Global| Aug 14 2019

Global| Aug 14 2019A Global Economy Beyond the Repair of Crazy Glue

Summary

It starts with weak IP in Europe Industrial output in the EMU area has lost its way, falling by 1.6% in June, at a -5.2% annualized rate over three months and -2.4% over 12 months. It does manage a small (0.4% annualized) gain over [...]

It starts with weak IP in Europe

It starts with weak IP in Europe

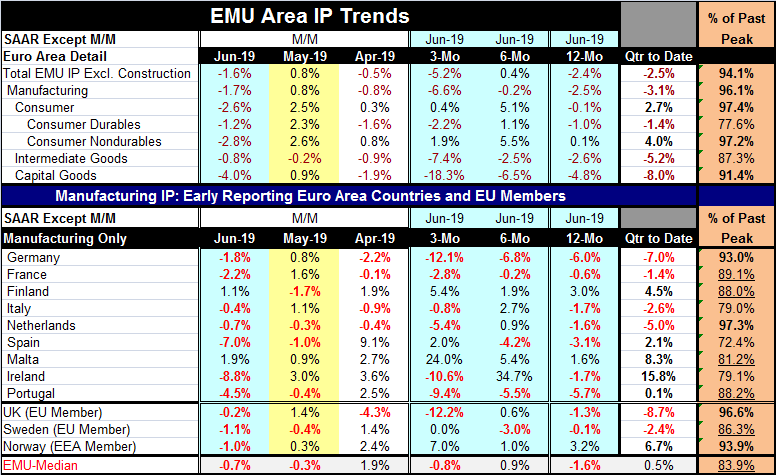

Industrial output in the EMU area has lost its way, falling by 1.6% in June, at a -5.2% annualized rate over three months and -2.4% over 12 months. It does manage a small (0.4% annualized) gain over six months, however. But GDP in the EMU is now confirmed weak. GDP in Germany declined in Q2. China just logged much weaker than expected economic numbers featuring weak output and retail sales and with that and an ongoing trade war fixed income markets are off to the races. By that, I mean fixed income instrument prices are rising, which means that yields are falling and falling fast they are.

Markets in disarray

The U.S. is the bellwether for all this with the 30-year U.S. Treasury bond yield at its lowest yield in the Post-War period (described by some as ‘the lowest yield ever'…but I don't have data to confirm that). The 30-year bond was not issued for a while and began to be reissued on a regular basis in 1977 compounding confusion about what its historic data really mean.

Market signals in unison

Despite all sorts of denials about the yield curve and its inversion and its meaning, in the U.S. the 10-year yield fell below the two-year yield for the first time since 2007 giving off another one of the fabled recession signals joining the 10-year to three-month bill inversion. It may not be a chorus of voices, but it is an important duet. Tune out these sirens' song at your own risk.

Stock market feathers finally are being ruffled by these fixed income machinations. But ruffling does not occur in isolation. It is simply, usually, an advance signal of poor economic data to come and we already have some poor economic data on our plates and reasons to fear more in the future.

Weak euro-eco-data

In addition to weak EMU and falling German GDP, the EMU IP figures are very disappointing. All of the sectors show output declines in June. Over three months, only consumer goods output is higher boosted by consumer nondurables. Over 12 months, all sectors are lower except for the thin 0.1% gain in consumer nondurables.

Thud...thud, thud

Perhaps most disturbing is that the sector output declines in the EMU are led by capital goods where output fell with a thud on a simple one month drop of 4% in June (that's right not annualized, a simple 4% drop- that's a 60% compounded and annualized rate for those of you that like to annualize things). Capital goods output falls on all horizons and its drop is accelerating from a rate of -4.8% over 12 months, to -6.5% over six months to -18.3% over three months. Thud, thud, thud. Of course, capital goods spending drives the growth of the future. Thud. And capital spending is the vehicle for productivity to rise. Thud… and for real wages to rise. Thud. Yes, a lot of bad trends are in play in June and the year is only half-over!

Europe is broadly weak

Of the 12 EMU and non-EMU European economies listed in the table, all but two show output declines in June. Five showed declines in April and then again in May. But seven show declines over three months with the U.K. revealing a horrific pace of decline at a -12% annualized rate along with Germany. Five countries in the table show net IP drops over six months; over 12 months 9 of 12 countries show output declines.

Waiting for good dough in the EMU…and in the U.K.?

We are waiting for the ECB to launch another round of stimulus probably a new bond buying program and some rate shaving. The BOE is facing sharply weaker industrial conditions plus an inflation rate that just topped its target of 2% substantially because of weakness in the pound sterling. We have seen that happen before. The last time that imported inflation flared, it did not spread to domestic industry and inflation itself came back within target sooner than expected. But this time the Brexit threshold is expected to be breached by Halloween- and that horror firm will not star Jaimie Lee Curtis. It will be a real life event

Don't worry! I got my finger on it...

Policymakers have no magic elixir for what is ailing the global economy. Crazy Glue will not work, nor will staples or cellophane tape or even fabled fix-it-all duct tape. Monetary policy has been used and abused. Fiscal policy as yet is untried for several different reasons. In Europe because of Maastricht constraints and in Japan because the debt to GDP ratio already is so high (in fact, Japan has a consumption tax hike slated for this year). China has been contrary. It has been leaning heavily on the use of debt for stimulus so much so that it has become rather ineffective. Now many are worried about China's homemade debt bomb. It's what happens when the Crazy Glue sticks to your fingers and they then stick together impeding your ability to continue -got to be careful using that stuff. Arguably unbridled debt issuance is the Crazy Glue for the terminally crazy

Horse of a different color

Of course, the U.S. is different. It has had an expansive fiscal policy all along. Italy has made some minor use of fiscal policy after a confrontation with the EU Commission. It wants to use fiscal stimulus in a more significant way. But the EU Commission is hell-bent to enforce the arbitrary debt rules of the European Union. But Mario Draghi has suggested that Europe will not be able to get out of its situation without fiscal policy help. It is unusual for a central banker to give fiscal policy advice. But Mr. Draghi is in his sunset year. And this way he spares putting the burden of saying this on the shoulders of Christine Lagarde, his successor. And Christine, in any event, must woo over the Germans if she is to be successful so she will be in no position to spout such Teutonic heresy once in office. Germany for its part is running a fiscal surplus; Angela Merkel has just recently said it has no reason for fiscal stimulus.

So!?

The planet Germany as its own solar system

Germany is one of the hard money countries that usually pushes to enforce Maastricht rules (except when Germany itself breaks them). But right now the German economy is weak and it is running a fiscal surplus. It has room to use fiscal stimulus but instead is dragging its heels and even running a counter-intuitive contractionary fiscal policy. It is not clear what will ‘give.' The ECB can shave interest rates and it can ramp up bond buying, but a pending dispute against bond buying in Germany could take Bundesbank participation out of the mix. That would severely crimp the effectiveness of any bond buying stimulus for the EMU. Apparently planet Germany's gravitational pull can throw the entire EMU system out of its orbit.

Paying the piper

The global economy is now paying the price for its continual reliance on fiscal policy, debt creation, and government spending and for its overreliance on stimulative monetary policy. How could this happen?

How we got here...Globalism gone bad

You can dispute this analysis, but it is clear to me that globalism done badly is to blame. Under good globalism, all countries would have participated in better-balanced growth. Exchange rates would have been market-determined and would have moved to more or less keep current accounts in balance as trade barriers continued to fall. Instead, developing countries targeted and controlled their exchange rates and acquired most of the growth. The U.S. became an export target because of its high income and wealth. Developing countries set low targets for their exchange rates to enhance their competitiveness as they attracted investment to export more cheaply to the U.S. Fast-developing countries did not see their exchange rates rise. The development of their local domestic economies was retarded and consumption was suppressed. As a result, the developing economies ‘recycled' their surplus dollar back to the U.S. to support a too-strong dollar and to cement their own growth. The U.S. became a Mecca of over-consumption. Developing Asian economics became production centers with low domestic consumption. The U.S. and other economics had to grow consumption to create growth. A combination of low interest rates and fiscal stimulus kept growth afloat while the U.S. underwent blood-letting through its current account. Europe too underwent some of the same pressures and was forced to push even harder on interest rates since fiscal policy there was placed in the penalty box by the EU Commission.

Trade war!

These circumstances brought us to where we are now and they also explain that the trade war has been a reaction to these events. It is and was totally predictable since economic imbalances were piling up instead of being dealt with in a competitive market determined foreign exchange market these conditions were simply left to spread their uneven effects.

A war with an objective; not a thoughtless conflict

The Trump Trade War was and is intended to bring China's polices into alignment with true competitive conditions. It is also meant to be a model for other less than free-trade compliant countries to get in step. China's reluctance to deal, after seemingly being very willing to make modifications, has now created an impasse. Xi thinks he can wait Trump out and maybe deal on trade with Democrats. But based on current market data, no one has that much time. Markets can tell. They smell a rat and they are beginning to get prices ready for rat infestation. And despite all the safeguards enacted in the last downturn, recessions always expose excesses. There will clearly be some nasty surprises ahead. And China will sponsor many of them despite being ‘Communist.' If China wants to be part of a global trading system, it must trade and act fairly. No one will dispute that. And while everyone will owe Trump a debt of gratitude for his efforts to reform China, no one will like the cost of it all. No one will pat him on the back. But there is no Crazy Glue for a broken global growth model.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief