Global| Jul 19 2013

Global| Jul 19 2013As Central Banks Struggle With Policy,

Summary

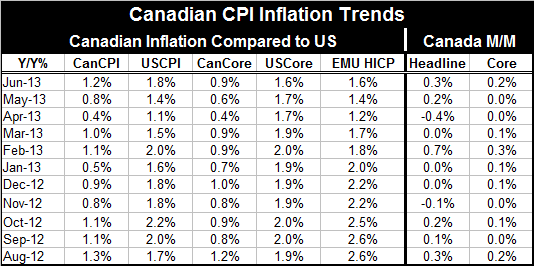

Local inflation trends seem to be launched on highly similar paths. Headline inflation in Canada is up by 1.2% compared to 1.8% in the US and 1.6% in the European Monetary Union. Canada's inflation of 1.2% is its highest since August [...]

Over the years economists have basically been taught to observe inflation as principally a monetary phenomenon which means it's principally a domestic monetary phenomenon. And, of course, no sooner do we teach everyone this sort of lesson that it no longer seems to be true. I realize that that's a bit of heresy.

Clearly global demand conditions have a lot to do with keeping inflation low on a worldwide basis at the moment. Having come through a financial crisis and, in fact, not having really having come all the way through it, we find that we are possibly still only in the eye of the storm. There is still the final leg of the extraction from the crisis to be accomplished. The crisis both revealed and created substantial worldwide debt problems. These problems, in turn, threw nations and their individual transactors into a state of disequilibrium, forcing them to deal with what they suddenly realized was a situation of excess debt. Thus the need for individuals and nations to devote more resources to paying off past debts rather than to piling on more debt and spending in excess of income has knocked spending trends off their patterns leaving many industries with excess supply.

Excess supply drives prices lower.

In this situation, excess supply has exerted substantial pressure, downward pressure, on global prices. That's one of the reasons that we see inflation subdued globally. Countries are linked by international trading and capital flows so that price disturbances in one area also affect another area.

However, what we also see is that while there are substantial growth rate differences in the growth of the M2 money stocks in the United States, the European Monetary Union, and in Canada, their money growth rates also have broadly gone through the same sorts of transitions.

Prior to the onset of the financial crisis money growth rates were accelerating. In EMU the growth rate of money peaked before the financial crisis; in both the US and in Canada the growth rate of money spurted and peaked during the crisis.

In all three regions money growth rates dived during the crisis. Early on, during the workout phase, money growth was moderate and low in Canada and in EMU, accelerating only in middle-to-late 2011, while, in the US, money growth rates have been much stronger from the outset. They saw a bubble in the growth rate emerge, then growth rate settled back down below 7 1/2%. Currently growth rates in these three countries see M2 roughly between 5% and 7 1/2%.

Monetary theory warns us never to be too certain about predicting inflation. The monetary expert Milton Friedman long ago warned of how money supply had long and variable lags in its effect on the economy. However, I think in this increasingly open global economy, with increased reliance on capital flows, the rules and linkages between money supplies and prices have become even more complicated. Technology and the use of different kinds of monies for transactions also complicates the relationship between money supply and inflation overall.

When we compare national inflation rates we are comparing apples with apples. Whatever the new forces are that are interposing themselves between the money supply growth and inflation, are occurring throughout the global economy and having more or less the same effect on price developments everywhere. Central banks currently are trying to decide how much they can introduce more stimulus without risking the spillover to more inflation.

While the chart of money supply shows what's going on with money supply and we been warned about the effects of excess money growth on the price level, there is another, perhaps greater, risk than money growth. Countries have also been experimenting with policies of quantitative easing: the Federal Reserve in the United States, the Bank of England, the Bank of Japan and the National Bank of Switzerland, all have substantially ballooned the central bank balance sheets to an even greater extent than money supply begins to hint.

There are great concerns of what happens when central banks began to unwind these policies. Although I think what that really means is that there are great concerns about what happens when economic conditions normalize and these excess reserve conditions begin to have that effect that we would construe as a normal impact on the economy requiring central banks to take countervailing actions.

Just today North Korea has asked that countries begin to think about some kind of global approach to what happens when United States actually begins its tapering activities and then eventually does what it needs to do to unwind the effects of its massive quantitative easing program. There will be international repercussions. The Fed won't be the only central bank with a balance sheet bloat to unwind.

You'll remember that the initial impact of quantitative easing was to weaken the dollar and that led Brazil, and other BRIC countries, to scream bloody murder. In reaction, Fed Chairman Ben Bernanke urged to them to provide their own stimulus and lower their own domestic savings rates. This argument (that will never be settled!) is that the US deficit is in some sense the residual outcome of other countries running surpluses that are too large because they pursue strategies of export-led growth. In a monetary system with the dollar as the center country the US will be what economists call the 'N-minus-one' country and will soak up whatever is the residual of other countries actions. The Chinese have pushed back against this argument for a long time. However, with the financial crisis in tow, with US companies flush with funds on their balance sheet, with US banks having billions upon billions of dollars of excess reserves (which they choose not the lend), the question remains why is the US sucking and one half of one trillion dollars per year or more in capital flows? Why?

Surely the US has plenty of capital and liquidity? It has no inability to satisfy financial needs. But, of course, the real reason the US does this is because it needs to finance its trade deficit not because it needs more capital inflows. The US does not need more 'capital', it needs more foreign currency to pay its bills or for the foreigners it increasingly owes to hold more dollars. The last thing the US needs is more capital inflows - or more foreign debt. Interest rates already are low and investors are scrambling to figure out what to do with their monies. The Fed's tilt on quantitative easing which is in fact a policy that leans heavily on the credit channel, is to scoop up most of the highly rated and safe financial assets and force the private sector to make decisions to engage in more risky lending. Foreign inflows are not a solution to the problem.

These capital flows often bring foreigners into markets that they understand less well than they should. To the extent that foreign monies are plowing into countries less for the reason of making a certain investment return than for the reason of pursuing a national macro-economic objective of pegging their exchange rate, the more likely it is that the monies invested are not invested productively.

For now problems, risks and uncertainties in the credit side of the market are constraining bank lending and risk-taking in securities markets. Banks, for their part, are lending more cautious because they are wary of changes that might come from ongoing legislation. Lawmakers are trying to solve the too big to fail problem as well as to make sure that banks are well enough capitalized so that the problems of the last financial crisis do not re-visit us.

This explains why the economic recovery is so much less than robust. We have not simply put our shoulder to the wheel to try to advance economic growth as fast as possible. We have been dealing with the problems caused by the past financial crisis and recession. In addition to dealing with those issues we have also been planning ahead, trying to reconfigure our economy and financial environment so that it is safer in the future. It's a little bit like trying to drive your car and to repair it at the same time.

This week has put the Federal Reserve in the limelight with the Federal Reserve Chairman's biannual presentation on monetary policy in front of the House and Senate financial committees. About the only thing that is clear in the wake of these testimonies is that the Fed really doesn't know what it's going to do yet. By that I don't mean that it's confused but that is still keeping its options open since there is still some dissent within the Fed about what the Fed's role should be and there is still considerable uncertainty about the economy - both domestic and global- as well as uncertainty about the US fiscal agenda that will be faced in the second half of the year.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief