Global| Sep 01 2020

Global| Sep 01 2020A Potpourri of Problems; Has the Worm Turned? If So, in Whose Apple?

Summary

Many analysts think stock markets are walking on glass or eggshells, but they act like they are walking on sunshine. Alan Greenspan, former U.S. Federal Reserve Chairman's best-remembered remark about the U.S. stock market was his [...]

Many analysts think stock markets are walking on glass or eggshells, but they act like they are walking on sunshine. Alan Greenspan, former U.S. Federal Reserve Chairman's best-remembered remark about the U.S. stock market was his saying it was 'irrationally exuberant.' And while the comment did presage a stock market drop, stocks continued to run up for the next three years.

Many analysts think stock markets are walking on glass or eggshells, but they act like they are walking on sunshine. Alan Greenspan, former U.S. Federal Reserve Chairman's best-remembered remark about the U.S. stock market was his saying it was 'irrationally exuberant.' And while the comment did presage a stock market drop, stocks continued to run up for the next three years.

Globally markets continue to recover but on the economic front there is a world of hurt, pain and a progression in the wrong direction for a number of key variables.

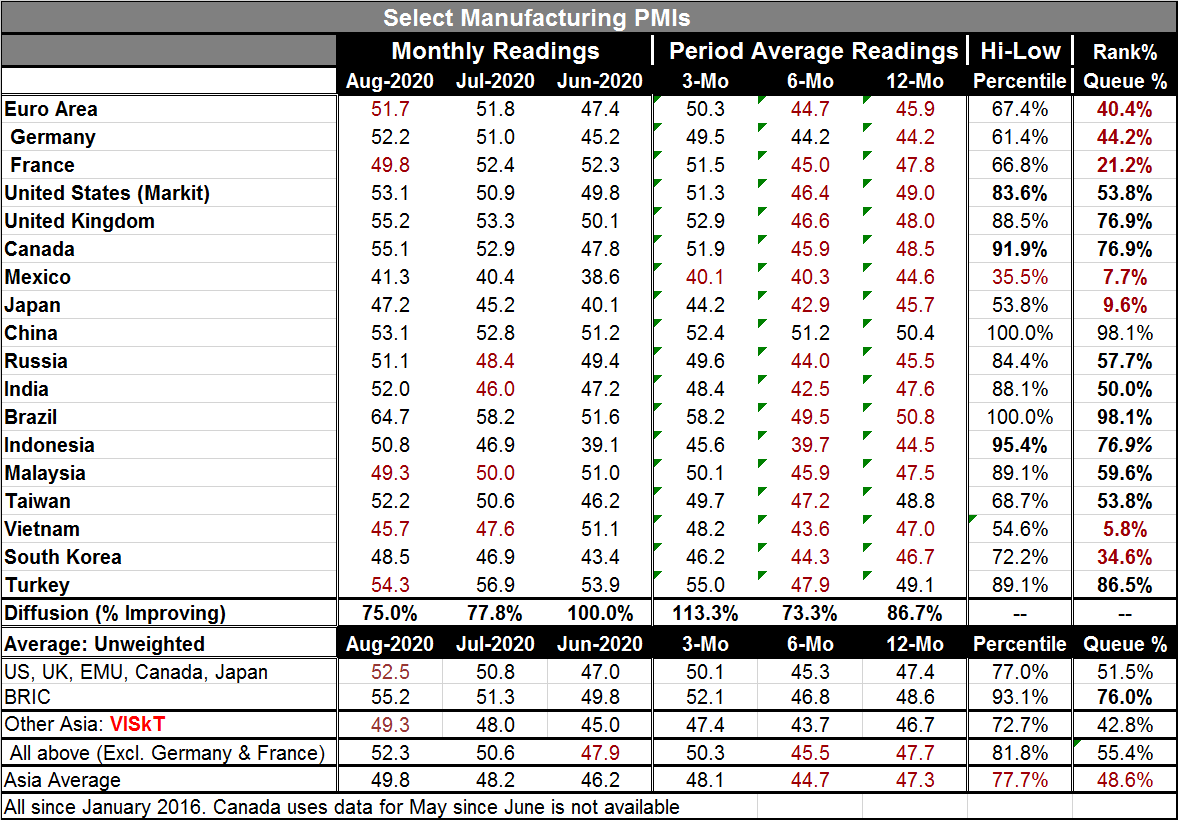

• Globally manufacturing PMIs (a slew of them were just released today) show a proliferation of readings that remain too low for comfort despite an overwhelmingly broad, but very slow arc, to higher levels.

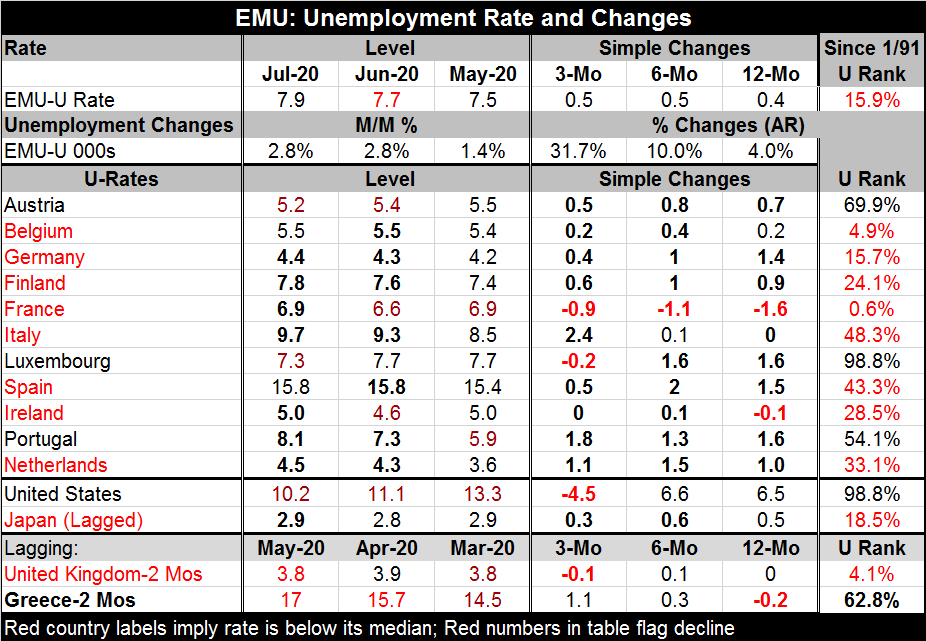

• The unemployment rate has just risen in Japan and is rising in the EMU- and on an all too broad front. In the U.S., the progress in reducing jobless claims has slowed and the lack of another supplemental help-package for the dislocations created by virus-fighting raises a red flag warning in the U.S. for the future.

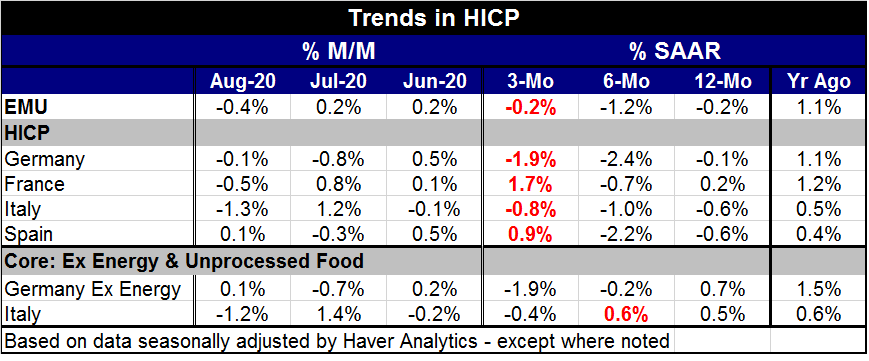

• In the EMU, very disturbingly, the flash HICP targeted inflation measure by the ECB has just soured to fall on a year-on-year basis. The global economy has been fighting off inflation undershooting for a number of years, pretending it was a minor nuisance. Have central banks been ignoring a more significant problem, that of oncoming deflation?

• While many fear that the global economy faces or will face a kick up in inflation due to excessive stimulus in the face of the virus, the evidence on the ground at our feet warns of deflation and weak growth. Is that a new more nefarious old enemy creeping into the picture: Stagflation?

The Trend in Unemployment

Globally unemployment rates have risen. Table “EMU: Unemployment Rate and Changes” shows 15 countries with 12 demonstrating net increases in unemployment over the last 12 months (France, Ireland and Greece are the exceptions). And while unemployment rates stabilized in the wake of the bite of coronavirus, the remedies nations chose to pursue meant that not all experiences are the same. In the U.S. due to a different way of handling support for the affected, the unemployment rate soared and has since dropped sharply shaving off 40% of the gross rise in the unemployment rate. In the EMU, the virus meant that unemployment rates largely stopped falling and since began rising. Among 11 of the longest standing EMU members, unemployment rates are up on a net basis over three months in all but two of them (France and Luxembourg; I omit Greece from this count and consideration because of lagging data).

The EMU remains a hodge-podge of events with the ranking of the current unemployment rate by country since 1991 and the level of the unemployment rate in July having an R-squared relationship of 0.04. The proportion of the variance in level of the unemployment rate across 11 long-standing EMU members explained by the rank standings of unemployment across countries is less than one-half of one percentage point! That result is stunningly tiny.

Let me explain what this is and what it means. First of all, if EMU member economies moved together, countries would be on their unemployment highs and lows together. They are not. The ranking compares at the same points in time the position of the unemployment rate relative to where it has been historically. Instead we see things like this: Luxembourg, with the highest ranking of current unemployment (98.8 percentile), ranks as fifth highest in terms of the current level of its unemployment rate. France, with a 0.6 percentile standing for its unemployment rate level (very low), ranks 6th in terms of the level of its unemployment rate across this group in the EMU.

This simply is another way of pointing up that there remain huge structural differences within the EMU and among even is long-standing members. Rules and regulations meant to imbue a common market with more homogenous rules have not brought similar functioning to the various labor markets in the EMU. That is troublesome for several reasons: (1) It makes making monetary policy difficult since not all countries are in the same relative or absolute positions when policy decisions are made. (2) Politically it tends to divide EMU members according to where they are in the unemployment cycle. Right now the German rate is at 4.4% and is among the lowest 15% of all unemployment rates Germany has experienced since reunification. Within the EMU, German unemployment rate ranks as the lowest of all. The French rate is at 6.9%, much higher and ranks as the 6th highest in the EMU, but for France its unemployment rate raw score is also among the very lowest it has experienced. France might find the same monetary policy Germany wants for absolute and relative reasons agreeable because of a relative reason. The French rate at 6.9% is very close to Luxembourg's rate of 7.3%. But Luxembourg's time-series ranking for that rate has it among the highest 2% it has experienced and that is the highest relative rate (unemployment rank) in all of the EMU. How can 7.3% be so different from 6.9%? The reason is that the EMU is not well-integrated.

Even so across the EMU on balance, unemployment has crept up at a time that the EMU-wide target variable for inflation is now negative year-over-year. There has been a lot of disagreement about the value of negative interest rates in the EMU. And the Germans for some time have been arguing to get rates back toward normal or at least above zero. But now with inflation negative, the move to negative rates by the ECB looks that much more prescient.

The flash inflation news for the EMU shows the EMU HIPC with prices weaker over 12 months with that results echoed by Germany, Italy and Spain. For the two early reporting core or ex-energy measures, we see positive numbers in both Germany and Italy year-over-year. For now deflation is a characteristic of the headline but not of broader price gauges that exclude energy or energy and food.

Manufacturing PMI Data

Also released today in a whirlwind of economic reports that could make your head spin before you could digest them all, was the manufacturing PMI data from Markit. These reports show widespread but very slow improvement with lingering weak readings. Japan, for example, has sixteen months in a row of its manufacturing PMI below 50 and in August it is still at 47.2.

The process of recovery is underway. But virus reinfections are occurring, unemployment gains may be backtracking and elsewhere job dislocations continue to rise. Economies are not nurturing much in the way of forward momentum to cruise on if things get tough or tougher.

Both the manufacturing and services areas are struggling across these economies. Markets remain optimistic that governments will continue to pour aid in when aid is needed. But in the U.S., we already see politics at work and interfering with that process.

On balance, the day's data are not very reassuring. The global economy is not having a 'V-shaped' recovery. Even the Baltic dry goods index that had made a strong initial rise after an ongoing slide has gotten caught up with a sideways motion.

Getting away from the numbers, what we see in the real world and in our everyday lives informs us too. Many people are still scared or wary. Behaviors have changed. Consumption patterns are strongly and strangely altered. Some industries are simply not coming back. Others are coming back slowly. In New York, for example, restaurateurs have made peace (some of them have) with outdoor dining, but as John Snow knew, winter is coming. At some point, outdoor dining no longer works.

Despite a GROWING RECOGNITION that the virus really does not kill that many and that it targets the weak therefore remains something with a fear factor that exceeds the real risk. And because the exact nature the virus is unknown, some fear even simple infection even if it will not kill them. The data on this are uneven. But it is fair to say that now policy and behavior are more driven by fear than fact and that comment is based on SCIENCE! Few people really know the science or the real risks. Many fail to understand that science has controversy. Science has many things to say on the subject of this virus NOT ALL WITH ONE VOICE. The stifling of other voices has NOT been productive and has led Democrats to excoriate Trump even for some very reasonable and science-supported comments. Science is still learning. But when it learns more, can WE unlearn what it previously led people to fear that so remarkably altered behavior? Can science put the toothpaste back in the tube?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief