Global| Aug 05 2005

Global| Aug 05 2005Bank of England Cuts Base Rate as Financial Strains Start to Show

Summary

Citing sluggish consumer and investment spending, the Bank of England yesterday reduced its repo rate from 4.75% to 4.50%. This was the Bank's first change in the rate in exactly a year, since August 5, 2004, when it raised the rate [...]

Citing sluggish consumer and investment spending, the Bank of England yesterday reduced its repo rate from 4.75% to 4.50%. This was the Bank's first change in the rate in exactly a year, since August 5, 2004, when it raised the rate to 4.75%; it last cut the rate in July 2003, from 3.75% to 3.50%. As we have noted here recently, including some commentary on the German economy yesterday, the economic situation in Europe is somewhat ambiguous, and the ECB chose at its meeting yesterday not to reduce its comparable base rate.

In the UK, a few indicators show that the picture is fuzzy there as well. Industrial production for June, reported today, edged down 0.1%, although some prior periods were revised higher. Manufacturing output increased 0.2% in June, better than market forecasts of 0.1%. The ONS indicated that it had made the new data available to the Bank's Monetary Policy Committee in time for its meeting.

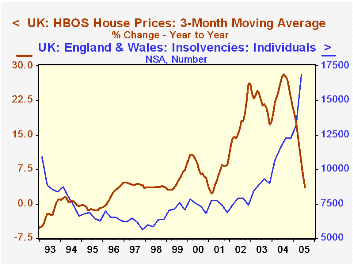

In contrast, the widely watched Halifax House Price Index was quite weak. As evident in the table below, these prices have slowed dramatically in recent months. The year-on-year home price inflation rate, at 2.3%, was the lowest since 1.3% in April 1996. Clearly the housing "bubble" in the UK -- if this price swing can be called that -- is over. Further, and perhaps in partial response to this development, consumer insolvencies in England and Wales have surged: data released this morning by the Department of Trade and Industry, show that these were nearly 17,000 in Q2, up a whopping 46.3% from a year ago. Company insolvencies, which had dipped below 3,000 for each of the previous three quarters, increased by 370 in Q2, or 12.4%. Thus, while real economic activity is hardly suffering in the UK, there are distinct financial strains. If allowed to go unanswered, the Bank of England seems to believe, they could well impose some suffering on the real economy.

| July 2005 | June 2005 | May 2005 | 2004 | 2003 | 2002 | |

|---|---|---|---|---|---|---|

| HBOS Housing Price (SA, £) | 162,994 | 162,693 | 162,424 | 156,979 | 132,235 | 110,947 |

| % Change* | 2.3 | 3.7 | 5.6 | 18.8 | 19.0 | 20.9 |

| Industrial Production (% Change, SA) | -- | -0.1 | 0.3 | 0.8 | -0.5 | -2.5 |

| Manufacturing (SA) | -- | 0.2 | 0.2 | 1.9 | 0.1 | -3.1 |

| Bank Repo Rate(Avg, %) | 4.75 | 4.75 | 4.75 | 4.38 | 3.69 | 4.00 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief