Global| Sep 18 2020

Global| Sep 18 2020Canadian Retail Sales Get Back All Recession Losses Then Some

Summary

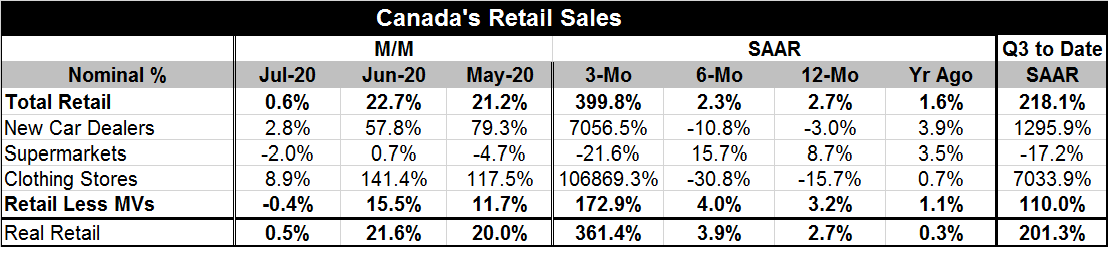

Canadian retail sales rose by 0.6% in July, a striking deceleration from their gains of 22.7% in June and 21.2% in May. Sales are now back to and above their pre-covid-19 levels; that virus that caused substantial backtracking in the [...]

Canadian retail sales rose by 0.6% in July, a striking deceleration from their gains of 22.7% in June and 21.2% in May. Sales are now back to and above their pre-covid-19 levels; that virus that caused substantial backtracking in the economy.

Canadian retail sales rose by 0.6% in July, a striking deceleration from their gains of 22.7% in June and 21.2% in May. Sales are now back to and above their pre-covid-19 levels; that virus that caused substantial backtracking in the economy.

Sales levels overall for retail less motor vehicle sales and real retail sales surpass their pre-recession levels of sales in July. Sales at new car dealers, supermarkets and clothing stress are still short of their pre-recession sales levels. New car dealer sales are still lower than their pre-recession levels by 5.5%. Supermarket sales are 16% below their pre-recession peak level. Clothing sales still lag their pre-recession levels by 17%. So while sales overall have made a ‘full recovery' various sectors continue to suffer from some fallout, but the overall sales performance has recovered.

The story of recovery is one of an uneven rebound and that is not just a Canadian story; it's a global story. Certain sectors are going to struggle more than others and there will be distributional consequences.

Canada shows some of the same signs we have seen in the U.S. but also some differences. The three-month growth rates in July are very strong; some of them are growth rates in the thousands in terms of percentage changes. But supermarket sales are a clear exception as food sales have been in the U.S. The pandemic that caused people to be shuttered and stay home coincided with the closing of restaurants and with more home consumption of food boosting supermarket sales when other sales economy-wide were diving. So in the recovery phase sales are going back to normal levels and that is causing – has caused supermarket sales – to decline in July as well as in May. They are net lower over three months while all other sectors have sales at explosive levels.

In the U.S., sales fell over 12 months and six months for most categories then surged over three months. Canada shows sales rising over 12 months overall and for supermarkets and for retail excluding motor vehicles and for real retail sales. Over six months, total sales supermarket sales, retail less motor vehicle and real retail sales also rise unlike the U.S. case. These suggest lesser disruptions overall in Canada than those experienced in the U.S. where sales declined more broadly over six months and 12 months then responded with huge three-month rates of growth.

Canada's quarter-to-date growth rates also show strong and super strong growth compared to Q2 levels with supermarket sales as the lone exception. The recovery appears to be occurring apace, despite the slower growth overall in July.

Canada's July slowdown is abrupt. Retail sales excluding motor vehicles even declined in July with the push higher to overall sales coming from motor vehicles themselves as new car dealer sales rose on the month by 2.8%. Clothing sales are ‘slowing' but still up at the otherwise extremely strong monthly growth rate of 8.9%. Even the much slower 0.6% month-to-month gain in overall sales corresponds to an annualized gain of 7.4%. On balance, Canadian retail sales appear to be in a solid recovery mode and hopefully the recovery will spread to other sectors not separately enumerated here. There are many economic sectors that remain challenged in the wake of the virus that is still lurking and circulating. As long as there is a fear of infection and the virus lurks, it will be an issue for growth at least until a workable vaccine is able to be distributed.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief