Global| Sep 10 2018

Global| Sep 10 2018BOF Survey Makes Gain in August; BOF GDP Outlook Is Unchanged

Summary

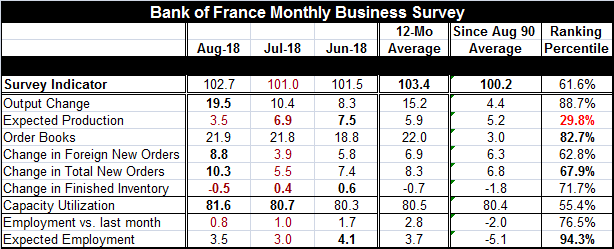

The Bank of France survey shows a headline reading in August at 102.7; that is stronger than its July reading of 101. The BOF index peaked at 107.1 in December last year. It retreated sharply from its December reading to 104.3 in [...]

The Bank of France survey shows a headline reading in August at 102.7; that is stronger than its July reading of 101. The BOF index peaked at 107.1 in December last year. It retreated sharply from its December reading to 104.3 in January; it steadily eroded until it hit is recent low at 99.8 in May. Since May, the index has oscillated around reading with a ‘101 handle’ of some sort. The August reading at 102.7 is the highest reading since February 2018, but is still below the 12-month average of 103.4. On balance, the BOF index has boomed and eroded, settled, and now has stirred. But how much weight should we put on this newfound strength and rebound? The BOF seems circumspect.

The Bank of France survey shows a headline reading in August at 102.7; that is stronger than its July reading of 101. The BOF index peaked at 107.1 in December last year. It retreated sharply from its December reading to 104.3 in January; it steadily eroded until it hit is recent low at 99.8 in May. Since May, the index has oscillated around reading with a ‘101 handle’ of some sort. The August reading at 102.7 is the highest reading since February 2018, but is still below the 12-month average of 103.4. On balance, the BOF index has boomed and eroded, settled, and now has stirred. But how much weight should we put on this newfound strength and rebound? The BOF seems circumspect.

A significant rebound but how significant?

The August rebound is a significant departure from the recent months which appeared to be chronicling and ongoing deceleration. With this August reading, the question of trend is put back in play. Of course, the surrounding European data have been largely weaker especially in Germany where exports, orders and IP (all as real variables) have been showing weakness. It is hard to believe that France is going to stage a rebound with Germany and the rest of the EMU in a period of moderation.

Context

To provide some context, the Markit PMIs show the French total PMI higher in August than in July by 0.5 diffusion points but only above its three-month average by one tick. The BOF survey has much more acceleration than that. All of the EMU is only two ticks stronger in August than in July and the August composite PMI value is one tick below its three-month average. The background here pertaining to the EMU and gleaned from another French survey for August is less upbeat.

GDP

The BOF uses this survey to estimate GDP growth for the next quarter. On that basis, the BOF has not adjusted its outlook compared to last month. According to the monthly index of business activity, gross domestic product is set to expand 0.4% in the third quarter, unchanged from the previous estimate.

The survey details

The August survey shows a strong reading for output change at 19.5, compared to 10.4 in July. But expected production only logged a reading of 3.5, down from July’s 6.9. The outlook has slipped for two months in a row. Order books are pretty steady with a reading of 21.9 in August, compared to a reading of 21.8 in July. If we stop here to compared where these three readings stand in their historic profile, we find that the output change and order book readings are high in their respective 88th and 82nd percentiles while the expected production gauge lies only in its 29th percentile – very weak.

The change in foreign orders and in total new orders both moved higher in August after weakening in July. And both have rebounded enough to exceed their respective June levels as well. Still, orders of both types have queue standings in the 62nd to 67th percentiles which are moderately above their respective medians (medians occur at a ranking of the 50th percentile).

Inventory diffusion is low and has fallen off in each of the last two months; it actually logs a decline in August. Still, this metric has a ranking in its 71st percentile. Obviously, inventory changes that show declines are quite normal to some extent much more so than for other variables.

Employment vs. last month has slowed for two months running. Expected employment actually rose in August, reversing a weakening in July. Both the monthly employment change and the employment expectation are below their 12-month averages. However, the monthly change has a standing only in its 76th percentile while the expectation reading ranks in the 94th percentile and ranks among the top 6% readings all time.

The upshot

These results tell us that French output is still expanding briskly in the estimation of most mangers but that the outlook is under some pressure. Orders are no cause for concern as order books continue steady at a relatively elevated level although the change in orders both overall and in the export market have become more moderate. While employment is slightly less robust, the outlook remains for continued high levels of employment. That portion of the survey seems to grate against the production outlook response.

These are relatively solid numbers and make for a firm outlook. The BOF has kept its own quarterly assessment of GDP for a pace of 0.4%, an annual rate pace of 1.6% which remains modest. The sense in which the French survey depicts some pick up at this point is being set aside, it seems. The BOF is being cautious about raising its outlook, based on survey data. Perhaps that is because it is also wary about unfolding trade events and their eventual impact. The reduction in the expected production index to a diffusion reading of 3.5 in August from 6.9 in July leaves it below its 12-month average of 5.9; it has only a 29th percentile queue standing. That seems to be catching the eye of the BOF forecasters the most.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief