Global| Oct 18 2013

Global| Oct 18 2013Canada: Another Country Where inflation Remains Under Wraps; But How Much Does That Really Matter?

Summary

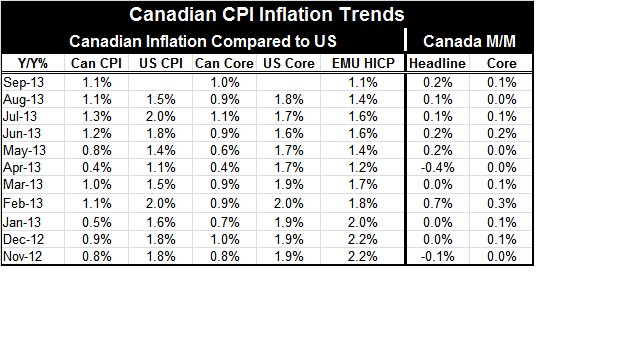

Canada's year-over-year CPI pace has expanded at a 1.1% rate in each of the last two months and has accelerated since November unlike inflation in the US and in EMU that has stabilized or moved lower. Yet inflation in Canada is still [...]

Canada's year-over-year CPI pace has expanded at a 1.1% rate in each of the last two months and has accelerated since November unlike inflation in the US and in EMU that has stabilized or moved lower. Yet inflation in Canada is still as low or lower than inflation in the US and EMU and Canada's core rate continues to run at a pace below the core of the US.

Canada's year-over-year CPI pace has expanded at a 1.1% rate in each of the last two months and has accelerated since November unlike inflation in the US and in EMU that has stabilized or moved lower. Yet inflation in Canada is still as low or lower than inflation in the US and EMU and Canada's core rate continues to run at a pace below the core of the US.

As we look at inflation trends globally it is getting hard to be agitated by inflation accelerations any more...really. Given the long problematic episode in Japan with deflation we now see inflation with a somewhat different eye than before. You can be too rich, too thin, and inflation can be too low (well, maybe not the too-rich part).

Canada's inflation pace at about 1% is in train with GDP growth below 2% and with the GDP growth rate in a downward trajectory. Central banks, long battling to get inflation lower, are now finding that their inflation fighting requires only minimal efforts and in some case, as with the QE program in the US, substantial monetary stimulus is not able to move the needle much on either inflation or growth. Canada is in that same narrow channel. Everyone wants more growth but no one seems to be able to figure it out. Past fiscal and debt excess have taken those tactics off the table.

Canada has a still-elevated rate of unemployment, but at 6.9% the rate is back to where it was in 2005. Canada's unemployment rate has fallen in step with the US rate in this cycle, but Canada has unemployment on a more even keel historically than does the US where unemployment is still high and has been made its progress in curious ways.

Central banks generally seem flummoxed by the current state of affairs. While they can claim victory over inflation, it's unclear that they have had much to do with it- like winning a baseball game because the other side walks in the winning run, or forfeits the game entirely.

Indeed, it appears that the legacy of previous central bank miscues combined with a long string of fiscal mistakes keep inflation low even in Canada where the financial crisis has had the least aggressive bite.

Central banks, from Canada to the US, Europe and Asia, are currently putting up winning inflation numbers but holding their breath. Conventional economic analysis says that central banks have been aggressively accommodative, trying to rekindle demand and despite ongoing inflation-fighting success there are concerns about the future. Can inflation stay in check even as growth returns? Will the excessive monetary accommodation come back to haunt these now-celebrating central banks?

Academics stack-up on ideological lines on these issues. Since we do not understand fully why growth is so weak (if did we could fix it), the policy debate is over the future. That argument pits those who look at historic relationships to return vs. those that don't or who think that we can engage in countervailing policy moves. Frankly, our record at countervailing policy moves has not been a good one. But from A to B to NZ (America, Britain, to New Zealand) inflation is controlled and growth is weak. We can applaud those looking to the future now that the financial crisis has passed, but we also need to improve the here and now. How can we do both?

I believe our recent policy record demonstrates that for whatever reason QE-type programs no longer are effective (if they ever were). The counterpoint that we need to do much more of it to be effective is far too dangerous and idea to implement (too dangerous an `experiment') given the high debt levels in the important monetary center countries around the globe.

While some still say cyclical impacts dominate unemployment, I think the evidence is becoming increasingly clear that the main issues are structural and call for fiscal or regulatory solutions: more fiscal action and less regulation. Those suggestions will make me a pariah among both conservatives and liberals. so they must be on the right track.

Countries around the globe need to attend to their long-term deficit issues. But that does not mean that short-term stimulus is out of the question (except politically, of course). The US, like most countries, has huge future deficits projected stemming from a now unaffordable promise of entitlements. No G-7 country is immune from this problem. Yet, progress on what we promise in the future does not really limit the ability of governments to do more now. Even in fiscally conservative times, actions that cut future deficits could be combined with some carefully thought out short terms stimulus. The problem with fiscal pump priming is that it is done by partisan politics, not according to economic principles. Thus, conservatives in the US will likely not give in to allow it. In Europe austerity may have been damped, but it is still the main program. In Japan monetary excess is having its impact via the exchange rate and that can't last.

All that means that fiscal policy, the likely most effective tool for stimulating growth, is to go unused. Despite the clear message from Europe on the dangers of excessive austerity, too many countries are trying to get instant religion on debt and deficits and in downsizing government and that can't help but retard growth in the short turn (real time!). At the same time our technology revolution is enabling us to make more with fewer workers so unemployment is stubborn even as we achieve some growth. In the US unemployment is falling mostly as people leave the labor force. This can't be any sort of lasting solution.

Low inflation is nice. I suspect it will be with us much longer since the forces restraining growth and hiring are still active. I am much more concerned about the prospect of political instability stemming from poor economic performance than I am worried about inflation flaring up.

This economic slowdown has been one that cut a broad swath across income groups and across nations. Although the rich have fared better than most (as always) there has been some great dislocation, even among the affluent, or formerly affluent. At some points nations will have to take a longer term look at the issues. Fiscal and monetary policy will have to be considered together and ideology will have to be tempered to acknowledge the challenges of the times. You might want to be a well-rounded athlete who can run, lift weights and swim. But if there is a flood, swimming will be the most important skill. While swimming you may wonder about your survival when the water level falls. but don't forget to swim while you ponder that prospect. We are doing too little swimming and worrying too much about the future, trying to set plans based on pre-flood ideologies. Does that make any sense? You may be worried about inflation; I am worried about the sharks.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief