Global| Jul 18 2014

Global| Jul 18 2014Canadian Inflation Ticks Higher; What Does It Say About the U.S.?

Summary

No man is an island; nor is any country (except in some cases literally). And even though the U.S. is geographically separated from most of its trading partners by large distances, it is influenced by events in their economies. But no [...]

No man is an island; nor is any country (except in some cases literally). And even though the U.S. is geographically separated from most of its trading partners by large distances, it is influenced by events in their economies. But no country influences the U.S. more than Canada which is by far the largest U.S. trading partner and shares a long unguarded border with it.

No man is an island; nor is any country (except in some cases literally). And even though the U.S. is geographically separated from most of its trading partners by large distances, it is influenced by events in their economies. But no country influences the U.S. more than Canada which is by far the largest U.S. trading partner and shares a long unguarded border with it.

Canadian inflation is on the rise. U.S. inflation is on the rise (Sorry Janet) and those are trends that markets will have to confront the same as they are now confronting an ugly geopolitical reality that they for long have tried to brush aside and wish away. If wishes were jobs, people would be employed and we would have world peace.

Economic problems are not brushed aside without consequence.

Generally, economic problems get worse when not promptly attended. Fed Chair Janet Yellen, when she speaks to us publically, she says the right things about policy being `data dependent.' But policy has been conducted for some time with a blind eye to the consequence of stronger growth (a fast dropping unemployment rate) and rising inflation (both the CPI and the Fed's targeted PCE deflator). But how long can the Fed keep ignoring forces that should be pushing it to be less accommodative?

The Fed is ignoring the direction (and speed) of economic progress for the sake of its targets that are expressed as levels of variables not as changes. At least there once was an unemployment rate that the Fed cited in some one-off fashion, but policy was not tied to it. The actual unemployment rate fell so sharply after the Fed set its unemployment gauge, that the Fed's unemployment (non-)policy variable was quickly shunted aside. Now the Fed only says that it looks at a collection of labor market variables. But it has a long-term objective for the headline PCE of 2%. The PCE right now is at 1.8%, hardly leaving the Fed a lot of breathing room. And given our ability to forecast, for all intents and purposes, the actual inflation rate is tailgating the Fed's objective. One would not expect the Fed to be using the same logic and tactics with the unemployment rate so much lower (still too high!) and the inflation rate drafting the Fed's target. But it is; it does.

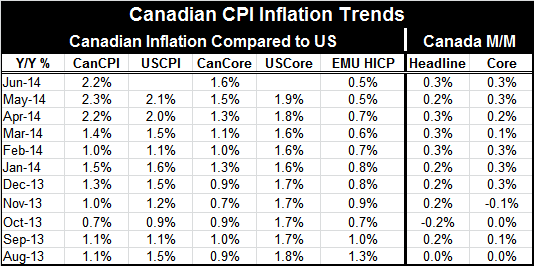

The U.S. CPI is related to the Canadian CPI with an R-squared value of 0.68. The U.S. CPI is related to the European HICP with an R-squared value of 0.72. Both of these are strong relationships. Canada's inflation pressure is going up, while Europe's is going down. But then, IMF Managing Director Christine Lagarde warned today that markets might be too optimistic about Europe. She said that Europe is still recovering, however, not raising fears of backsliding. But there you have the reason for weaker European inflation: it's weak growth. Meanwhile, in the U.S., growth seems to have taken hold more firmly. Both the U.S. and Canada have energy development plays underpinning growth.

The U.S. should be mindful of trends in its neighbor to the North. The U.S. and Canada share business cycles (and inflation cycles) very closely. U.S. and Canadian inflation rates are closely connected even when they differ. Yes, Canada is a different economy with some of its own unique features, but in the big picture the U.S. and Canada are all but joined at the hip.

James Bullard, St. Louis Fed President, is warning that if growth is stronger the Fed may have to raise rates sooner. While that is not controversial, Bullard says it's because he thinks it is going to happen- that part is controversial. We can be sure that when the Fed shifts to start to hike rates, there will be no such thing as a measured pace in the markets' reactions. Every bond manager that has not had a lobotomy will know what to do. Neutral is a long way from where the Fed funds rate currently resides. And that Fed shift will weigh heavily on all markets including the U.S stock market that has poked its head above the clouds. The transition from low rates supporting high P/Es to strong earnings supporting them may not be a smooth one. We warn of more volatile days ahead and urge keeping an eye on our neighbor to the North for some additional clues. Watching inflation may become more important than watching for growth.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief