Global| Mar 09 2016

Global| Mar 09 2016Bank of France Monthly Survey Slips; BoF Cuts GDP Outlook

Summary

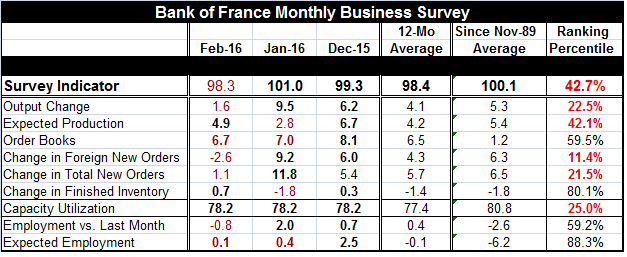

The Bank of France business indicator took a sharp turn south in February as it dived back below its October 2015 level but above its November 2015 level. Upon seeing its survey results, the Bank of France cut its Q1 GDP outlook to a [...]

The Bank of France business indicator took a sharp turn south in February as it dived back below its October 2015 level but above its November 2015 level. Upon seeing its survey results, the Bank of France cut its Q1 GDP outlook to a gain of 0.3% from 0.4% it held previously.

The Bank of France business indicator took a sharp turn south in February as it dived back below its October 2015 level but above its November 2015 level. Upon seeing its survey results, the Bank of France cut its Q1 GDP outlook to a gain of 0.3% from 0.4% it held previously.

The survey results show the BoF indicator standing only in the 42nd queue percentile of its historic range. That is well below its median (50th percentile).

However, several of survey components are above their respective medians and by a good deal of space. The expected-employment gauge, as well as the change in finished inventories, has a reading near its 90th percentile, a very high standing. Even so, these two gauges show raw diffusion values are very low- either negative or barely positive. For expected employment, this demonstrates the pressure that French industry has been under over this entire period back to late 1989. We cast averages for the last 12 months as well as back to 1989 and over the last year the employment gauge also is borderline negative but still much stronger over 12 months than it has been over the full period of over 25 years. For inventories, the build news is not such good news, as rising inventories amid other signs of weakness usually generate output pullbacks.

Past employment also has a relatively firm reading at a 59.2 percentile standing. This simply tells us that the employment situation has been relatively firm. It is the same ranking as for order books where the quantity of orders on the books is in a relatively firm position. But new orders are overall much weaker. Total new orders are only in their 21st percentile and new foreign orders are even weaker in their bottom 11th percentile. These are growth-threatening readings. Thus, not surprisingly, expected production is at a 42nd percentile standing while the actual output change shows a 22nd percentile standing. Capacity utilization is very low with a 25th percentile standing; there is no supply constraint.

These metrics show a relatively sharp turn lower in the survey as evidenced by the graph. By the numbers, there is weakness in output as well as more weakness expected in production and more expected to come with new orders slipping. All this is led by order weakness from abroad. Despite some very low percentile standings, this weakening has not yet manifested itself as pessimism on the employment front. Indeed, the outlook for employment is still much more upbeat than the assessment of past employment situation. We have to wonder about this. Are firms late to the game of setting employment expectations? Or is this slowdown we are registering going to be episodic in nature? The weakness in the survey certainly suggests that the slowing is something to be wary of. The Bank of France is wary enough to have cut its Q1 GDP outlook. Will that outlook stabilize? For now we have to put the French GDP outlook on watch pending the result of the next survey given that the February picture deteriorated suddenly and sharply. The shallow rising gradient in the BoF index is still in place but will stay there only if this monthly deterioration proves to be a one-off affair.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief