Waiting for (Tariff) Inflation...

by:Joel Prakken

|in:Viewpoints

In Samuel Becket’s renowned play, Vladimir and Estragon wait for Godot, who never arrives. It’s like waiting for the inflation impact of recent tariff increases…or is it?

On April 2, “liberation day,” the Trump Administration announced a baseline 10% tariff on most imported goods and additional “reciprocal” tariffs, quickly delayed until August, on select countries. This was on top pf other new tariffs on vehicles, parts, steel, aluminum, and other select commodities. I estimate that by June these initiatives increased the import-weighted average of tariff rates on goods - call it the “statutory” tariff rate - by 17.5 percentage points, to 20%. At May’s volume of imports, that implies an increase in the “run rate” of customs duties of nearly $600 billion at an annual rate, a staggering rise. If passed fully forward, it would lift the aggregate price level by roughly 1.7%. Yet so far, despite economists’ warnings, any impact on inflation has been difficult to discern. Why?

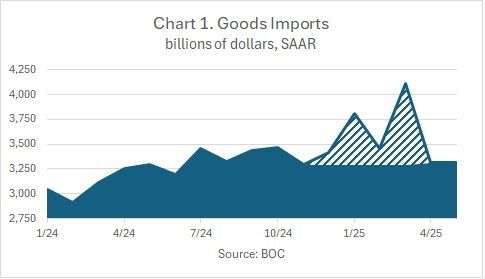

One reason is that imports temporarily surged early this year as importers rushed to beat the anticipated increase in tariffs (Chart 1). Until the resulting excess stocks are worked down, merchants can postpone selling goods subject to the new tariffs, delaying price pressures arising from the recent increases. But is there even more to it than that?

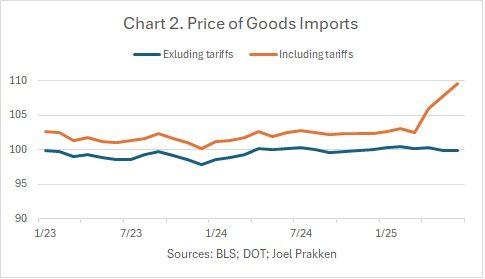

So far, we can rule out the tariffs being absorbed by foreign suppliers. Chart 2 shows the price of imported goods through June, both before tariffs (as reported by the Bureau of Labor Statistics) and including customs duties collected so far by the US government. Since March the price of imports, including tariffs, has jumped sharply with no discernible offsetting decline in the price before tariffs. So, there’s little indication here that foreign suppliers have trimmed margins to protect market share. Note, however, that since March the increase in price including tariffs is “only” 7%, far short of the 17.5% percentage point rise in the statutory tariff rate. Why not more (yet)?

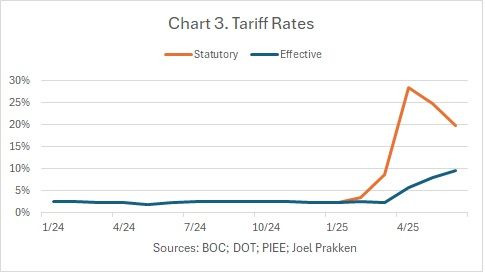

Chart 3 compares the statutory tariff rate to the “effective” rate computed as custom duties actually paid divided by goods imports. Payments have lagged far behind statutory liabilities for at least three reasons. First, payments are not due until 15 days after the liability is assessed. As tariff liabilities increase, this delay can push some payments into the following month, slowing the rise in payments until customs duties reach a steady run rate. Second, given the uncertain legality of the tariffs, importers, perhaps hopeful the tariffs will be rescinded, may be delaying payments with reduced fear of enforcement penalties.

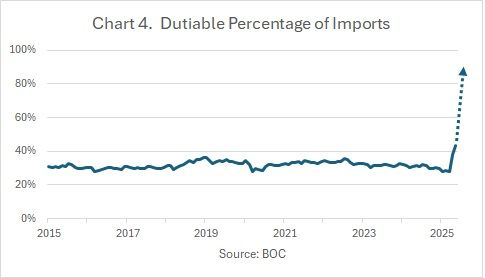

Third, and probably most important, imports are not “dutiable” (i.e., subject to tariffs) until released from customs. That release can be delayed for up to five years by storing merchandise in bonded warehouses. As evidence of this phenomenon, Chart 4 depicts the share of imports recorded as dutiable. Before the new tariffs this share hovered near 30%. However, with the notable carve out of USMCA-compliant imports, the new tariffs apply to nearly all imported goods, not just those that previously were dutiable. I estimate that roughly 85% of goods imports are now potentially subject to tariffs, yet the actual share has risen only to 44%. The difference may be hiding temporarily in bonded warehouses.

It’s likely that importers and other wholesalers are, for now, absorbing some of the increase in tariffs. But unless policy changes, there seems little doubt where this is headed. The effective tariff rate will double towards the statutory 20% rate as the share of dutiable imports rises towards 85%, implying that considerably more inflation pressure will metastasize in domestic supply chains. Furthermore, the area between the two curves in Chart 3 represents an as-of-yet unmaterialized cost that eventually will start moving forward towards final demanders. And none of this reflects the steep reciprocal tariffs that (might) go into effect in just a few weeks.

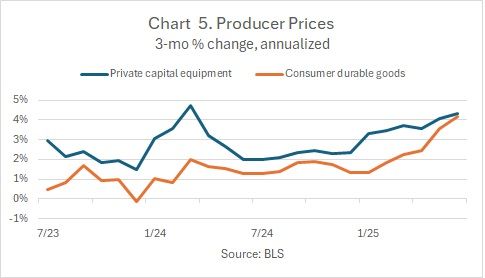

Despite the lags, evidence that the new tariffs are pushing through to price inflation is gradually emerging. For example, Chart 5 shows the 3-month change (at annualized rates) of producer prices for private capital goods and consumer durable goods, two categories of commodities with high concentrations of imports. In the 3 months since liberation day, both have moved up to exceed 4%. But with so much of the eventual costs still unrealized, it is too early to assume there’s little more tariff-related inflation risk to come – or to base monetary policy on that assumption - because in my epilogue to Becket’s play, Godot arrives pretty soon.

A longer version of this commentary is available here.

Joel Prakken

AuthorMore in Author Profile »Joel Prakken is former Chief US Economist of S&P Global and IHS Markit, co-founder of Macroeconomic Advisers, and past president and director of the National Association for Business Economics. He has served as an outside advisor to the Congressional Budget Office, on the Advisory Panel of the Bureau of Economic Analysis, and as a consultant to the Joint Committee on Taxation. He holds a BA in economics from Princeton University and a PhD in economics from Washington University in Saint Louis.