Global| Jun 18 2020

Global| Jun 18 2020BOE Agents' Survey Remains Very Weak

Summary

The Bank of England Agents’ Survey is an aid to the BOE for policymaking. The survey is a series of judgmental responses that are scored on a scale from +5 to -5. A simple weighting of the responses shows this to be the weakest survey [...]

The Bank of England Agents’ Survey is an aid to the BOE for policymaking. The survey is a series of judgmental responses that are scored on a scale from +5 to -5.

The Bank of England Agents’ Survey is an aid to the BOE for policymaking. The survey is a series of judgmental responses that are scored on a scale from +5 to -5.

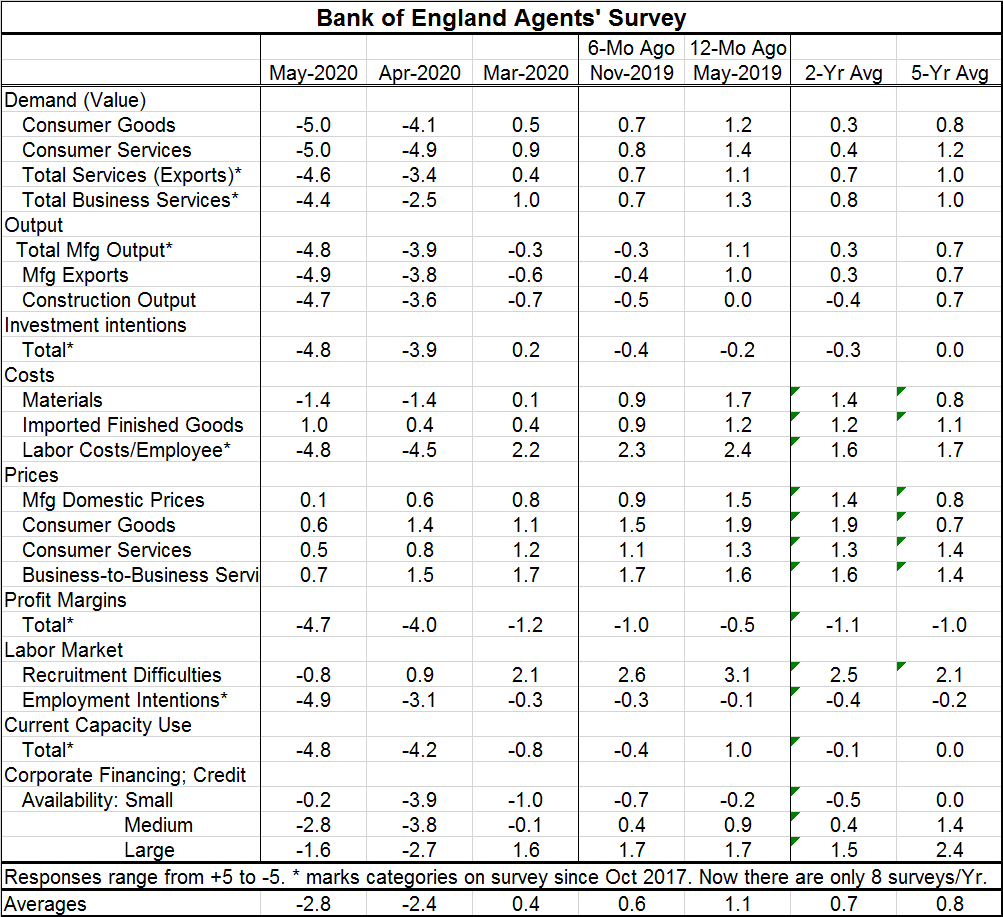

A simple weighting of the responses shows this to be the weakest survey on average in its history. The last two months have readings that are uncharacteristically weak. The survey has been in use in some form since mid-1997. The survey that has changed a lot over this period has produced average negative ratings across all categories in a month about nine percent of the time and until the last two months the largest negative average was -0.6. For May the average response is -2.8, compared with a response of -2.4 in April. The negativity came on suddenly as March scored a +0.4. I do not mean to put an overly fine point on these numbers especially since the survey has changed and expanded over time. Also I am using a simple approach, a simple average of all responses and not attempting to weight the most important responses. This averaging is simply a way to try to make some comparisons of a complicated response set with history.

The Agents’ Survey, like many other better-known U.K. surveys, has been weak in the wake of the Brexit decision and the unknown future attached to that. So the coronavirus caught the economy in an already weak position. The average agents’ response in late-2019 was in its lower quartile at about a 24th percentile standing. That reading quickly turned much weaker as the virus hit.

The U.K. economy continues to reel under the impact of the virus. Demand has been hit hard as the agents' response makes very clear. Both consumer goods and services attack a worst possible -5 rating. Output rivals the weakness in demand with rating quite near -5 from total manufacturing output, manufacturing exports and for construction. Investment intention decisions record a -4.8 response. Costs show more variation in their assessments with labor costs near a -5 reading and imported finished goods assessed at +1.0. Prices also show resiliency with low but positive readings across the categories. Firms were assessing their profit margins negatively since mid-2017 when the survey began. But in April and May, the assessments went south very quickly and deeply. Similarly, labor recruitment assessments have been exceptionally weak over the last two months. Corporate financing has been under pressure for a number of months across firm size. However, the advent of support programs has improved respondents’ assessments in May compared to April.

In view of all the distress in the economy, the BOE has just announced an increase in its QE program to support the economy. The monetary policy committee decided to lift the asset purchase program by GBP 100 billion to GBP 745 billion. Eight members including Bailey voted to raise the QE as they judged that a further easing of monetary policy is warranted to meet its objectives. However, one member, Andrew Haldane, preferred to maintain the program at GBP 645 billion.

On an optimistic note in an unrelated action today, the Baltic dry goods index jumped as capesize vessel segment rates jumped 50% on strong iron ore demand. The Baltic dry index, which tracks rates for ships ferrying dry bulk commodities and reflects rates for capesize, panamax and supramax vessels, rose 281 points, or about 22.6%, to 1,527, its highest since Dec. 10. The Baltic capesize index jumped 1,217 points, or 49.6%, to 3,672, its highest since Sept. 25. These are powerful signs of greater shipping activity and of an increase in the pulse of the global economy. Up to this point we have seen a bottoming in global PMI indexes and there have been a few reports of real strength in the U.S. economy. Today another U.S. report kicked up its heels, the regional Philadelphia Fed manufacturing report. However, the Baltic dry goods index is a global barometer and its rebound is welcome news to all global trading economies.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.