Global| Jun 17 2016

Global| Jun 17 2016Canadian Inflation: Alone in the Sweet-Spot

Summary

Inflation globally is low. In the EMU, the price level is falling. Japan's inflation is weak. In the U.S., the CPI is up only 1.1% although the U.S. targets the PCE deflator which shows a much weaker core trend than the CPI. In [...]

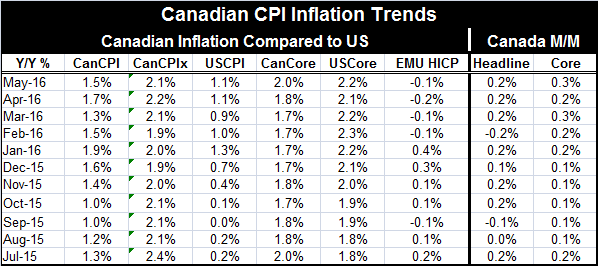

Inflation globally is low. In the EMU, the price level is falling. Japan's inflation is weak. In the U.S., the CPI is up only 1.1% although the U.S. targets the PCE deflator which shows a much weaker core trend than the CPI. In Canada, inflation has a 2% target midpoint and has stayed for the most part in the 1% to 3% range that the Bank of Canada has prescribed. The BOC also has a less volatile index with eight `rogue' components extracted called the CPIx which continues to expand very much along the midpoint of its guidelines and has been consistent in recent years in staying within its broader range.

Inflation globally is low. In the EMU, the price level is falling. Japan's inflation is weak. In the U.S., the CPI is up only 1.1% although the U.S. targets the PCE deflator which shows a much weaker core trend than the CPI. In Canada, inflation has a 2% target midpoint and has stayed for the most part in the 1% to 3% range that the Bank of Canada has prescribed. The BOC also has a less volatile index with eight `rogue' components extracted called the CPIx which continues to expand very much along the midpoint of its guidelines and has been consistent in recent years in staying within its broader range.

This range and midpoint approach seems to be much more effective than the policy in the EMU where a little below 2% apparently allows the German to call -0.1% inflation moderate and want to be content while other EMU members gnash their teeth over it and worry about deflation. After all, what is a little below 2% as a target? We know that a little below 2% is a much larger distance for the Germans than `a little above it,' and that asymmetry is a problem for policy-making in the EMU.

In the U.S., policy can't seem to get a grip on what it wants to do. Year-to-date calculations on the PCE and core PCE that go back for all sequential 12-month periods over the last 25-years (yes, 25-years, long before this target was adopted!) all show that U.S. PCE and core PCE inflation has stayed below 2% on both gauges for all those 25-or-less year-to-date horizons. Yet, until very recently the FOMC wanted to have a higher Fed funds rate on the belief that inflation was rising to its goal. The Fed claimed it was convinced that inflation would be on a path to 2% over the (ill-specified) medium term. But now of course it does not seem to believe that anymore.

Economists everywhere will like the Fed's advanced approach of looking ahead and using sophisticated forecast techniques and complex models to ascertain the right fine-tuning for policy today. That is, they will like the idea until they look at the forecasting track record. The BOC diagnostic approach seems far superior to the Fed's forward-looking approach. With inflation in a 1% to 3% band, there is warning when the rate deviates from the center and approaches one edge of the band or the other and time for policy to react. On this broad, two-percentage-point wide target, the BOC has plenty of room to be right whereas the Fed and ECB objectives leave a razor thin margin for `right' and a large area in which to have knock-down drag-out disagreements about `wrong.'

Even though Canada is a natural resource dependent economy and its economy should be subject to considerable shocks as commodity prices oscillate as they have in this business cycle, the BOC's CPIx rate has really only been outside this two-percentage-point band once since in late-2002 (that was in late-2002). There is no evidence here that having a broad target obstructs monetary policy in any way. It seems a far better way to do things than the way policy targeting has been done in the U.S. and EMU.

Having said that, there is nothing in the adoption of such a technique that would guarantee that inflation would stay in that band. However, the point is that, with inflation still well below 2% if it were at 1% or close to it the central bank could argue that it was making its progress- sort of like being in the first cut just off the fairway- not quite in the rough. The existence of the CPIx, especially constructed for this purpose, has been to help reduce volatility. This is far better than to have Janet Yellen simply wave her arms about how the inflation gauge is distorted because of rising or falling oil prices. It also has been really helpful since using the CPIx has eliminated 8 of 9 episodes of inflation being outside the preferred range for Canada. That is a great filter. The filter not only enhances the central bank credibility but it calms markets and increases the notion that the central bank knows what it is doing and has control as well. Maybe the Fed and ECB should consider broadening their objectives and recalibrating an intermediate inflation gauge with enhanced stability properties. It seems to be working up north.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief