Global| May 04 2021

Global| May 04 2021Canada's Trade Balance Ends Its Brief Flirtation With Surplus

Summary

On its trade account, Canada has logged six monthly surpluses in the last six and one-quarter years. In March, the trade data are coming off a string of two surpluses in a row. Despite the surplus rarity, Canada's surpluses have [...]

On its trade account, Canada has logged six monthly surpluses in the last six and one-quarter years. In March, the trade data are coming off a string of two surpluses in a row. Despite the surplus rarity, Canada's surpluses have tended to cluster together.

On its trade account, Canada has logged six monthly surpluses in the last six and one-quarter years. In March, the trade data are coming off a string of two surpluses in a row. Despite the surplus rarity, Canada's surpluses have tended to cluster together.

Export and import prices

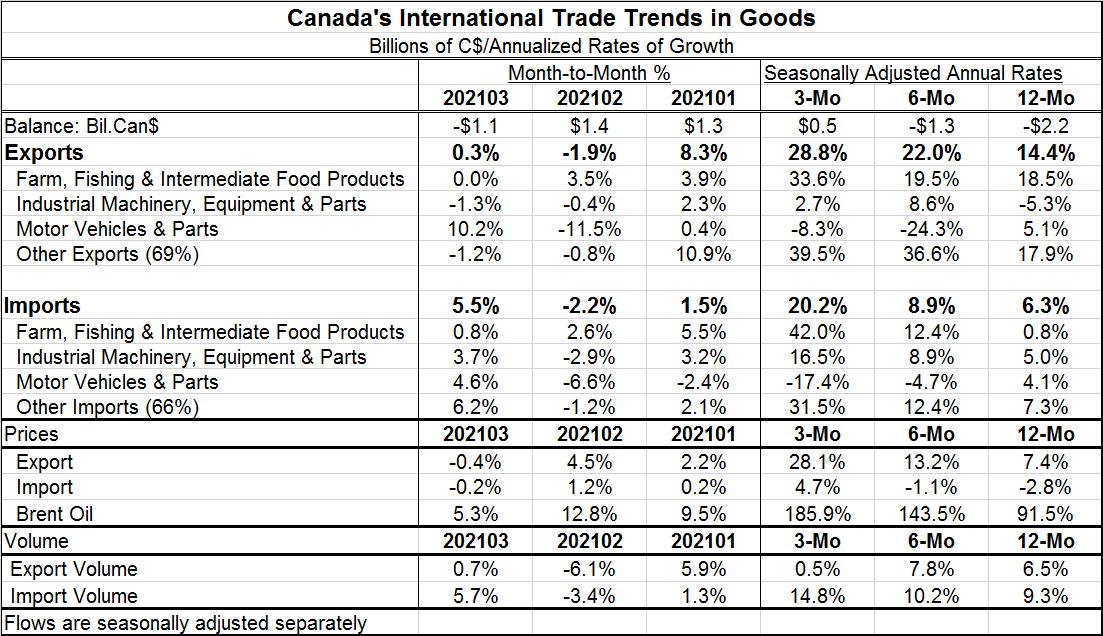

One factor that pushed Canada's trade balance to surplus in the past two months was export prices. Export prices that are up by 7.4% over 12 months, rose at a 28.1% annualized rate over the past three months. During those same two periods, import prices fell by 2.8% over 12 months and rose at a moderate 4.7% annualized rate over the last three months.

Prices and volumes interact

Of course, prices can really affect export and import values over the short turn. Over the longer run, the impact of prices on changes in value depend on what economists call price ‘elasticities.' If a good is very ‘price elastic' it means potential buyers are price sensitive so that if prices go sharply higher purchases will slow or even decline. Price effects can be either quick in affecting trade flows or may take time depending on the product as well as on export and import contracts. Canada saw its export volumes rise by 6.5% over 12 months then slow to an annualized pace of 0.5% over three months as export prices rose sharply. On the other hand, imports whose volume rose by 9.3% over 12 months saw import volumes step up over three months, advancing at a 14.8% annual rate as import prices continued to rise at a moderate pace. Of course, the impact on trade values from price and volume effects work out simultaneously and we see the net effect embedded in the value growth figures reported previously as well as below.

Export and import value trends

Canada's export values gathered momentum rising at a 14.4% pace over 12 months, rising at a 22% pace over six months and to a 28.8% pace over three months annualized. Imports also gathered pace rising by 6.3% over 12 months with its annualized growth rate rising to 8.9% over six months and then to 20.2% over three months.

Exports and imports by month

Monthly exports outpaced imports 8.3% to 1.5% in January. By February the export advantage was reduced as both flows backed off and as exports fell by -1.9% and imports fell a touch faster at -2.2%. In March, the worm turned as imports surged, rising by 5.5%, as exports nudged ahead rising by just 0.3%.

The commodity composition of trade

Both exports and imports saw a steady acceleration of trade flows on both sides (exports and imports) for farm and fishing goods. Industrial machinery exports fell over 12 months but have been rising on balance over both three months and six months. On the import side, industrial machinery imports have been gathering pace steadily from 12-months to six-months to three-months. Exports and imports of motor vehicles & parts show escalating declines on the import side against exports where growth turned negative but without any clear intensifying momentum beyond that. The categories ‘other' exports and ‘other' imports absorb about two-thirds of trade in the case of each flow; that dominates trends for both export and import flows. Other exports grow at a pace of 17.9% over 12 months, but that pace was doubled over both six months and three months. For imports, the catch-all category saw growth of 7.3% over 12 months with slower but steady acceleration to 12.4% over six months and onward to 31.5% over three months. ‘Other imports' are up by 6.2% in March compared to its export counterpart category that shows the flow falling by 1.2% on the month.

Summing up

Globally trade flows have been picking up as economies have recovered. We see that in Canadian flows as well. Trends in motor vehicles are the exception to the general trend. But those flows are substantially between the U.S. and Canada and are governed by the U.S.-Canada auto trade agreement in addition to macroeconomic circumstances. For now the U.S., a very important export market, is growing very fast especially over the past two months. U.S. auto buying has stepped up as stimulus monies have been doled out by the federal government. But car production at the same time has been hampered by a chip shortage. That may cause trade in vehicles to continue to forge its own trend in the future. Still, the major trend we see here is revival as both exports and imports have come to life despite the ongoing presence of the virus as well as in the face of chip shortage issues.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief