Global| Dec 31 2013

Global| Dec 31 20132014: An Upswing At Last?

Summary

This is my last research report of 2013. In it I look ahead to 2014. The chart and table in this report provide a basis for thinking of the trends that are set in place as 2013 ends and projecting them into the year ahead. We have [...]

This is my last research report of 2013. In it I look ahead to 2014. The chart and table in this report provide a basis for thinking of the trends that are set in place as 2013 ends and projecting them into the year ahead.

This is my last research report of 2013. In it I look ahead to 2014. The chart and table in this report provide a basis for thinking of the trends that are set in place as 2013 ends and projecting them into the year ahead.

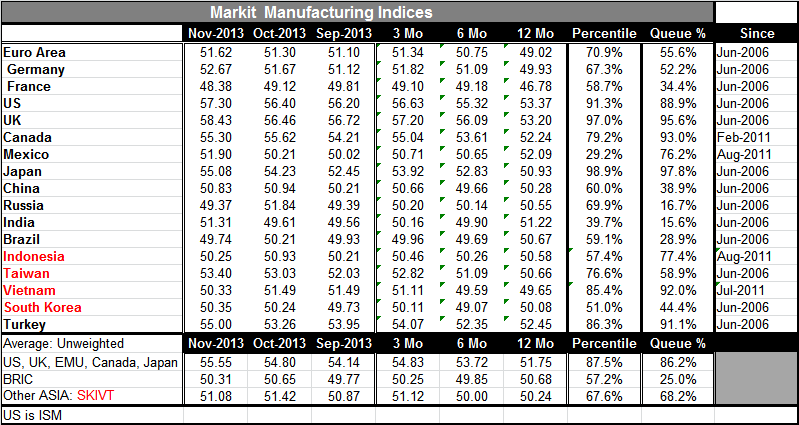

We have known for some time that Europe has been on an improving trend. But with each passing day its upswing looks more solid. In the United States, there have been hints of improvement, but job growth remains a major question mark. Globally the goods sector is recovery much more fully than the services sector. And since the goods sector is the high productivity sector job growth lags. In EMU, for example, the manufacturing sector PMI stands in the 75th percentile of its historic range, a quite respectable showing, while the services PMI languishes at the 54th percentile of its range, better than its current showing about half the time.

As long as domestic demand in the developed countries languishes, the rest of the world will find growth harder to come by. Taiwan and Brazil are examples of two highly export oriented countries where their domestic growth has been held back because a weakness in export markets. Indeed as a group the BRIC countries are exceptionally weak. China has been devastated by the slowdown in its former target export markets. It sees the shift as permanent and has begun to wean itself away from export-led growth to stimulate growth at home. One of the broader implications of this is that there will be more global inflation.

Up to this point in time, China had been trying to generate economic growth- output growth- by ramping up its production facilities and employing its citizens to satisfy the demands of consumers in other countries. Bizarrely, as China `developed' the share of consumption in GDP fell rapidly. More bizarrely, China amassed huge foreign exchange reserves even though its needs to spend money at home were pressing. China did not allow its peoples' purchasing power to improve as it developed. Instead it held the yuan low to help it effect export penetration and build up more foreign exchange reserves. If you have ever studied macroeconomics and thought about equilibrium, China could not have been doing more to disrupt the notion of equilibrium. It had growing international trade surpluses and it did not let its currency rise. It had growing GDP and it did not spread the wealth among its citizens. It had rising foreign exchange reserves that it did not use those funds to help improve the lot of its people in a country with a great deal of poverty.

So now China, seeing demand overseas dry up, is forced to do what it should have been doing all along, improve the lot of tis people. Developing domestic demand means paying people more so they can afford to buy things. This is a 180 degree shift for China. It is already in progress and it is having the effect of raising wages in China and taking the cap off one of the most deflationary or disinflationary forces in the global economy.

Some manufacturing business already is flowing back to the United States. China is going to lose its allure as a knee-jerk cheaper place to do business. And the flaws in China, in its infrastructure and legal system, will appear as larger disincentives to companies that would locate there.

Weaker demand in the most developed countries is already having far flung impacts on the global economy itself. It has already greatly affected monetary policy and there have been different fiscal responses in Europe than in the United States. Europe's fiscal `experiments' appear to be over and with that we will see in EMU growth progress in 2014. We look for growth in the U.S. to continue as well. These developments will have positive worldwide implications. And the shifts in China mean that there will be less price discipline overall.

We look for some `real growth' to emerge in 2014, but we also think there will be real risk. As central banks shift away from highly accommodative policies, there will be more concern about traditional macroeconomic tradeoffs.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief