Global| May 14 2021

Global| May 14 2021Canada's Orders Rebound As Does the Economy

Summary

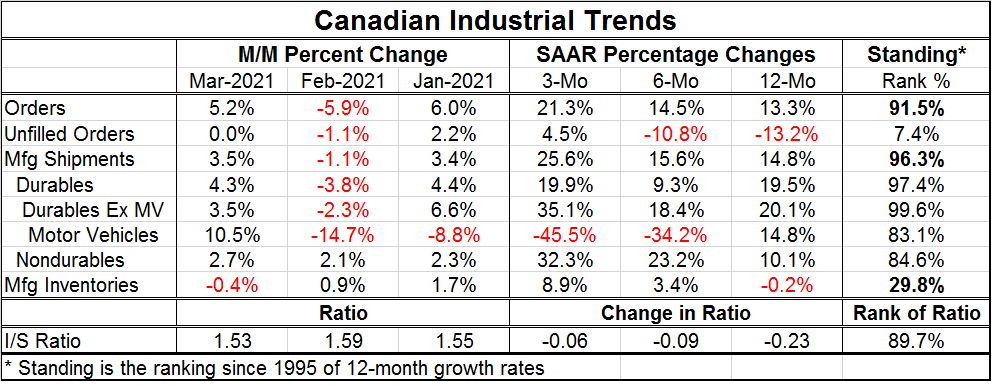

After plunging in February, Canada's orders recouped and gained back most of those losses in one month rising by 5.2% in March. Despite what is clearly still a great deal of volatility, Canadian orders are accelerating their rate of [...]

After plunging in February, Canada's orders recouped and gained back most of those losses in one month rising by 5.2% in March. Despite what is clearly still a great deal of volatility, Canadian orders are accelerating their rate of growth from 12-months to six-months to three-months. Unfilled orders manufacturers' shipments, and inventories also accelerate on this timeline. Nondurable goods shipments accelerate on this timeline as motor vehicle shipment growth rates decelerate. Motor vehicles are in the grip of a chip shortage. Durable goods and durables excluding motor vehicles show less clear trends but removing motor vehicles leaves the durables growth rates at a point where they are close to signaling steady acceleration as well.

After plunging in February, Canada's orders recouped and gained back most of those losses in one month rising by 5.2% in March. Despite what is clearly still a great deal of volatility, Canadian orders are accelerating their rate of growth from 12-months to six-months to three-months. Unfilled orders manufacturers' shipments, and inventories also accelerate on this timeline. Nondurable goods shipments accelerate on this timeline as motor vehicle shipment growth rates decelerate. Motor vehicles are in the grip of a chip shortage. Durable goods and durables excluding motor vehicles show less clear trends but removing motor vehicles leaves the durables growth rates at a point where they are close to signaling steady acceleration as well.

All the orders and shipment series have rankings that sit in the top 10th percentile to top 20th percentile based on a ranking of year-on-year rates of growth. However, unfilled orders rank in their lower 7.4 percentile and inventories rank in their 29.8 percentile. With such strength in the sector, such weak backlogs and low inventories may not make as much sense. But what this dataset seems to capture at a point in time is orders jumping and shipments flying out the door at a time that supply chains do not permit order replenishment for a restocking of goods sold. So far, shipments seem to be keeping up with orders; but those growth rates are neck-in-neck. Still, the inventory situation is not anywhere near critical as the inventory-to-sales ratio sits at its 89.7 percentile. Inventories are still relatively abundant relative to sales.

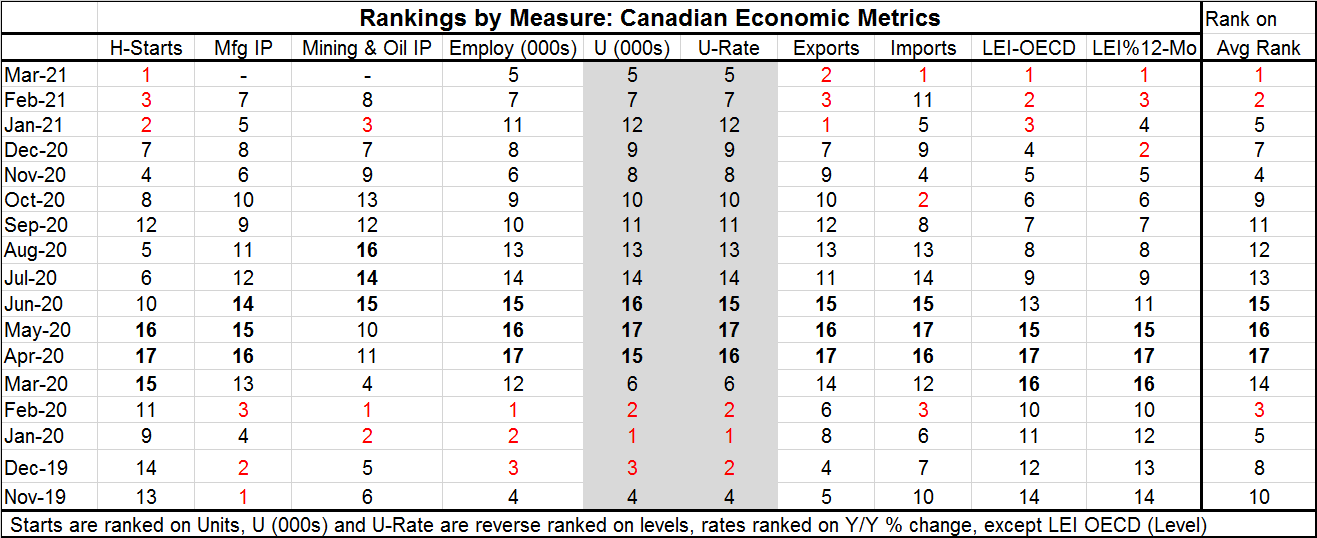

The table below takes a snapshot of sorts of the breadth of the Canadian economy to see where it stands. The far-right had column is a re-ranked average of all rankings in the table. On that basis, March and February are, across the sweep of reporting sectors, among very the best the economy has seen in the last 17 months.

The unemployment data are reverse-ranked so that their ranking values accord with economic rank in of other sectors where low rankings indicate strong data. This treatment puts the labor market metrics on the same cycle as for other metrics in the table.

What we see here is a Canadian economy that was doing fairly well ahead of the impact of the virus. At that time, it had an overall ranking of 3 and 5 in January and February ahead of impact of the virus. And it was improving from its weaker November-December readings.

Then the virus struck...

Next we see April, May and June rankings slide to their lows in most cases; for mining, the lows came a bit later…

But now Canada is seeing its best housing starts, its strongest imports and over the last three months its strongest exports. As for signaling, the highest LEI value as well as the highest LEI growth rate over the last 17 months is also being generated.

Revival in train

Canada has revival in train. The industrial sector is no surprise since we see that sector in recovery globally. But here in this aggregate table we also see other aspects of the economy coming back to life. However, it is also true that the level of the unemployment rate and the number unemployed are still not back to their past lows the unemployment lows are still November 2019 through February 2020. But both of these labor market metrics are up to their fifth best (fifth lowest, number of unemployed and unemployment rate) standings in March. That is a big jump from ranking 7th in February and 12th in January of this year. The job market is not back the way much of the rest of the economy is, but it is on its way and it has momentum.

Snapshot of Canada's Economy

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief