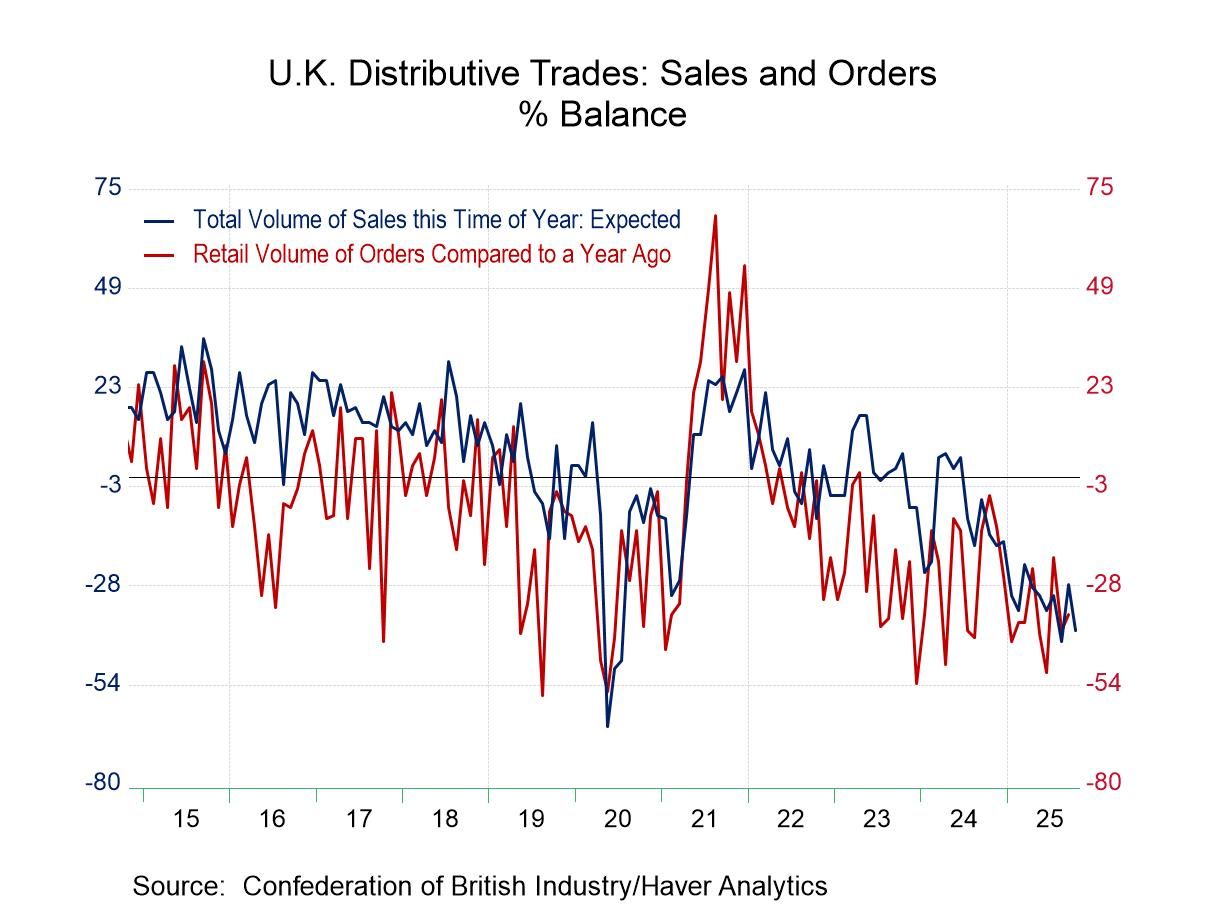

U.K. Distributive Trades: Mixed with a Worsened Outlook

The Confederation of British Industry report shows some improvement and deterioration in the same month; retailing improves while wholesale survey worsens sharply. The look-ahead to October for retailing weakens sharply while there was mixed performance in the outlook for wholesaling. The report doesn't do much to clarify the outlook.

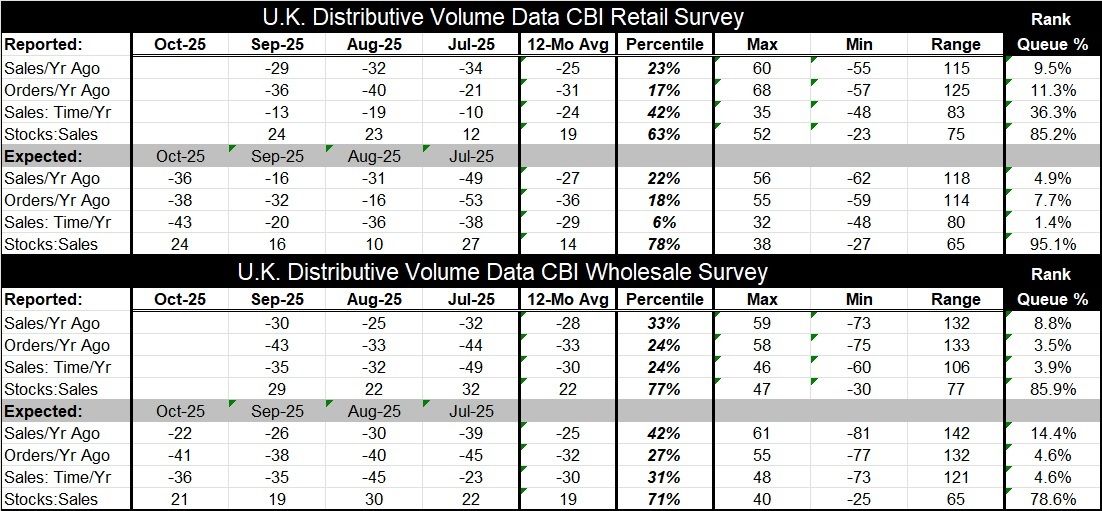

Current Sales: Current sales compared to a year ago improved to -29 in September from -32 in August. Orders compared to a year ago also improved to -36 from -40. These improvements still leave the monthly reading levels worse than their respective 12-month averages although sales at the time of year are significantly better than their 12-month average. The queue percentile standings for these metrics of sales are all weak, the only element in the report that is strong, or firm is for the stock to sales comparison, and that is usually a negative indicator.

Sales Expectations: The expectations in October for sales dropped sharply to a -36 reading from -16 in September, orders dropped to -38 from -32 in September while sales ‘for the time of year’ plunged to -43 from -20. Each one of these readings is weaker than its 12-month average. Historic standings are even weaker than for the current sales and orders metrics, with sales for a year ago with a 4.9 percentile standing and sales ‘for the time of year’ at an even weaker 1.4 percentile standing, rarely ever weaker. The current vs. the outlook signals are crossed.

Current Wholesaling: Worse performance in the current readings while the outlook for the next month is mixed marks the overview of the wholesale trade arm of the distributive sales report. Sales adjusted for the time of year and orders and sales compared to a year ago all deteriorate. Each one of these readings is not only weak month-to-month but each is weaker than its respective 12-month average. And the queue rankings are all in the lower tenth percentile range.

Wholesaling Expectations: The outlook shows mixed performance for sales compared to a year ago, improving to -22 in October from -26 in September; orders deteriorated to -41 from -38 in September. Sales ‘for the time of year’ barely ticked weaker in October. Readings are weaker than their respective 12-month averages as well, except for year-ago sales. The percentile standings for the three categories range from a ‘high’ percentile standing at its 14th percentile for sales compared to a year ago, while the other two metrics show rankings that are below their 5th percentiles in their historic queue of values – an extremely weak showing.

Summing up: Clearly the survey shows a mixed view of retail and a general worsening as well as a mixed-up picture between current performance vs. what is expected for next month. While there is little consistency in this survey in terms of monthly changes, what is crystal clear is that conditions - no matter where, or when, assessed - are very weak. Perhaps it is reports like this one that are keeping the Bank of England on hold instead of battling inflation with growth looking like it might give way at any moment.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global