Global| Jul 11 2016

Global| Jul 11 2016Bank of France Business Indicator Is Flat

Summary

The Bank of France business indicator is flat in June, hovering just outside the lower one-third ranking in its historic queue of data. Expected production is back up in June after posting a negative survey value in May and sits in [...]

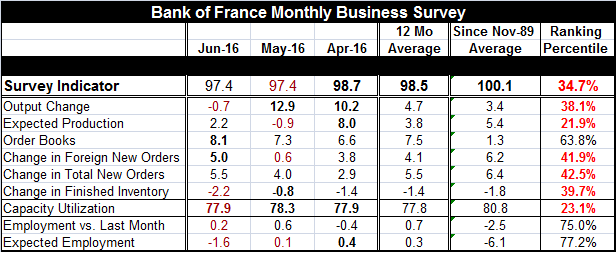

The Bank of France business indicator is flat in June, hovering just outside the lower one-third ranking in its historic queue of data. Expected production is back up in June after posting a negative survey value in May and sits in its lower 21st percentile of its queue of data since November 1989. Expected production made strong strides until 2015/2016 when it settled down and has been moving sideways at this still historically weak level around a survey value of zero.

The Bank of France business indicator is flat in June, hovering just outside the lower one-third ranking in its historic queue of data. Expected production is back up in June after posting a negative survey value in May and sits in its lower 21st percentile of its queue of data since November 1989. Expected production made strong strides until 2015/2016 when it settled down and has been moving sideways at this still historically weak level around a survey value of zero.

Order books continue to improve showing a 63rd percentile standing, the strongest relative standing of any component except for employment. Both foreign and new orders moved higher in June compared to their May values; both of these series still have a queue standing in their lower 40th percentile.

Capacity use slipped in June with the drop in output. Capacity utilization has an extremely weak 23rd percentile standing.

The employment reading posted a weaker month-to-month survey value and expected employment slipped and posted a negative reading. Still, the queue standings for both employment and expected employment are relatively firm in the mid-to-upper 70th percentile of their respective historic queues.

Despite these overall weak standings, the Bank of France finds these results consistent with another 0.2% gain in GDP in the second quarter; this is the same as its estimate made last month.

Today the IMF trimmed its outlook for euro area growth to 1.4% from 1.6%, a small setback for the current year. The slight cut back in the IMF's forecast stands in contrast to statements about the draconian nature of the risk of Brexit uttered before the vote. Italy in May saw its industrial output fall by 0.6%. The upshot is that globally growth is still without traction and with a weak outlook.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.