Global| Sep 26 2003

Global| Sep 26 20032Q U.S. GDP Growth Revised Up Again. Profit Surge Lessened But Nonfinancial Profits Raised

by:Tom Moeller

|in:Economy in Brief

Summary

US economic growth was revised up slightly to 3.3% for 2Q03 from 3.1% reported last month and from 2.4% estimated in July. The upward revision beat Consensus expectations for 3.1% growth. Revisions were mostly technical and were the [...]

US economic growth was revised up slightly to 3.3% for 2Q03 from 3.1% reported last month and from 2.4% estimated in July. The upward revision beat Consensus expectations for 3.1% growth. Revisions were mostly technical and were the last before "benchmark" revisions later this year.

The upward revision reflected less drag from inventory reductions and somewhat faster growth in domestic final demand, up at a 5.1% rate.

Growth in fixed investment was ticked up slightly to 7.1% due to raised growth in nonresidential structures of 4.2%. Expenditures on equipment and software grew at an unrevised 8.2% rate. Growth in Federal defense spending was revised little at 45.8%, accounting for over half of the economy's growth last quarter.

Personal consumption expenditures growth was unchanged at 3.8%. Purchases of motor vehicles surged at a 33.5% rate and buying of furniture & household equipment rose at a 17.9% rate.

Growth in corporate profits with adjustment for depreciation (CCA) and inventory valuation (IVA) was revised down slightly to 45.7% (AR, 14.3% y/y) from 50.8%. The spike reflected a huge surge in the depreciation allowance. These "operating profits" rose 72.1% (AR) after tax.Growth in operating profits after tax at nonfinancial corporations was revised up to 71.8% (AR, 21.3% y/y) from 64.7% estimated last month. This figure is derived from the income side of the National Income and Product Accounts.

Inflation was revised up slightly to 1.0%. The price index for domestic final demand grew at a 0.3% rate (1.7% y/y).

"The 2001 Recession: How Was It Different and What Developments May Have Caused It?" is the question explored in this paper from the Federal Reserve Bank of St. Louis.

| Chained '96 $, % AR | 2Q'03 (Final) | 2Q'03 (Prelim) | 1Q'03 | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|---|

| GDP | 3.3% | 3.1% | 1.4% | 2.5% | 2.4% | 0.3% | 3.8% |

| Inventory Effect | -0.7% | -0.9% | -0.8% | -0.2% | 0.6% | -1.2% | 0.1% |

| Final Sales | 4.0% | 4.0% | 2.3% | 2.7% | 1.8% | 1.5% | 3.7% |

| Trade Effect | -1.3% | -1.2% | 0.8% | -0.4% | -0.7% | -0.2% | -0.7% |

| Domestic Final Demand | 5.1% | 5.0% | 1.4% | 3.1% | 2.4% | 1.6% | 4.3% |

| Chained GDP Price Deflator | 1.0% | 0.9% | 2.4% | 1.5% | 1.1% | 2.4% | 2.1% |

by Tom Moeller September 26, 2003

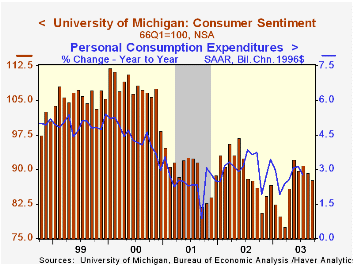

The University of Michigan’s consumer sentiment index for September fell more than indicated in the mid-month report. The figure for the full month fell to 87.7 versus the mid-month read of 88.2 and versus 89.3 in August. Consensus expectations had been for a reading of 88.5.

During the last five years there has been an 83% correlation between the level of consumer sentiment and the y/y% change in real PCE.

The Index of Consumer Expectations fell for the fourth consecutive month to the lowest level since April.

The read of Current Economic Conditions fell for the second month.

The University of Michigan survey is not seasonally adjusted.It is based on telephone interviews with 250 households nationwide on personal finances and business and buying conditions. The survey is expanded to a total of 500 interviews at month end.

| University of Michigan | Sept | Aug | Y/Y | 2002 | 2001 | 2000 |

|---|---|---|---|---|---|---|

| Consumer Sentiment | 87.7 | 89.3 | 1.9% | 89.6 | 89.2 | 107.6 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief