Global| Sep 18 2018

Global| Sep 18 2018Canadian Factory Sector Looks Solid

Summary

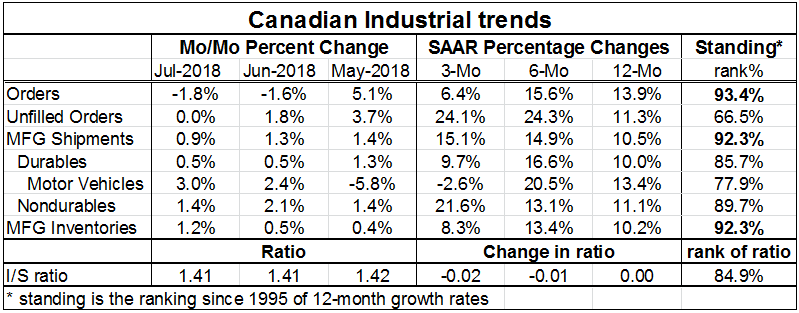

Canadian factory orders fell for the second month in a row in July but because of an order surge back in May the three-month growth rate continues to record a solid 6.4% rate of growth. Unfilled orders were flat in July but had risen [...]

Canadian factory orders fell for the second month in a row in July but because of an order surge back in May the three-month growth rate continues to record a solid 6.4% rate of growth. Unfilled orders were flat in July but had risen in each of the five previous months. Shipments increased in July but slowed from their previous pace, rising by 0.9% on the month a weaker gain than their 1.3% rise in June. Shipments have been rising for three months in a row and rose in five of the last six months.

Canadian factory orders fell for the second month in a row in July but because of an order surge back in May the three-month growth rate continues to record a solid 6.4% rate of growth. Unfilled orders were flat in July but had risen in each of the five previous months. Shipments increased in July but slowed from their previous pace, rising by 0.9% on the month a weaker gain than their 1.3% rise in June. Shipments have been rising for three months in a row and rose in five of the last six months.

The break down for durable and nondurable goods shows strength for both. Motor vehicles show very strong gains in the last two months but these are insufficient to compensate for a sharp drop in shipments in May. The pattern for motor vehicle shipments is the reverse of the pattern for total orders over the last three months.

Sequential growth rates

The sequential growth rates refer to the pattern of growth in the table from twelve-months to six-months to three-months. On that profile order growth is strong over twelve- and six-months then the growth rate dips over three-months. Unfilled orders show an 11% gain over twelve months; from there annualized gains of 24% over six-months and three-months show a step up. Shipments show acceleration from a ten percent pace over twelve-months to a fifteen percent pace over three-months. Durable goods show weaker shipments over three-months for durables overall as well as for motor vehicles (which notch an actual fall over three-months) but there is no clear pattern of deceleration for either of these series. On the other hand, nondurable goods show steady acceleration in shipments from twelve-months to six-months to three-months. All in all it’s a pretty solid report, not without its blemishes, but a solid report.

Inventories

Over this horizon inventories have continued to grow although they have slowed their pace over three months after having accelerated a bit over six months. Inventories to sales ratios are relatively stable; they have fallen a bit over three-months and six-months but are unchanged over twelve-months.

Standings

The ranking of these industrial metrics shows a high standing for the year-on-year growth of orders, shipments and inventories. Each of these post rankings that place their twelve-month growth rate in the top ten percentile of their historic growth rate queue of values since 1995. Unfilled orders with a still-solid ranking in its 66th percentile are the weakest measure in the table.

Risks

On the whole, the industrial sector where data always oscillate seems to show solid growth. Of course, there still are cross border issues with the US so it pays to keep an eye on these trends. But so far the only hint of any weakness comes from the motor vehicle sector.

The economy

The Canadian economy is performing well. Housing starts are softer but could also be described as moving more or less sideways despite some uptick in five year mortgage rates. Employment continues to grow steadily and the ranks of the unemployed continue to diminish as the unemployment rate itself holds steady. Manufacturing output in real terms has slowed slightly and slowed progressively from twelve-months to six months- to three-months. Canada’s leading economic index is flat over twelve-months lower over six-months and up at a nearly 2% pace over three-months. That is less than a full vote of confidence in the future. Retail sales have slowed in both in real and in nominal terms, but at 3.4% over three-months, the pace of real retail sales is still solid. Among retail sales, industrial output and the jobs market, Canadian data seem on quite solid footing with question marks only raised in some of the ancillary reports, and optimism mitigated by a minor slowing trends among these three key sectors.

Policy

Canadian inflation like inflation in the US has been firm but not so clearly excessive. However, the solid performance of the economy may cause central banking officials to believe that another rate hike is either warranted or could easily be tolerated by the economy. This would be understandable based on the new factory sector report of today. BOC governor Poloz has viewed the inflation rise as a temporary uptick. But the more that inflation stays at or near the border line of its policy objective with growth looking solid, the more likely a rate hike becomes. Canada is entering that situation. Just because central bankers see a rise in inflation as ‘temporary’ does not mean they are necessarily willing to sit back and do nothing to see if they are right. Also it is September and the Federal Reserve in the US is expected to raise rates again this month. If the BOC does not join in, exchange rate pressure could develop and exacerbate whatever inflation issues may currently exist.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief