Global| Jul 17 2014

Global| Jul 17 2014Car Registrations Back off in Europe and Raise Questions

Summary

Car registrations in Europe fell by 4.2% in June after a 1.4% decline in May. Over three months registrations are falling at a 4.2% annual rate, over six months they are falling at an 8.8% annual rate and over 12 months they are [...]

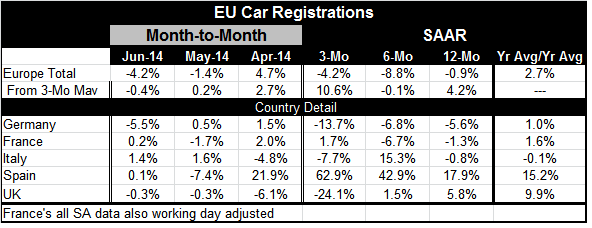

Car registrations in Europe fell by 4.2% in June after a 1.4% decline in May. Over three months registrations are falling at a 4.2% annual rate, over six months they are falling at an 8.8% annual rate and over 12 months they are falling at a 0.9% annual rate.

Car registrations in Europe fell by 4.2% in June after a 1.4% decline in May. Over three months registrations are falling at a 4.2% annual rate, over six months they are falling at an 8.8% annual rate and over 12 months they are falling at a 0.9% annual rate.

These growth statistics tell a pessimistic story of the path of European car sales. However, the chart would suggest that sales may still be in a very shallow uptrend, albeit at levels of registrations that are far below historic standards. However, the chart is also consistent with a more pessimistic reading.

In Germany, sales fell sharply in June, dropping by 5.5% and plunging the three-month annualized growth rate, to -13.7%. Germany now has a set of sequential growth rates that indicate a clear deteriorating trend.

In France, registrations grew by 0.2% in June after a 1.7% decrease in May. France has a three-month annualized growth rate that is positive at 1.7%. That growth rate upends what was a developing and deteriorating trend for car registrations over six months and 12 months. Still, it does not clarify the path of future registrations in France.

In Italy, sales grew by 1.4% in June after a 1.6% advance in May. Still, over three months registrations in Italy are falling at a 7.7% annual rate. That's worse than its -0.8% rate over 12 months. However, the six-month growth rate for Italy is positive at 15.3%. Italy's trends are therefore convoluted and their future path is unclear.

In Spain, the fourth largest euro area economy, registrations grew by 0.1% in June after a 7.4% decrease in May. Still, because of a huge surge in April, the three-month annualized growth rate for registrations in Spain is 62.9%. The six-month growth rate is 42.9% and the 12-month growth rate is 17.9%. Spain is clearly an exception to these other European trends. Its performance is exceptional. The key is that after registrations jumped in April, they held most of that ground with only moderate backtracking.

The United Kingdom has had strong auto registrations throughout this recovery, but recently registrations have become very volatile. Sales fell by 0.3% in June, the same as it May. Due to a sharp drop in April, the three-month annualized growth rate for the UK is at -24.1%. Still, the six-month growth rate for the UK is a positive 1.5% and over 12 months UK registrations are up by 5.8%.

It's hard to put a very positive spin on the car registration data for Europe. All countries except Spain exhibit a great deal of weakness in registrations and in trends at some point in recent months. The weakness in car registrations goes hand-in-hand with other signs of weakness that we have seen, stemming from industrial output to consumer confidence to industrial sentiment across all euro area countries. Car registrations are another dataset warning us about the potential for a growth slowdown in Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief