Global| Apr 28 2021

Global| Apr 28 2021Can You Tell When the Virus Struck Germany?

Summary

Rod Stewart famously sang 'every picture tells a story, don't it?' Bad grammar aside, the saying is true just as it's true that a picture is 'worth a thousand words'...and that expression pre-dates 'Word' and its ability to [...]

Rod Stewart famously sang 'every picture tells a story, don't it?' Bad grammar aside, the saying is true just as it's true that a picture is 'worth a thousand words'...and that expression pre-dates 'Word' and its ability to continuously generate a document's 'word count'! How did they know that?

Rod Stewart famously sang 'every picture tells a story, don't it?' Bad grammar aside, the saying is true just as it's true that a picture is 'worth a thousand words'...and that expression pre-dates 'Word' and its ability to continuously generate a document's 'word count'! How did they know that?

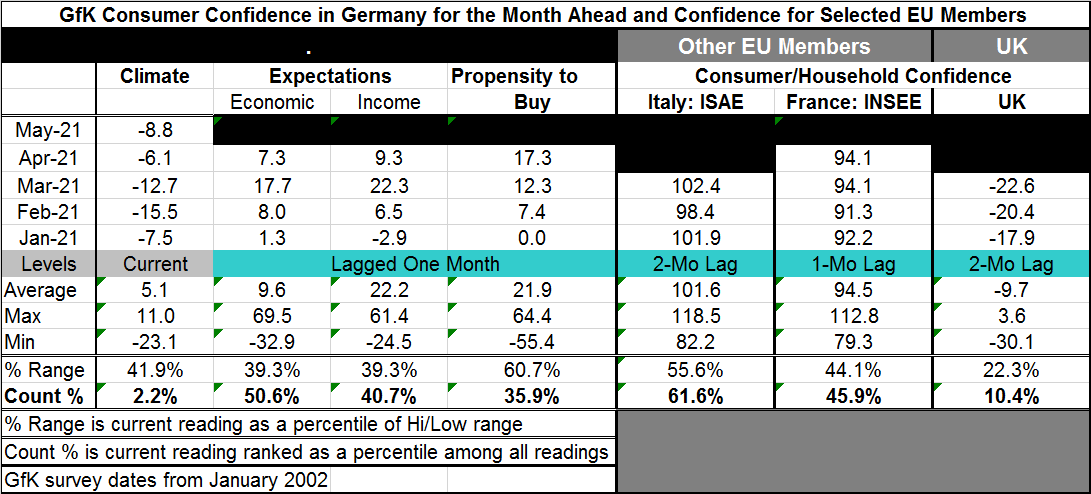

In the case of this chart for Germany, however, nothing could be truer than these two expressions. Consumer climate simply plunged off of a ledge that would have struck fear into the heart of even Wile E Coyote. However, since that plunge, there has been no sustained recovery for Germany. There is a spike low and a rebound. The rebound captures a bit more than half the loss for climate but then there is a relapse and another disappointing rebound. Now there is yet another relapse-in-the-making.

The dual impact of the virus

Expectations have moved in lockstep with climate during this period although the chart plainly shows (saving us another 1,000 words) that such co-variation between these two series has been historically rare.

What this graphic shows, well, graphically, is how these two very different measures are each locked onto the very same thing that has wrenched both of them to and fro. That 'thing,' of course, is the Virus.

The viro-conomy

As I have long maintained, the virus has taken the place of economics since there is no economic trend that matters, that can't be subverted, trumped, wiped out, and even reversed by an outbreak of –or the hibernation of- the Virus. In the U.S., the degree of vaccination is growing and this is enabling more confidence about the future and about current activity and we can see day-by-day conditions in the U.S. getting stronger. There is still risk and the head of the CDC in the U.S. is sometimes more (seemingly) apoplectic than is warranted. All this contrasts with Europe and, of course, Germany in particular where vaccination has lagged. The EU is now suing AstraZeneca for nonperformance on its contract and trying to prevent the export of any vaccine made in facilities in Europe. After failing to persuade AstraZeneca to do such a thing of its own volition, the EU has turned to heavy-handedness.

While there is no denying that lingering outbreaks in Europe are real, dangerous and debilitating, the situation in Europe pales next to the drama unfolding in India. In Europe, it was the EU's own error in not procuring enough vaccine at the start that has helped create these delays. Now it wants to punish not 'the messenger,' but the vaccine maker.

The cost of Brexit...was worth it!

It is on days like this that the U.K. can breathe a breath of fresh air and look at the huge costs of Brexit and say… "It was worth it." The U.K. has made so much better progress on the virus than the EU all on its own. Had the U.K. still been part of the EU, it would have had the vaccine it procured torn from it and shared across Europe. Some things can be done better in a customs union. Other things cannot. And so far, God has not given the EU the wisdom to discern the difference between those two things or to accept fully the consequences of its own missteps. Suing AstraZeneca for its own mistake is a good example of misplaced values.

Where Germany stands

The German GfK measure shows us that the virus is still an active force in Germany. Note that this is a May forecast for confidence a look ahead. As such it is based on up-to-date data perceptions and observations and yet there is another dip in the index.

At -8.8 in May, the index has slipped from -6.1 in April. While the headline reading improved in April (-6.1) from March (-12.7), the economic reading (component readings lag the topical headline by one month) fell to 7.3 in April from 17.7 in March. Income expectations fell also to 9.3 in April from 22.3 in March. The only component to move higher in April was the propensity to buy, climbing to 17.3 in April from 12.3 in March.

The queue percentile standings labeled as 'count %' in the table find the May headline at a 2.2 percentile standing; the April readings are at the 50.6 percentile for economic expectations, the 40.7 percentile for income expectations, and despite the rise in the month, at the 35.9 percentile for the propensity to buy.

Other Europe

The topicality of Italian, French and U.K. confidence has various timing issues but all lag the German experience by one or two months. Right now trends are not so clear so the inherent bias of having a reading from a different month is unclear. But in Italy, confidence sits at its 61.6 percentile as of March. For April, France has a 45.9 percentile standing. For March, the U.K. has a very weak 10.4 percentile standing.

Summing up

With the virus in play, it's the same old song: uncertainty. Nobody knows what tomorrow will bring. There are optimists and pessimists. Be careful to whom you listen. Truth is out there somewhere, but these days it all too often is hiding behind someone's partisanship or political agenda so watch your step, be nimble and use your brain. Vet carefully the things you are told.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief