Global| Jun 07 2019

Global| Jun 07 2019A German IP Report That Will Send Chills Up Your Spine

Summary

Germany's industrial production is lower across all sectors in April. It is also falling across all sectors over three months, over six months and over 12 months. Headline as well as manufacturing IP for Germany shows that IP is [...]

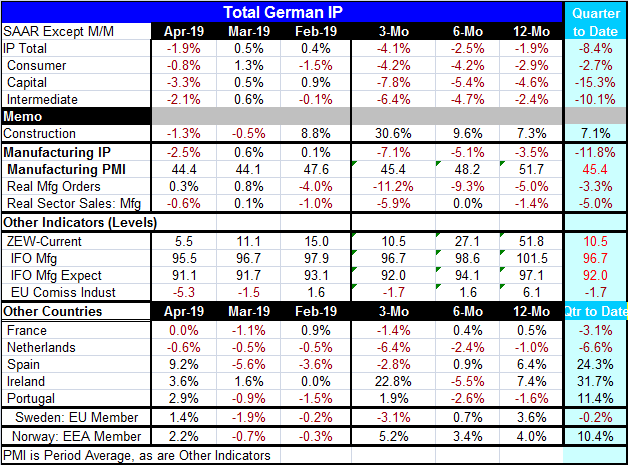

Germany's industrial production is lower across all sectors in April. It is also falling across all sectors over three months, over six months and over 12 months.

Germany's industrial production is lower across all sectors in April. It is also falling across all sectors over three months, over six months and over 12 months.

Headline as well as manufacturing IP for Germany shows that IP is falling at an accelerating pace over shorter internals. This is most disturbing. German average PMI readings also are declining sequentially. Real orders are sequentially weakening. Real Sales are not (quite) in that same circumstance, but they are falling in two of three periods and are flat over six months. As far as trends for hard German industrial measures: real output, real sales and real orders, are concerned there is little here that is reassuring and a lot that is disturbing.

The third panel of data down is a compendium of German business indicators or surveys; all of them show sequential weakening as well.

Turning to other early-reporting EMU members and to other European countries, while output trends are not as uniformly negative for all European nations, for France, the Netherlands, Spain and Sweden all show sequential slowing from 12-months to six-months to three-month. Ireland is contrary with very strong three-month growth; Norway show persistent expansion and a tendency to acceleration Portugal shows some life over three months, mostly on the back of strength in April.

The quarter-to-date column (final shaded column) calculates the percentage change of April over the Q1 period average centered and compounded. For PMIs, we display simpler calculation of April less the Q1 average reading. Regardless of the metric, all German indicators show a weaker April than Q1 average. Either the April PMI level is lower or there are declines in other readings producing often sharply contracting rates of growth QTD.

Even for the rest of Europe, three of seven early reporting nations show output falling on a quarter-to-date basis. Negative QTD rates hold sway in EMU members France and the Netherlands as well as in EU member Sweden. Spain and Ireland both EMU members contrarily show strong gains QTD with growth rates in the 25% to 30% habitat. Portugal (an EMU member) and Norway have QTD output expanding at a double-digit pace. However, for both of them (as well as for Spain, to a lesser extent), the QTD expansion is created substantially by sharp output reductions in March and April as much or more than such a strong expansion in April.

The whole of the global economy is affected by the ongoing trade war. Even before the tariffs bite, there is an expectation that they will bite and that helps to freeze investment and to chill activity, except for flows that might speed up to try to beat the imposition of a tariff. But in the Americas, the threatened tariffs on Mexico came so fast that it has been impossible to for firms to get goods across the border ahead of the tariff imposition if the current deadline holds.

On balance, there is a lot of weakness in the mix. Today a shockingly weak U.S. jobs report is also on offer. There are as yet unknown tariff effects in play but what we do know is that they will not be stimulative effects. Still, central bankers are watching and waiting…when do they actually begin thinking? I ask this because that will turn the waiting to action. Waiting to act on bad news you know is coming is an incredibly hard-headed way to make policy…and it's wrong.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief