Global| Nov 17 2020

Global| Nov 17 2020Canada's Housing Starts Rise As Recovery Stays on Track

Summary

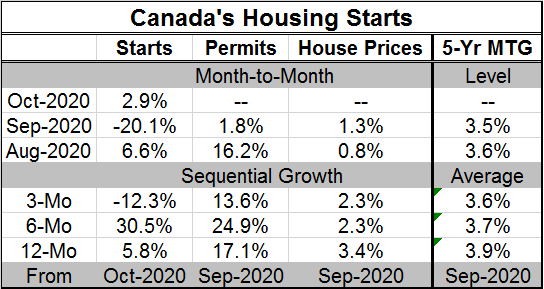

Housing starts in Canada rose in October after a sharp drop in September when multi-unit activity backed off sharply. The increase in starts is attributed to single-detached urban starts which dominated some slight weakness in urban [...]

Housing starts in Canada rose in October after a sharp drop in September when multi-unit activity backed off sharply. The increase in starts is attributed to single-detached urban starts which dominated some slight weakness in urban multiple-starts. Mortgage rates in Canada continue to be low and attractive. Overall activity in Canada continues to advance and also continues to lag behind year-ago levels. For the most part, recovery from the virus is an ongoing task. Housing seems to be in step with other macroeconomic trends in those respects.

Housing starts in Canada rose in October after a sharp drop in September when multi-unit activity backed off sharply. The increase in starts is attributed to single-detached urban starts which dominated some slight weakness in urban multiple-starts. Mortgage rates in Canada continue to be low and attractive. Overall activity in Canada continues to advance and also continues to lag behind year-ago levels. For the most part, recovery from the virus is an ongoing task. Housing seems to be in step with other macroeconomic trends in those respects.

Near-term growth and progress remain the order of the day despite a virus that is spreading again and will likely hold back activity in the months ahead.

Starts and unemployment

In February, Canadian unemployment was at 5.6%. It moved up to 7.8% in March and to 13% in April and to its cycle high reading of 13.7% in May. Since then, the labor market has been under repair and unemployment has fallen back to 9% in September from 10.2% in August. During this period, housing starts more or less tracked with the national unemployment results suggesting that the impact of Covid-19 dominated both measures. The unemployment rate peak came in May while housing was at its low point just a month earlier. Unemployment progressed to lower levels through October while housing starts reached a recovery peak in August, backed off in September and got back on the growth path in October. Housing starts have been more volatile that employment/unemployment, but they have generally tracked lower and higher together.

However, the virus is on an expanding path again in Canada and in many places it is changing the living preferences of people and affecting where they want to live and the kind of unit they want to occupy. All of this catches the home-building industry in mid stride with projects already on the books.

The Covid-19 update

As of November 16, the number of total Coronavirus cases in Canada is 302,192 – that represents a doubling from the number in late-September. New daily virus cases have shot up to stand at 6,115 on November 16, well above even the spike-high of 2,760 back on May 3 of this year during height of the ‘first wave.' The number of active cases is also rising very sharply – doubling from late October. However, the silver lining in all this grim news is that, despite the spread of infection, the death toll is much less than half of its worst under the first wave and even lower looking at averaged statistics. The virus is spreading but has not been as lethal. Still, policymakers are wary and people are for the most part modifying behavior to try to stay virus free. Canada, like everyone else, is back in the virus soup. For some, it is hotter than for others

The combination of the spread and of people's reaction will, of course, damp economic data. In some ways, the housing industry might be less affected because building is an activity that takes place out of doors making it a relatively safe Covid-19 activity. But house-buying in a pandemic may bring a lot of factors into play that could either speed up home buying decisions or slow them down. This includes the loss of income and the large presence of unemployment. Canada sets Covid-19 policy province by province and for that reason has had some uneven results.

An industry comparison

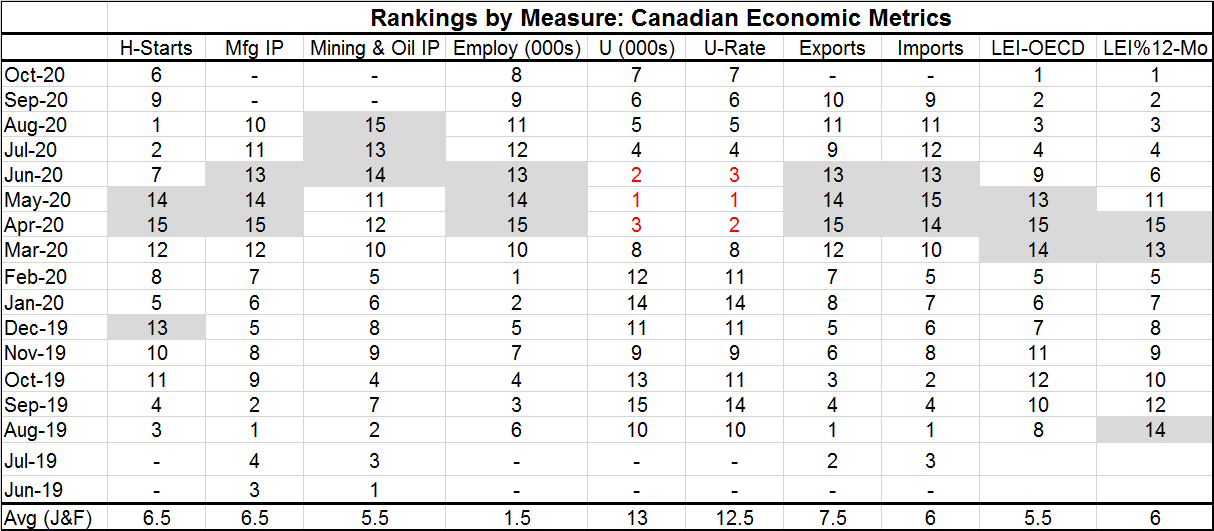

Given the challenges it has faced, the housing sector appears to be healthy, at least as healthy as other parts of the economy that are also dealing with the same problems. The table below ranks each of these metrics (high to low; High value = rank of one) against the most recent 15 observations for each. The time periods vary slightly because of data reporting lags. What we find is a clear clustering of low rankings (high number) from April to June when the virus hit hardest as the first wave. This finding holds except for the unemployment data where high rankings (low numbers) are bad events. For the unemployment data, we see ranks of 1, 2 and 3 represented in April, May and June. Interestingly, the leading economic index data, arrayed either by LEI level or by year-on-year percentage change, show a tendency to lead even in this ‘artificial cycle: to get ‘bad first' then to get ‘good first'. The LEI data, encouragingly, show very strong readings in August, September and October. With the second wave of virus in play, this is both surprising and encouraging. Mining and oil show an exceptional lagging behavior with worst values displayed in the most recent data. But Covid-19 has decimated energy prices and that accounts for the lagging behavior of this sector. Housing emerges from this exercise with relatively strong rank of 6th for housing starts in October, the best of any sector except the LEI measure; housing even has a ranking of one in August, a ranking that has since eroded. Still, that is and was a striking post Covid-19 result.

Except for the LEI gauges (that are intrinsically forward-looking) and housing (!), no sector is showing that it has or had fully recovered from the covid-19 hit. Relative to their pre-coronavirus levels in January and February (the two-month average is at table bottom), all rankings are weaker in October than that average except for housing starts and the LEI data (remembering that the unemployment data are on a reverse ranking scale). Canada's recovery may be under challenge by the virus, but all signs say a recovery is still in gear and housing is among the sectors in the vanguard.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief