Global| Apr 27 2007

Global| Apr 27 2007Can’t Tell a Book - or GDP – by its Cover, or Headline

Summary

GDP growth surprised on the slow side for 2007Q1 coming in at a pace of 1.3%. The Yr/yr pace slowed, too, to 2.1% a sharp slowdown from 3.1% Y/Y just last quarter. Despite the low growth print of the headline, GDP was anything but [...]

GDP growth ‘surprised’ on the slow side for 2007Q1 coming in at a pace of 1.3%. The Yr/yr pace slowed, too, to 2.1% a sharp slowdown from 3.1% Y/Y just last quarter.

Despite the low growth print of the headline, GDP was anything but weak. Consumer spending came in with a gain of 3.8% quite strong and in the 25th%-tile of all its contributions to GDP growth since 1980. With consumer spending running hard at 3.8% it would be difficult to believe that to boost GDP the Fed would want to cut rates and spur even stronger spending. As it is, the rate of unemployment is falling. Now the issue for GDP is that, for the moment, there are some special subtractions in play that are keeping real spending growth in the various GDP sectors from hitting the bottom line. It is these subtractions we need to turn our attention to.

The subtractions from GDP in Q1 were not a surprise. Residential structures took nearly one percentage point from GDP growth by itself. As large as this is for such a small sector of the economy (only 4.5% of GDP) it was its smallest subtraction by this beleaguered sector in three quarters. It is obviously too small to continue to have this sort of outsized impact on GDP. Since the sector is only 4.5% of GDP it could only subtract a percentage point from GDP growth for four years in a row before it would be reduced itself to only 0.5% of GDP itself. Housing cannot and will not continue to be such a negative.

While housings weakness could spill over to in other ways it seems that people’s tendency to rely on home equity increases to support spending have been exaggerated, this according to a new study Alan Greenspan had a hand in. With the upward revisions to U of M Consumer sentiment on Friday (4/27/07) the erosion in consumer attitudes seems to have been stabilized as well. Spill over form housing no longer seems to be such a risk.

Also subtracting from GDP are inventories. They have subtracted from growth in five of the past eight quarters. But this is their weakest rise in six quarters. Inventories have already done a lot of their adjusting or so it seems especially With consumption so strong, surely this sort of inventory paring won’t go on for long.

The ongoing subtraction from GDP is GDP net exports. They have contributed positively to growth in only six quarters (out of 29 quarters) since the end of 1999. The net export drain is a persistent drain on US product and on US incomes. The other drains are temporary or cyclical in nature. For this reason and more the net export drain is particularly troublesome. Despite a very weak dollar (read ‘a highly competitive dollar’) and reported strong growth in Europe and in China US exports FELL in 2007-Q1. Generally what happens to the trade account is that US imports are strong due to strong US growth and they outpace exports. But this quarter US imports are weak due to weak US growth and exports fell pushing the deficit up. It does not make sense for US exports to be so weak and to me, at least, this is the most troubling aspect of this GDP report.

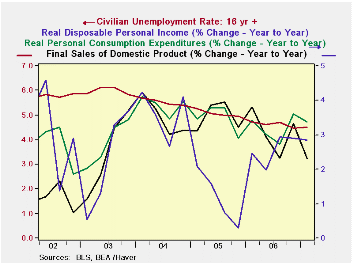

The chart above shows several measures of US domestic activity in GDP. We show real consumer spending (PCE) and the consumer income that support such spending (real disposable personal income). We also plot final sales of domestic products. As an overlay on this mapping we chart the unemployment rate that continues to fall. Very clearly US activity- however you define it- is strong enough to drive the rate of unemployment lower. This is the main reason why despite evidence of a slowing in GDP the Fed will not want to touch stimulus with a ten foot pole.

We have been through the accounting of GDP and see the measures that account for most of the GDP slippage. We can tell that there are certain leakages that relate to certain problems or issues in the economy. We can even assess some of them to be temporary. But we cannot deny the impact they had on GDP in the quarter. Despite the slowdown in GDP we find there is growing wage pressure and dropping unemployment. While the Fed is not comfortable with GDP growth slowing and certainly is quite uncomfortable with GDP at 1.3% (annualized) – even for one quarter - it can see that the economy, despite its weak headline, is growing quite fast enough. This GDP report helps to explain the Fed’s dilemma like nothing else could. Despite the slowing in GDP and the low growth rate, inflation pressures are worsening and the rate of unemployment is dropping. What is the Fed supposed to do about all that? It’s not supposed to happen that way. Note: Stagflation

This GDP report has prompted some to raise of the specter of stagflation. Is this what stagflation is? Stagflation may be a difficult topic to wrap your brain around, but we can answer this question with some degree of clarity.

NO! and on the other hand…NO! –that’s just be clear about it.

People who are calling this stagflation are confused.

While it may seem like stagflation with the GDP growth rate falling and inflation rising stagflation is not really about rising inflation and slowing growth (even though the name says Stag-flation). Instead stagflation is about stubbornly high inflation and insufficient growth.

For stagflation, inflation need not be accelerating; it just needs to be ‘high.’ Growth need not be decelerating; it simply needs to be insufficient’.

The US economy may be losing steam and it may have slowed but growth is NOT insufficient. Corporate profits are doing well and DJIA has just made a series of all-time record highs. Other market indices are on 6-yr highs plus the RATE OF UNEMPLOYMENT is low and has been falling.

When unemployment starts to rise and inflation is stubbornly high or rising we can open this question of stagflation. But let me say this: I have seen stagflation and this is not stagflation.

As for inflation, inflation may be rising, and it may be above the Fed’s comfort zone, but it is hardly high.

The problem with branding this as stagflation is that we have NO ‘stag’ at all and very little ‘flation’.

| PCE | Services | Goods | Non Residential Structure | Residential Structure | Equipment % Software |

Inventory | Net Exports | Government | |

| Q1-07 | 2.66 | 1.51 | 1.15 | 0.07 | -0.97 | 0.14 | -0.30 | -0.52 | 0.18 |

| GDP Growth | 2006 Q1 | 2006 Q2 | 2006 Q3 | 2006 Q4 | 2007 Q1 | Current |

| Actual/A,P,F | Actual | Actual | Actual | Actual | Advance | Yr/Yr |

| Real GDP | 5.6% | 2.6% | 2.0% | 2.5% | 1.3% | 2.1% |

| PCE | 4.8% | 2.6% | 2.8% | 4.2% | 3.8% | 3.4% |

| Durables | 19.8% | -0.1% | 6.4% | 4.4% | 7.3% | 4.5% |

| Nondurables | 5.9% | 1.4% | 1.5% | 5.9% | 2.9% | 2.9% |

| Services | 1.6% | 3.7% | 2.8% | 3.4% | 3.7% | 3.4% |

| Business Invst. | 13.7% | 4.4% | 10.0% | -3.1% | 2.0% | 3.2% |

| Structures | 8.8% | 20.3% | 15.7% | 0.9% | 2.1% | 9.4% |

| Equipment | 15.6% | -1.4% | 7.7% | -4.8% | 1.9% | 0.8% |

| Housing | -0.3% | -11.1% | -18.6% | -19.8% | -17.0% | -16.7% |

| Inventories ($B)* | $41.2 | $53.7 | $55.4 | $22.4 | $14.8 | $31.8 |

| Farm | $4.3 | $1.9 | $2.5 | $2.4 | $3.0 | $1.2 |

| Nonfarm | $36.8 | $52.2 | $53.3 | $20.0 | $11.3 | ($45.2) |

| Net Exports ($B)** | ($636.6) | ($624.2) | ($628.8) | ($582.6) | ($597.8) | $38.8 |

| Exports | 14.0% | 6.2% | 6.8% | 10.6% | -1.2% | 5.5% |

| Imports | 9.1% | 1.4% | 5.6% | -2.6% | 2.3% | 1.6% |

| Government | 4.9% | 0.8% | 1.7% | 3.4% | 0.9% | 1.7% |

| Real Final Sales | 5.6% | 2.1% | 1.9% | 3.7% | 1.6% | 2.3% |

| For Yr/Yr: * average, ** Change from Yr ago Qtr | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief