Global| Mar 21 2017

Global| Mar 21 2017An Excessive Price Rise Slaps the U.K. Upside the Head- Has Carney Lost Control?

Summary

The U.K. inflation rate moved up above the BOE's 2% threshold for inflation, surprising markets. Bank of England Governor Mark Carney reacted to the report, saying that it was important not to overreact to economic data for a single [...]

The U.K. inflation rate moved up above the BOE's 2% threshold for inflation, surprising markets. Bank of England Governor Mark Carney reacted to the report, saying that it was important not to overreact to economic data for a single month.

The U.K. inflation rate moved up above the BOE's 2% threshold for inflation, surprising markets. Bank of England Governor Mark Carney reacted to the report, saying that it was important not to overreact to economic data for a single month.

True enough.

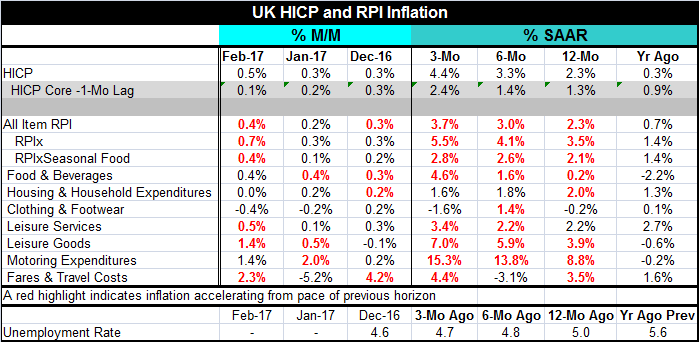

But the table below also speaks the 'truth' and it shows that the pace of price increases is steadily accelerating and doing so for a broad group of RPI categories as well as for the headline.

Acceleration! Seat belts, please!

The RPI, the RPIx and the RPIx-excluding seasonal food all show accelerating inflation. Of the seven separate independent RPI categories, only three fail to show a steady expansion in their inflation rates on all horizons from 12-month to six-month to three-months. And of those same seven categories, five already are showing price gains at 2% or in excess of 2% (Danger, Danger, Mark Carney, Danger!). Year-on-year gains are highest for motoring expenditures (8.8%), leisure goods (3.9%), fares and travel costs (3.5%), leisure services (2.2%), and housing & household expenditures (2%). Falling short of a 2% year-on-year gain are food & beverages (0.2%) and clothing & footwear (-0.2%).

Two inflation pulses

The U.K. is battling the two-headed inflation hydra of high/rising oil prices and a weak pound sterling. But each of these two elements has probably put its respective largest move behind it. Both of them create an inflation pulse more than inflation. When currencies fall, there is a pass-through into domestic prices of the subsequently higher import costs. Once the new import-cost pricing is fully passed through, the 'inflation pulse' ends. Similarly, oil prices create a once-and-for-all rise in the price of oil (if the gain sticks of course!); that also passes through to the domestic price level then stops having an impact once it is reflected in the new structure of (higher) domestic prices. The key for the central bank is not to accommodate the increase in prices and to keep expectations aligned with the past inflation path so that the incipient inflation impulse does not spread. Carney is trying to keep expectations in line with his commentary. Moreover, there is already some backsliding on oil prices and less than full clarity that OPEC is going to be able to implement and defend the new higher price level for oil that has been developing. Wildcat producers in the U.S. are adding rigs each week and increasing their output, putting more pressure on the OPEC cartel's already slow-acting output restrictions.

Inflation...still not a real problem but an issue to be managed

Just as the ECB has argued that signs of true inflation are hard to find, Carney sees the same sort of (temporary) forces in train but with an added currency kicker that has magnified as well as broadened the overall inflation impact. For the U.K., there is another difference. Unlike the EMU, the unemployment rate is extremely low. Germany has a very low unemployment rate but not all of the EMU. So the U.K. has more of a resource constraint that could also come into play than what the ECB has to weigh and balance. However, Carney is not so concerned about the low unemployment rate because there is a Brexit shock waiting in the wings and he has championed the cause for more stimulus ahead of the Brexit event and transition. Just today Goldman Sachs announced that it would be 'sponsoring' an investment banker migration out of London. Hundreds of people are reported to be in the process of being transferred out of London. Goldman has decided to implement its Brexit strategy. Goldman is putting its contingency plan in place now rather than waiting. The more that firms do this ahead of time, the more that Carney will be right and the more that the U.K. economy will need more stimulus not less or at least a better plan 'B' (Brexit).

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief