Global| Mar 20 2015

Global| Mar 20 2015Canadian Inflation; A Study in Contrast

Summary

Inflation in Canada continues weak, crawling along the bottom of the range established by the Bank of Canada. The central bank has a desired inflation in a range of 1% to 3% but also expects that inflation will drop below 1% for much [...]

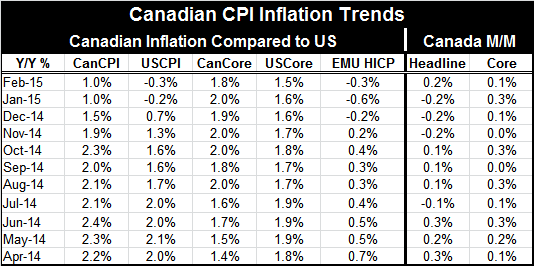

Inflation in Canada continues weak, crawling along the bottom of the range established by the Bank of Canada. The central bank has a desired inflation in a range of 1% to 3% but also expects that inflation will drop below 1% for much of the year. Falling energy prices are the same old story here and in the short run there's nothing to do but wait it out.

Inflation in Canada continues weak, crawling along the bottom of the range established by the Bank of Canada. The central bank has a desired inflation in a range of 1% to 3% but also expects that inflation will drop below 1% for much of the year. Falling energy prices are the same old story here and in the short run there's nothing to do but wait it out.

We are in a period of controlled inflation. For the United States, Canada and EMU inflation rates for core and headline inflation measures are below 2% over the last five years and 10 years on a cumulative basis as well as more recently. The central bank of Canada has an inflation range making its 1% core performance more in line with the inflation facts of late. The ECB targets only headline inflation so its -0.3% pace constitutes a big miss from its target of 2%. Moreover, the ECB has been missing persistently with year-over-year headline inflation below 2% for 25 months in a row. That's two years of missing with the degree of the miss increasing. In the U.S., the Fed offers forecasts of the PCE and of the core PCE. Its guidance is in terms of the headline inflation rate, but the Fed, somewhat confusingly, will make references to both measures. But with the Fed focused on a rate of 2% and the PCE headline rising by only 0.2%, the Fed has a major shortfall to deal with. Even the core PCE is up by only 1.1% year-over-year.

While we can debate the merits of differing inflation targeting programs, in this instance the Bank of Canada seems a lot more relaxed and in step with its goals. Having a range for inflation gives it flexibility and it can decide to react to inflation inside the zone or not as well as how to deal with out-of-the-range variations. I know some will see adopting a range for inflation as `soft', but in reality it all depends on how the central bank enforces the program.

For now the Bank of Canada is in its sweet spot but only at the edge of it. Since the energy price drop is seen as a special or temporary phenomenon, it can be given some slack.

However, in Europe the inflation shortfall is more severe for political reasons. This is a target short fall in currency union where some members are shocked and hurt by such low inflation (think Mediterranean members) while others (think Germans) are quite willing to just let it play out. Of course, the German economy is a low inflation economy geared to perform in this climate. Greece, Spain, Portugal, Italy and the like are not so constructed. Because of the growth-inflation linkage, these members want inflation boosted and want stimulus policies adopted to help hit the price target. In the EMU, this is very much a political question with various members having differing positions and with the adoption and enforcement of austerity rules acting as another important motivating factor for some members to expect the central bank to at least hit its target instead of adding monetary squeezing to fiscal squeezing.

For the U.S., it is much less clear how all this is playing out. The U.S. central bank unlike Europe's does not have only an inflation objective. While the Fed does make guesses at growth rates for GDP, it does not target GDP but it does make forecasts for the unemployment rate that come into play a bit more in the policy discussion. On this score, the U.S. unemployment rate has dropped very sharply, and while U.S. growth is better than growth in Europe, it is still not satisfactory. Indeed, U.S. job growth has picked up much more than GDP growth and this disconnect is now part of the policy discussion. The Fed is confronted with an unemployment rate that is looking low -almost too low- by historic standards and according to what had been recent policy judgements. Yet inflation both core and headline continue to fall. The only way to describe Fed policy is to admit that it has been `moving the goal posts.' Or, if you like this analogy better, it is like the famous Three-Stooges skit where they keep drawing a line in the sand and challenging the bully to cross it. Each time he does cross it, so they draw another until they finally run away. Well, the Fed is not yet running away. But it has drawn and erased lines below which it did not think the unemployment rate would fall. The Fed is really at odds in trying to understand economic performance. One of its policy metrics is telling it to slow down on the easing and to tap the brake, while the other is telling it to go full speed ahead.

We cannot be surprised that a central bank with two bosses winds up with contradictory orders. However, in the case of the Fed, the contradiction has been there for some time and yet the Fed has not resolved how to deal with it. For the moment, the Fed rhetoric is about how it won't tighten until it is sure inflation is on a 2% path. But inflation is still falling and the economy continues to tighten up. Still, there are NO SIGNS of economic overheating. Recent economic data have begun to back track, yet Fed rhetoric is all about how it is going to tighten. There is no mistaking what the Fed wants to do or which of its signals has become its master. Yet the other is still a constraint. There is no clear reason for the Fed to hike rates other than its growing impatience. The Fed is in fact talking about one policy objective (inflation) while reacting to a totally different policy fear. I find this schizophrenic behavior.

For now, despite what are highly similar inflation results, we are seeing very different monetary policies being implemented and considered in the near future in the U.S., Canada and the EMU. This may give us a chance eventually to decide which of these approaches works best.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief