U.S. Housing Affordability Continues to Fall in December

by:Tom Moeller

|in:Economy in Brief

Summary

- Rising home prices couple with higher mortgage rates to dampen affordability.

- Family income increase fails to keep pace with rising home costs.

- Payment as a percent of income reaches six-month high.

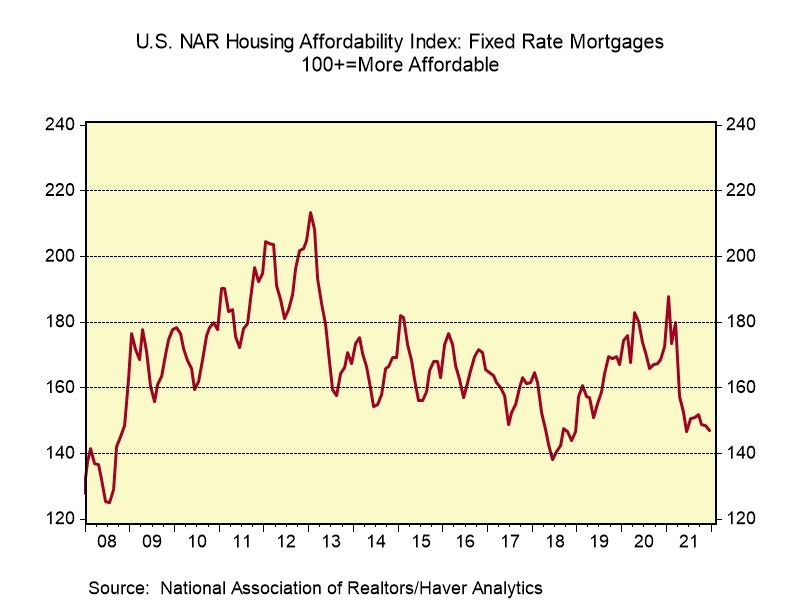

Potential home buyers are increasingly challenged when it comes to finding affordable properties. The National Association of Realtors' Fixed Rate Mortgage Housing Affordability Index fell 0.9% in December (-14.7% y/y) to 147.1 from 148.4 in November, revised from 147.8. The October figure was unrevised at 148.8. Affordability has fallen 21.7% since its recent high of 187.8 in January 2021. The Housing Affordability Index equals 100 when median family income equals the amount required for an 80% mortgage on a median priced existing single-family home.

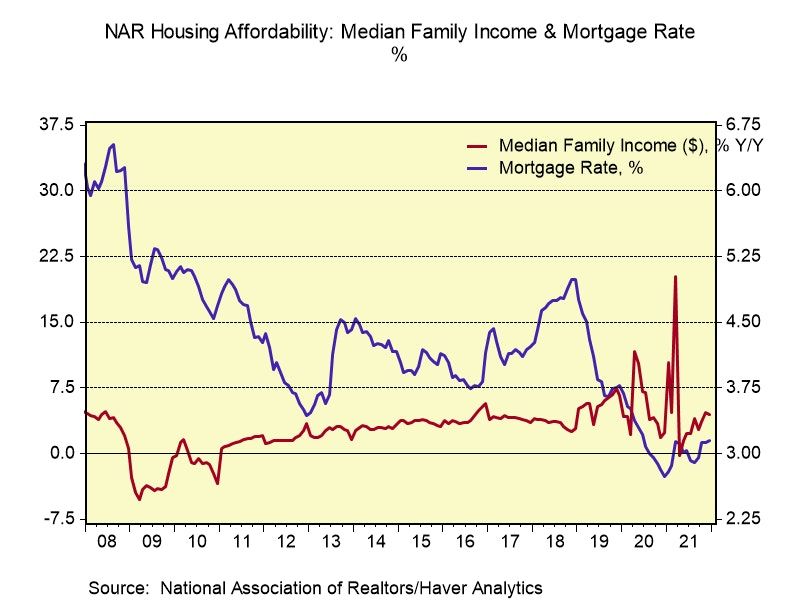

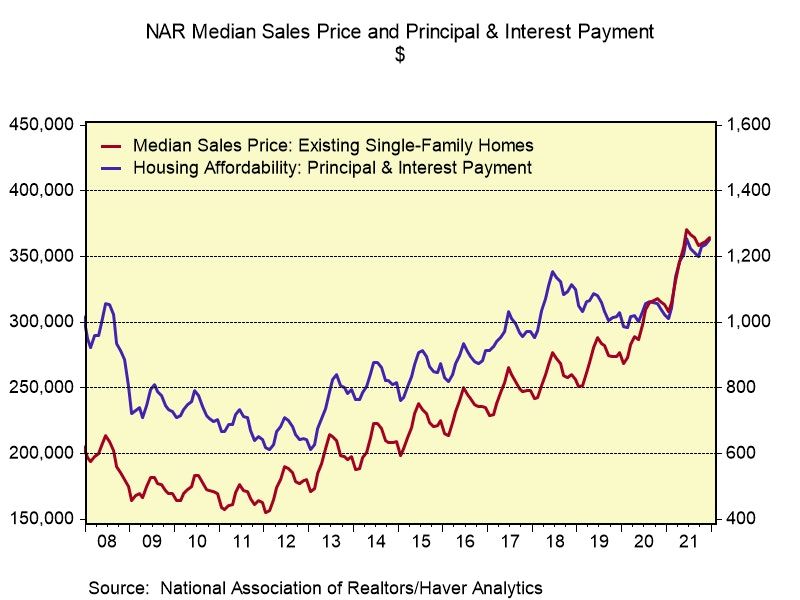

In December, the median sales price of a home rose 0.8% (16.1% y/y) to $364,300, following a 0.5% November increase to $361,300. Mortgage rates rose to 3.15% in December 2021, up from a low of 2.73% twelve months earlier. As a result, the monthly mortgage payment rose 1.2% to $1,252 (22.5% y/y) from $1,237, roughly equaling the June 2021 record of $1,253.

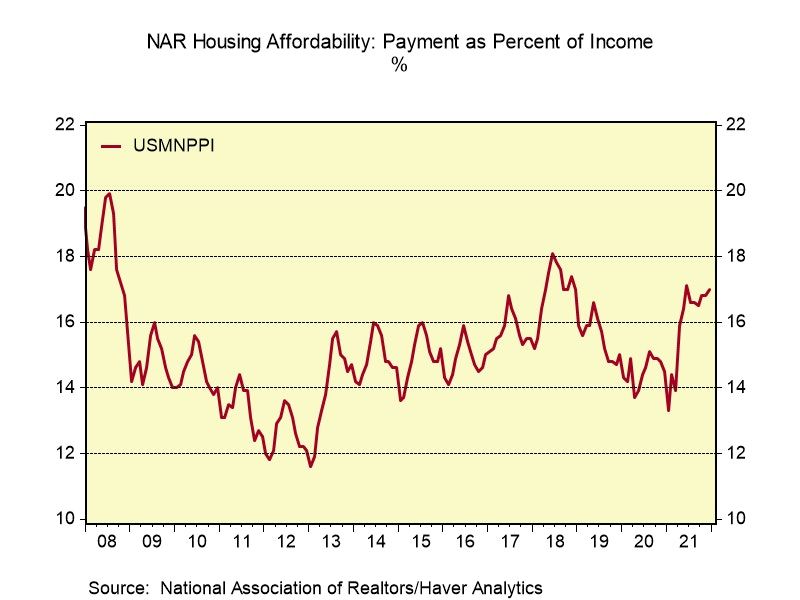

Median family income in December rose 0.3% (4.5% y/y) to $88,417 from $88,137 in November. As a result, the standard mortgage payment as a percent of income rose to 17.0%, the highest in six months. These figures are increased from a low of 13.3% last January.

Data on Housing Affordability can be found in Haver's REALTOR database. Median home sale prices are also located in USECON. Higher frequency interest rate data can be found in SURVEYW, WEEKLY, and DAILY.

Searching for Maximum Employment from the Federal Reserve Bank of San Francisco can be found here.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief

Global

Global