Global| Feb 25 2010

Global| Feb 25 2010A Pause And Backtrack In EU/EMU Growth In February

Summary

Manufacturing orders are up by 0.8% in December but the sequential growth rates do not show that the growth of orders continues to accelerate. MFG sales are also slowing as capital goods and intermediate goods sales rates over three- [...]

Manufacturing orders are up by 0.8% in December but the sequential growth rates do not show that the growth of orders continues to accelerate. MFG sales are also slowing as capital goods and intermediate goods sales rates over three-months are weaker than sales rates for six months

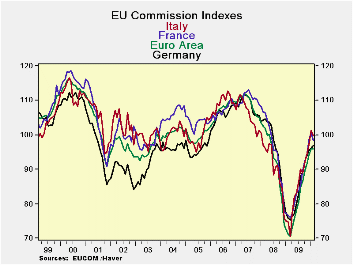

The overall EU index of confidence rose in February but the EMU index edged lower. Among the largest EU/EMU nations France and Italy saw declines. Germany posted a gain of 0.9% in the month while Spain‘s index advanced by 1.2%. The UK saw confidence edge up by a tiny 0.1%.

The overall EMU confidence measure stands in the 62nd percentile of its range but if we position it by queue among past values it stands in the bottom third among all confidence measures since 1989. Oddly the strongest relative standing of any sector is by retailing which is in the 64th percentile of its range and in the 57th percentile of its queue. The industrial sector and consumer confidence in their respective 50th to 55th range percentiles and in their respective 29th to 34th queue percentiles. The service sector stands just below its range mid point in its 49th percentile but sags back to a 23rd percentile standing in its queue

The difference between the range and queue percentiles tells us something about the density of the distribution of values for these readings. The queue percentile gives us a good fix on where the index stands compared to where it has been historically since a queue standing of 54% says that the indicator is weaker than this 54 percent of the time and stronger only 46 percent of the time.

The range standing simply positions the current reading between the best and worst readings in some historic span (since 1989). For now the range readings are higher than the queue readings because the current levels are elevated substantially from recession lows and the lows skew the range. But compared to the full spectrum of readings the current levels are not yet higher than they have been on average except for retailing (in the 57th percentile of its queue). So Europe is still lagging in its recovery. It is well short of getting back to neutral even though the recovery has slowed and this month has brought slippage to the EMU reading.

All the large countries continued to show overall sentiment readings that are below their queue midpoints, although four exceed their range midpoints. The highest queue standing is oddly and surprisingly in Italy with confidence in the 44th percentile of its queue followed by Germany, France and the UK all of which are in the 37th percentile of their respective queues. Spain is in the 16th percentile; EMU is in the 26th percentile.

So EMU is better than this nearly 75% of the time and this is after a 10 straight monthly rises in sentiment. That metric should stop you in your tracks. Even though the overall EMU reading stands in the 55th percentile between its worst and best readings, the ‘queue standing’ is just above the lower quartile. In addition to this Europe has big problems with Greece. You can see the dour mood in Spain with its 19% unemployment rate and then there is beleaguered Portugal. The ECB is on the cusp of new leadership – who will that be? Will it inspire stability? Will it be a tough inflexible guy like Weber from the Bundesbank or someone else? Europe is just a series of question marks. And if it backslides who does the US export to? The US has emerging troubles of its own

Welcome to 2010.

| EU Sectors and Country level Overall Sentiment | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EU | Feb 10 |

Jan 10 |

Dec 09 |

Nov 09 |

%tile | Rank | Max | Min | Range | Mean | By Queue Rank% |

Average Level |

| Overall Index | 97.4 | 97.2 | 95 | 91.5 | 62.4 | 166 | 115 | 68 | 47 | 100 | 33.9% | 100.5 |

| Industrial | -13 | -13 | -16 | -19 | 56.5 | 178 | 7 | -39 | 46 | -8 | 29.1% | -7.8 |

| Consumer Confid | -14 | -13 | -14 | -15 | 52.9 | 165 | 2 | -32 | 34 | -11 | 34.3% | -11.1 |

| Retail | -5 | -3 | -6 | -6 | 64.5 | 108 | 6 | -25 | 31 | -6 | 57.0% | -5.7 |

| Construction | -32 | -34 | -33 | -32 | 21.7 | 203 | 4 | -42 | 46 | -17 | 19.1% | -17.1 |

| Services | 0 | -2 | -2 | -9 | 49.2 | 123 | 32 | -31 | 63 | 13 | 23.1% | 12.8 |

| % m/m | Feb 10 |

Based on Level | Level | |||||||||

| EMU | -0.1% | 2.0% | 2.4% | 95.9 | 55.4 | 185 | 116 | 71 | 46 | 100 | 26.3% | 100.5 |

| Germany | 0.9% | 0.6% | 1.6% | 97.0 | 47.8 | 158 | 121 | 75 | 46 | 101 | 37.1% | 100.6 |

| France | -1.9% | 1.7% | 4.1% | 98.4 | 54.4 | 157 | 119 | 74 | 44 | 100 | 37.5% | 100.5 |

| Italy | -1.7% | 4.3% | 2.6% | 99.7 | 58.6 | 139 | 120 | 71 | 50 | 100 | 44.6% | 100.5 |

| Spain | 1.2% | 0.3% | 1.3% | 90.1 | 41.2 | 210 | 116 | 72 | 44 | 100 | 16.3% | 100.2 |

| Memo:UK | 0.1% | 3.4% | 6.9% | 98.3 | 66.1 | 158 | 115 | 65 | 50 | 100 | 37.1% | 100.2 |

| All since Feb 1989 | 251 | -Count | Services: | 160 | -Count | |||||||

| Sentiment is an index, sector readings are net balance diffusion measures | ||||||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.