Global| Jan 11 2016

Global| Jan 11 2016Canada's Housing Starts Grow Weaker

Summary

The global malaises, especially the knock-on effects of weak oil, have been hammering Canada, a natural resource-intensive goods economy. In December, housing starts are lower by 18.4% month-on-month, their sharpest one-month drop [...]

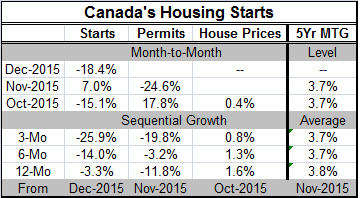

The global malaises, especially the knock-on effects of weak oil, have been hammering Canada, a natural resource-intensive goods economy. In December, housing starts are lower by 18.4% month-on-month, their sharpest one-month drop since January 2013. The drop reverses a rise in November which itself reverses another sizeable drop in housing starts in October. Starts have been becoming increasingly volatile in recent months. The 12-month standard deviation of month-to-month percentage changes is at its highest level since December 2009, confirming this observation.

The global malaises, especially the knock-on effects of weak oil, have been hammering Canada, a natural resource-intensive goods economy. In December, housing starts are lower by 18.4% month-on-month, their sharpest one-month drop since January 2013. The drop reverses a rise in November which itself reverses another sizeable drop in housing starts in October. Starts have been becoming increasingly volatile in recent months. The 12-month standard deviation of month-to-month percentage changes is at its highest level since December 2009, confirming this observation.

Canadian housing starts are lower by 25.9% at an annual rate over three months, at a 14% rate over six months, and at a much more subdued 3.3% rate year-over-year. Permits, which lag by one month, are showing steady and somewhat more pronounced weakness. House price gains are continuing but slowing. Housing is not being destabilized by mortgage rates which remain quite stable. It is the economic environment that is leaching strength from the sector.

Canadian retail sales have been slow with no real trend in place as 2015 progressed. But the leading economic index for Canada has been falling. Still, that index reached its low point in August and has climbed a bit in recent months. Economic momentum is not favorable and is neutral at best, but with some new weakness in the global sphere and in oil prices yet to be discounted.

The housing sector will continue to suffer in this global environment. Disarray in OPEC breeds weakness in oil prices and that in turn has brought plunging oil prices which weigh heavily on investment and output in the oil industry, an important sector in Canada. Real weakness in other commodities has left a pall over the extractive sector as a whole. Canada, of course, is concentrated in this sector.

Central banks try to rekindle growth with monetary policy. In Canada, inflation has remained tolerably close to the bounds monitored by the Bank of Canada, and policy has been steady. Fiscal policy, once overused globally, is still held in abeyance. Special problems in China are destabilizing global financial markets. Canada's housing market is only one of the sectors caught in the squeeze of this international maelstrom.

Housing activity is still not in the doldrums. Despite recent weakness, the level of starts ranks weakly in the 45th percentile among all levels of activity since 1990. But housing is under pressure. The sector reflects some degree of the pressure being faced by the whole of the Canadian economy as well as from global knock-on effects.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief