Global| Nov 09 2015

Global| Nov 09 2015Bank of France Indicator Jumps in September; Still Not Out of the Woods

Summary

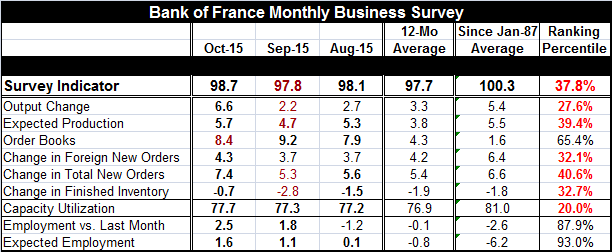

The Bank of France indicator moved up to 98.7 in October from 97.8 in September. It is still below its long-term average of 100. Nonetheless, the pick-up in this indicator has the Bank of France looking for growth of 0.4% in Q4 2015, [...]

The Bank of France indicator moved up to 98.7 in October from 97.8 in September. It is still below its long-term average of 100. Nonetheless, the pick-up in this indicator has the Bank of France looking for growth of 0.4% in Q4 2015, up from a 0.2% gain estimated for Q3.

The Bank of France indicator moved up to 98.7 in October from 97.8 in September. It is still below its long-term average of 100. Nonetheless, the pick-up in this indicator has the Bank of France looking for growth of 0.4% in Q4 2015, up from a 0.2% gain estimated for Q3.

The French business survey indicator rose on a broad front in October, improving in seven of eight key components month-to-month. This is an improvement in the change from September when four indicators weakened.

The October indicators all show better values than their 12- month averages, a testament to the sense of improvement on the year. Moreover, only the change in foreign orders this month is below its long-term average from 1987. This echoes the weakness reported earlier in German orders where the foreign sector was found to be extremely weak.

While there is clear evidence of improvement and of ongoing improvement, there is still a very long way to go. The French survey indicator lies only in the 37th percentile of its historic queue of data. That means the indicator has been weaker only about 37% of the time and stronger about 63% of the time. The indicator is near the bottom third of its historic range and that means the survey components will produce generally weak readings.

The weakest readings of the survey are for capacity utilization (20th percentile), the change in output (27th percentile), the change in foreign orders (32nd percentile), and the change in finished inventories (32nd percentile). However, the weak build in inventories could be a positive as inventory building does not appear to be excessive by historic standards and has been pacing with output changes (27th percentile compared to the 32nd percentile for inventories).

The middling comparisons are made up of still below median readings for the most part, production (39th percentile), change in new orders (40th percentile) and the stronger overall order book reading with a 65th percentile (above median) standing.

The strong readings are for employment with the `employment vs. last month' response rated as the 13th best and the `expectation ahead' rated as the 7th best overall.

Employment optimism stems from some real progress and optimism about the future given improved conditions in October.

The percent of queue standings, however, remain very weak for France - generally below their respective medians. Year-over-year French GDP has only attained a 1% year-over-year pace in Q2 after five even weaker previous quarters. French growth is struggling and is only beginning to get a toe hold on improvement. And the global environment is still challenging.

Today the OECD trimmed its forecast for growth this year and cut more substantially its outlook for 2016. The OECD is concerned about the withering growth of international trade which correlates strongly with global output. Both the German and French reports this month registered a pull-back from overseas orders. That China will have a weaker path is expected, only the degree of its slowing is a point of argumentation. The OCED flagged ongoing weakness in developing economies as a problem.

It looks like the Fed in the U.S. will engage its tightening cycle at yearend. The U.K. has been set back in its quest to consider a hike. More monetary stimulus is in store in the EMU. Exchange rates are moving in the right direction to help France, but global growth has been so weak that price competiveness has not helped much. Time will tell if monetary policy can help. But a period of still-slow growth lies ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief