Global| Jun 22 2021

Global| Jun 22 2021CBI Orders Continue to Accelerate

Summary

The Confederation of British Industry (CBI) survey for the U.K. had another strong showing in June with the net orders reading climbing to +19 from +17 in May. Orders have progressed from averaging -23 over 12 months to averaging -7 [...]

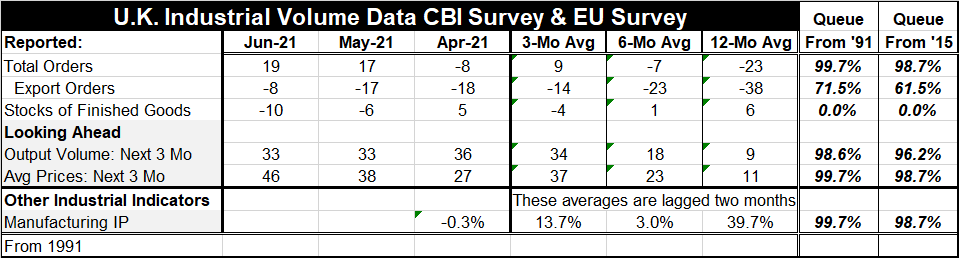

The Confederation of British Industry (CBI) survey for the U.K. had another strong showing in June with the net orders reading climbing to +19 from +17 in May. Orders have progressed from averaging -23 over 12 months to averaging -7 over six months and to averaging +9 over three months, and then this month orders steps up to a reading of +19 in June. On data back to 1991, this is a top 0.3 percentile standing (it has been this high or higher only 0.3% of the time). From 2015, it is a top 1.3 percentile standing. On either timeline, this is a very strong reading; in fact, it is the strongest reading on both timelines with the percentile standing differences due only to the difference in the number of observations in each period.

The Confederation of British Industry (CBI) survey for the U.K. had another strong showing in June with the net orders reading climbing to +19 from +17 in May. Orders have progressed from averaging -23 over 12 months to averaging -7 over six months and to averaging +9 over three months, and then this month orders steps up to a reading of +19 in June. On data back to 1991, this is a top 0.3 percentile standing (it has been this high or higher only 0.3% of the time). From 2015, it is a top 1.3 percentile standing. On either timeline, this is a very strong reading; in fact, it is the strongest reading on both timelines with the percentile standing differences due only to the difference in the number of observations in each period.

Strong Growth

The U.K. economy is coming back after being bottled up in reaction to the virus and its many manifestations of re-spreading. Right now the U.K. is exceptionally strong and its fiscal borrowing and deficit for May came in below expectations. Public sector net borrowing decreased to GBP 24.33 billion in May from GBP 43.76 billion in the previous year. The deficit was also below forecasts. These things typically happen when the economy is stronger than expected; it is generally because of greater than expected tax revenues.

Covid-19 Progress

U.K. Covid-19 infections are on a slight upswing but are still low. Deaths from Covid-19 are very low and as of June 21 were as low as 5 on the day a very low reading. There were however 10,633 new infections. Some still fear that the U.K. could be at risk to a third wave from the Delta variant. The Delta variant, also known as B1.617.2, is thought to be between 30-100% more transmissible than the Alpha variant, also known as B.1.1.7. Currently, about 99% of the new cases in the UK are thought to be the Delta variant. However, it is estimated that over 85% of adults in the U.K. have antibodies against the coronavirus (Source here).

Survey Strength

U.K. export orders are improving as well as overall orders as they improved sharply to a negative reading of -8 in June from -17 in May and those compare to a 12-month average at -38. Export orders have a firm 71.5 percentile standing on data back to 1991.

Meanwhile, with orders ramped up, it is not surprising to find inventories extremely lean, falling to -10 in June from -6 in May and with their lowest standing ever on both timelines.

Looking ahead, expected output volume at a reading of +33 is unchanged month-to-month and just below its reading of +36 in April. The expected output reading jumped to +30 in March from +2 in February and has since stayed in that same very high range. The reading this month has a 98.6 percentile standing on data from 1991 forward.

Average price pressures also are expected to step up. The June reading rose to +46 from +38 in May and that was up from +27 in April. Price expectations jumped to +20 in March from +3 in February, rising in unison with output expectations. Prices also have a reading that clings to the top of the range just like for volume expectations.

Comparing the CBI survey data to hard data we have, the last manufacturing IP reading at -0.3% month-to-month was as of April. Manufacturing IP has a 13.7 annualized pace of growth over three months and a 3% annualized pace over six months. The year-on-year gain is very strong because of the weak year ago comparison; manufacturing IP is up by 39.7% and has a very high percentile standing on its gain over 12 months. But the three-month and six-month data already hint at some slowing down for IP data even though the survey report from the CBI remains extremely strong. The economy is still reopening and IP data are two months less up-to-date than the survey reports themselves. Maybe the U.K. economy is accelerating again and the IP data have yet to show it....

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief