Global| Jan 10 2018

Global| Jan 10 2018British Chamber of Commerce Survey for Q4 Is Mixed and Sour

Summary

The BCC survey is a somewhat marked contrast to the new estimates for Q4 GDP also released today from NIESR (the National Institute of Economic and Social Research). NIESR estimates that the U.K. accelerated in Q4 growing at a [...]

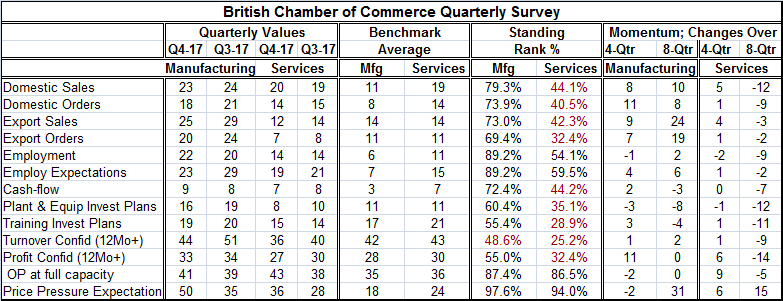

The BCC survey is a somewhat marked contrast to the new estimates for Q4 GDP also released today from NIESR (the National Institute of Economic and Social Research). NIESR estimates that the U.K. accelerated in Q4 growing at a quarterly pace of 0.6%, up from 0.4% in Q3. The Chamber of Commerce characterizes growth in Q4 as 'subdued.' Most service sector readings are below their pre-EU referendum levels. While manufacturing fares better in the survey, readings are generally trailing when compared to their Q3 levels.

The BCC survey is a somewhat marked contrast to the new estimates for Q4 GDP also released today from NIESR (the National Institute of Economic and Social Research). NIESR estimates that the U.K. accelerated in Q4 growing at a quarterly pace of 0.6%, up from 0.4% in Q3. The Chamber of Commerce characterizes growth in Q4 as 'subdued.' Most service sector readings are below their pre-EU referendum levels. While manufacturing fares better in the survey, readings are generally trailing when compared to their Q3 levels.

The Curious Labor Market

The Chamber of Commerce survey, like the NFIB survey in the U.S., has a query about the quality of labor. In services 71% of the firms responding to the survey reported skill shortages and claimed that the shortages were reaching critical levels. Manufacturers report the most difficulties finding skilled workers that they have had since 2016. Interestingly, these complaints parallel the complaints currently being fielded in the U.S. NFIB report. But in the U.K., like in the U.S., wages seem to be mostly unaffected by this complaining. The U.S., Germany and the U.K. all are reporting low unemployment rates that have been better than current levels since the early 1990s only about 5% of the time or even less (see yesterday's report "Euro Area Unemployment: Lowest Since 2009").

Brexit-related Hurdles Appear

Firms in the U.K. are experiencing several different sorts of pressures and these stem from the U.K.'s Brexit vote and subsequent fall-out. On one hand, there is uncertainty about demand in the post Brexit environment because there is uncertainty about how U.K. firms will be treated by the EU and what their business prospects are. Secondly, there are firms leaving to relocate in the EU area to protect themselves in the case of a most adverse ruling. Thirdly, there are questions regarding how EU workers that have been employed in the U.K. will be treated once the U.K. achieves EU separation and some have left as a result. This might be resulting in some form of 'brain drain' from the labor market. There is also the aggressive BOE move after the Brexit vote that pushed the pound sterling lower and improved the competiveness of U.K. firms selling abroad. While the BOE has begun to unwind that move, sterling remains on balance lower and that might explain why manufacturing firms are doing better than services firms in the survey. It also explains the high inflation expectations in the survey since inflation has shifted up as sterling shifted down.

The Service Sector

Over four quarters, the service-sector categories mostly show improved responses. But when services categories are compared with their levels of eight quarters ago, there are net declines up and down the line of responses. Furthermore, viewed through a much broader relative lens, the queue rankings of the various responses compared to all other responses back to Q2 1990 shows that of the 13 responses listed in the table service sector firms have readings below their period medians in 9 of them. Only two categories are strong for services and that is for responses to the question "operating at full capacity?" and for price pressure expectations. Of course, inflation in the U.K. has been running over the top for some time in the wake of the drop of sterling. There are exceptionally low readings (below their 40th percentile) for export orders, plant and equipment investment plans, training & investment plans, turnover confidence, and profit confidence. It is interesting that despite complaints about worker quality firms do not intend to ramp up training.

The Manufacturing Sector

The manufacturing picture is much stronger with only four quarterly declines logged in the quarter-to-quarter survey and only three net lower readings when compared to eight quarters ago. Both 4-quarter and 8-quarter changes are negative for plant and equipment investment plans a rather clear signal that Brexit uncertainty is holding back capital spending in the U.K. Manufacturing firms, like service sector firms report a high proportion of firms operating at full capacity and register price pressure expectations in their queue standing responses. Manufacturing has only one response below its historic median and that is for turnover confidence. Profit expectations are at a queue standing of 55%, but sales (turnover) confidence is weaker at a 48.6 percentile standing. For the most part, the rest of manufacturing readings are relatively firm to strong with capital spending plans being one of the lowest standings along with training and investment plans. Manufacturers have capital investment plans with a 60.4 percentile standing and training plans at a 55.4 percentile standing. Despite skills shortages, firms are not investing in training with much gusto. And as mentioned earlier, capital spending is being held back despite high capacity usage.

Summing Up

Despite the relatively upbeat NIESR outlook for Q4 growth, the BCC survey gives us ample reason to put out the caution flag and slow the pace of optimism. Firms are beginning to act in some dysfunctional ways by complaining about labor skills but being unwilling to either pay up for better quality labor or being willing to train labor to upgrade it. Neither action is really irrational since a trained worker could leave and take his newly acquired skills with him in tight labor market and even if the labor market is tight firms cannot overpay for labor, being limited to paying labor only for its ability to produce. Still, there are work-arounds for the issues at hand and yet the policy in force seems to be to doing very little other than to log complaints. Kicking the can down the road and waiting for greater certainty to appear is not pro-active. This is not a pro-growth strategy to say the least. Whatever growth proves to be in Q4, the BCC survey is putting us on notice for the future.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief