Global| Apr 10 2017

Global| Apr 10 2017BoF Index Holds Most of Its Recent Gains; Still BoF Scales Back Its Growth Outlook

Summary

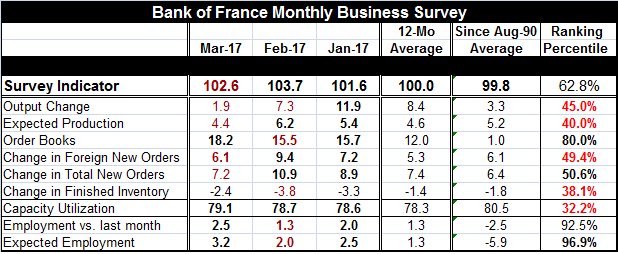

The Bank of France cut back its outlook for growth to 0.3% in the first quarter from a previous estimate of 0.4%. Its business index in March fell to 102.6 from 103.7 in February. The February index had jumped to that level from [...]

The Bank of France cut back its outlook for growth to 0.3% in the first quarter from a previous estimate of 0.4%. Its business index in March fell to 102.6 from 103.7 in February. The February index had jumped to that level from January's 101.6. At its new March level, the business index standing is in the 62.8 percentile of its historic queue of data, higher less than 38% of the time. That's a firm, but not impressive, standing.

The Bank of France cut back its outlook for growth to 0.3% in the first quarter from a previous estimate of 0.4%. Its business index in March fell to 102.6 from 103.7 in February. The February index had jumped to that level from January's 101.6. At its new March level, the business index standing is in the 62.8 percentile of its historic queue of data, higher less than 38% of the time. That's a firm, but not impressive, standing.

Survey component standings

The standings for the index find very highs marks for current and expected employment each of which stand in their respective 90th percentile ranks. Orders books show a strong accumulation of business with an 80th percentile standing. After that, there is a lot more equivocation. The change in 'foreign new orders' and the change in 'total new orders' each show percentile readings that reside near their respective medians historically. Output change and expected output have 40th to 45th percentile queue standings, a bit below their respective medians (medians occur at the 50th percentile mark). Inventories and capacity usage each post readings below their respective 40th percentiles.

Momentum

The overall index is lower by 1.1 points month-to-month. Of the nine components, four are lower month-to-month. One of them, output change, is sharply lower. The output change has slipped all the way to 1.9 in March from 7.3 in February. It is the weakest reading in nine months since the index last posted a negative reading. The peak reading for this component was in December and it has slipped steadily ever since. Expected production also stepped back to a reading of 4.4 from 6.2 previously. Expected production was last weaker in December (not surprisingly), the month that has the peak gain in output. Survey participants recognized that as the peak. In January and February, stronger expected gains were posted, but in March there is a weaker output outlook (but still a positive one) although as with the output change variable the reading is below its average reading since 1990. Order books are a bright spot with a month-to-month gain rising to 18.2 from 15.5, logging a well-above average reading. However, the change-in-order components are weaker month-to-month. Foreign new orders slip to 6.1 from 9.4. They are above their 12-month average and on top of their longer terms average; they were last weaker in October of last year. Total new orders fell to 7.2 from 10.9 and are slightly below their 12-month average of 7.4 but above their longer term average. This series also was last weaker in October of last year. The change in finished inventories rating shows a negative reading but a less deeply negative reading than over the last two months. Still, the reading lies below its 12-month and longer term averages. The index was last stronger in December. Capacity use is up on the month and resides above its 12-month average reading, but not its longer terms average. It was last lower in November. The two job metrics are both stronger on the month and above their respective 12-month and longer term averages. The monthly assessment was last stronger in November, but the outlook was last stronger in January of 2001- a long time ago.

The details of the BoF index and its components shed a bit more light on why the BoF has cut back its outlook for Q1 growth. There had been some very strong momentum that has faded to a large extent across the board. The one exception -and a very important one - is the assessment of expected employment. French firms are feeling more solid about their job situation than they have for a long time. Orders books seem quite filled and new orders are coming in at a healthy clip. However, actual output change and expected production have lost some momentum. But new orders are still solid. There is room for some optimism but no need for too much. The BoF has struck its balance this month.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief