

Earlier declines in gasoline prices fostered a sharp rebound in petroleum demand. In December, motor gasoline demand is estimated up 5.7% from a year earlier and in the latest week up up 16.7%.

International Transmission of Inflation Among G-7 Countries: A Data Determined VAR Analysis is available here.

| Weekly Prices | 01/09/06 | 01/02/06 | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| US Retail Gasoline Price (per gallon) | $2.33 | $2.24 | 29.8% | $2.27 | $1.85 | $1.56 |

| Gold: Handy & Harmon, $ per Troy Oz. | $541.5 | $530.0 | 28.9% | $444.7 | $409.2 | $363.13 |

by Louise Curley January 10, 2006

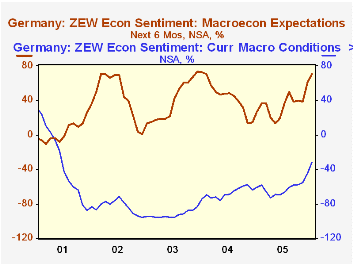

After a sharp rise in confidence among institutional investors and analysts in Germany last month, confidence increased meaningfully again in January. The excess of optimists over pessimists expecting improved conditions over the next six months is now 71%. 9.4 percentage points above December, 2005, 44.1 points above January 2005 and the highest excess since January, 2004. The investors and analysts also became less pessimistic regarding current conditions. Although pessimists still exceed optimists in appraising current conditions by 31.6% in January, the excess of pessimists was 12.8% less than that of December, 2005 and 29.6% less than that of January, 2005 and well below the extreme pessimism of the first half of 2003 when the excess of pessimists averaged around 95%. The percent balances for expectations and current conditions in the German economy are shown in the first chart.

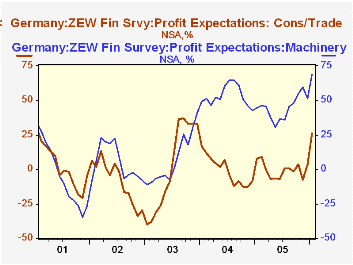

In its survey of investors and analysts, ZEW research also asks for opinions on profit expectations in a wide variety of industries. The results are expressed as the percent balance of those expecting increases over those expecting decreases. In the latest survey, the excess of those expecting increases over those expecting decreases varied from 68.7% for machinery to 3.4% for construction. The second chart shows profit expectations for the machinery and the consumption/trade industries. Expectations for rising profits have been strong for the machinery industry since Mid 2003 while those for the consumption/trade industry have been poor. The sharp rise in the excess of those expecting an increase over those expecting a decrease in the profits of the consumption/trade industry in January to 25.9% from 3.5 % last December is particularly encouraging.

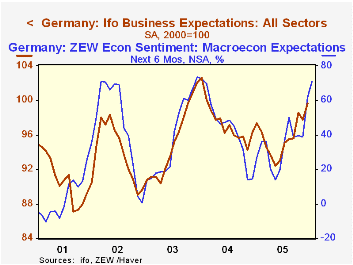

As shown in the third chart the ZEW measure of confidence, which is based on a small sample of some 300 investors and analysts, frequently anticipates the results of the broader IFO measure which is based on replies from some 7000 firms engaged in manufacturing, construction, wholesaling and retailing. The IFO index is scheduled to be release on January 25.

| Jan 06 | Dec 05 | Jan 05 | M/M Dif | Y/Y Dif | 2005 | 2004 | 2003 | |

|---|---|---|---|---|---|---|---|---|

| ZEW Investor Confidence Measure (% Balance) Exports | ||||||||

| Current Conditions | -31.6 | -44.4 | -61.2 | 12.8 | 29.6 | -61.8 | -67.7 | -92.6 |

| Expectation 6 Months Ahead | 71.0 | 61.6 | 26.9 | 9.4 | 44.1 | 34.8 | 44.6 | 38.4 |

| Profit Expectations | ||||||||

| Machinery | 68.7 | 51.0 | 44.4 | 17.7 | 23.3 | 44.7 | 53.4 | 7.0 |

| Consumption/Trade | 25.9 | 3.5 | 7.8 | 22.4 | 18.1 | -0.4 | -0.8 | 2.2 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief