Asia

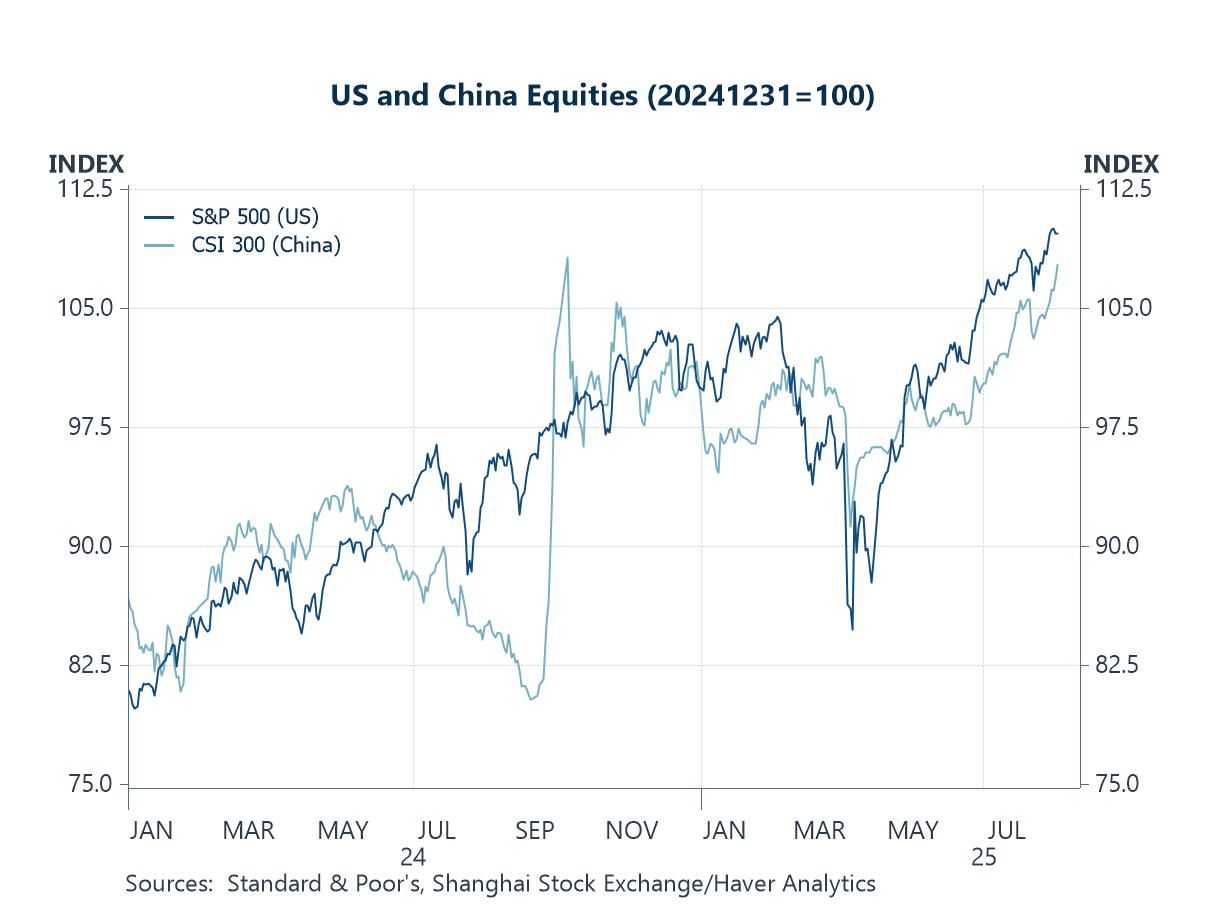

AsiaThis week, we examine recent developments in US-China trade and assess the broader implications of US trade actions for the BRIC bloc—Brazil, Russia, India, and China. Last week, the US and China extended their tariff truce by 90 days, a move welcomed by equity markets (chart 1). While this pause eased fears of renewed trade tensions, it remains temporary and fragile, with no durable resolution in sight.

As for China’s economy, July data disappointed: retail sales, industrial production, and fixed-asset investment all missed expectations (chart 2). This may signal that tariffs are beginning to bite, as earlier growth drivers—such as some front-loading of imports and one-off consumption boosts like China’s durable-goods subsidy—are fading (chart 3). Newer measures, including loan-interest subsidies, may provide some interim relief. Meanwhile, the property sector remains under heavy strain, with further price and investment declines evidenced in July (chart 4).

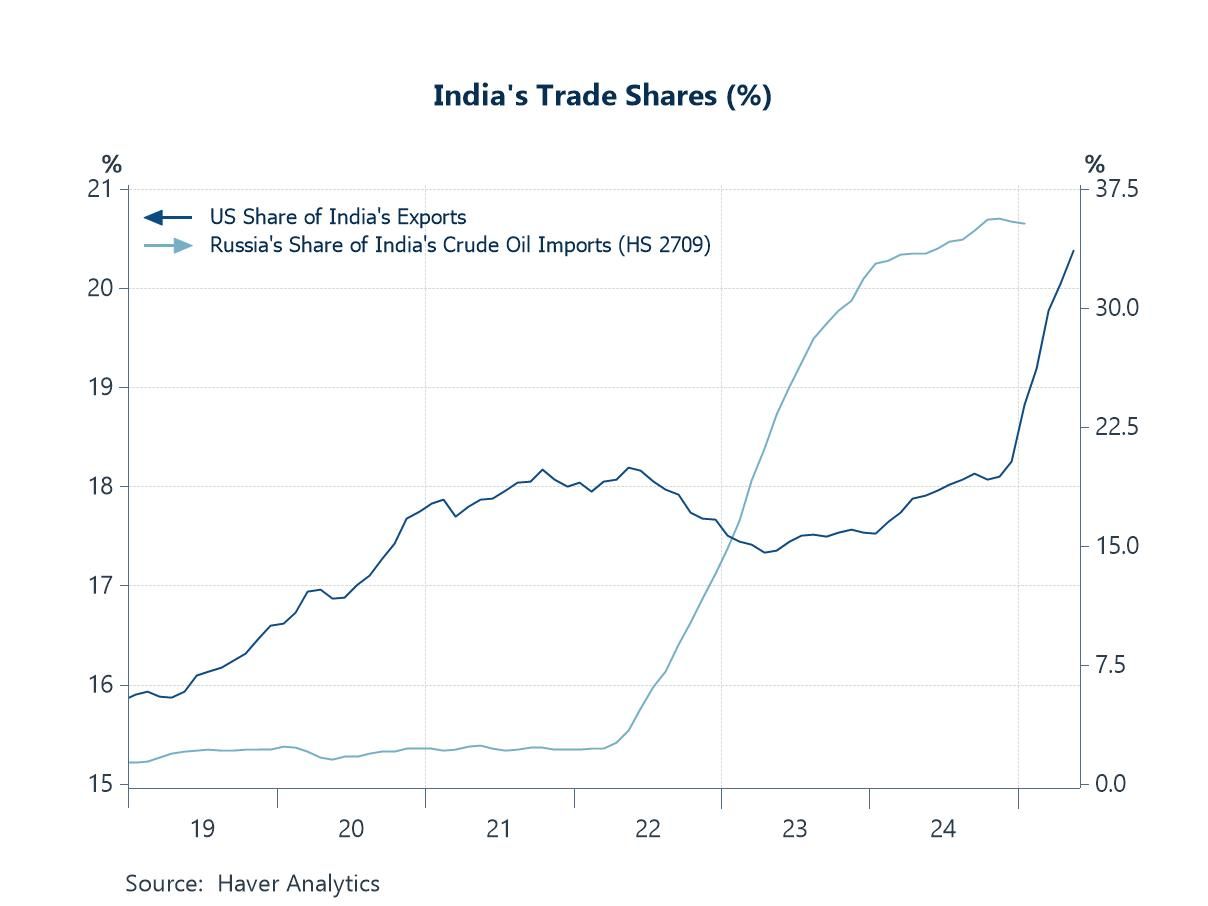

In the broader regional context, US trade measures may inadvertently push trading partners closer together, complicating Washington’s bilateral strategy. The BRIC bloc shows tentative signs of greater alignment, though this has yet to appear in data for trade flows (chart 5). China and India, however, are warming toward one another: Foreign Minister Wang Yi’s visit to India this week—focused on the Himalayan border among other issues—suggests an improving dialogue. Separately, discussions at the national level to restart direct flights between the two countries also signal a thaw. Full economic integration remains distant, but the scale of both economies suggests significant potential if relations continue to improve (chart 6).

The US-China tariff truce Last week, the US and China announced a 90-day extension to their mutual tariff truce. Although largely expected, the move still generated further equity market gains (see chart 1). This contrasts sharply with worst-case scenarios earlier this year, when tensions peaked and Washington imposed sweeping tariffs of 145% on Chinese imports — levels that would have severely disrupted global trade and growth if sustained. Instead, both sides agreed to keep additional tariffs at 10% until November 10, allowing more time to pursue a durable trade deal. Still, this is merely a pause rather than progress.