Global| Oct 01 2025

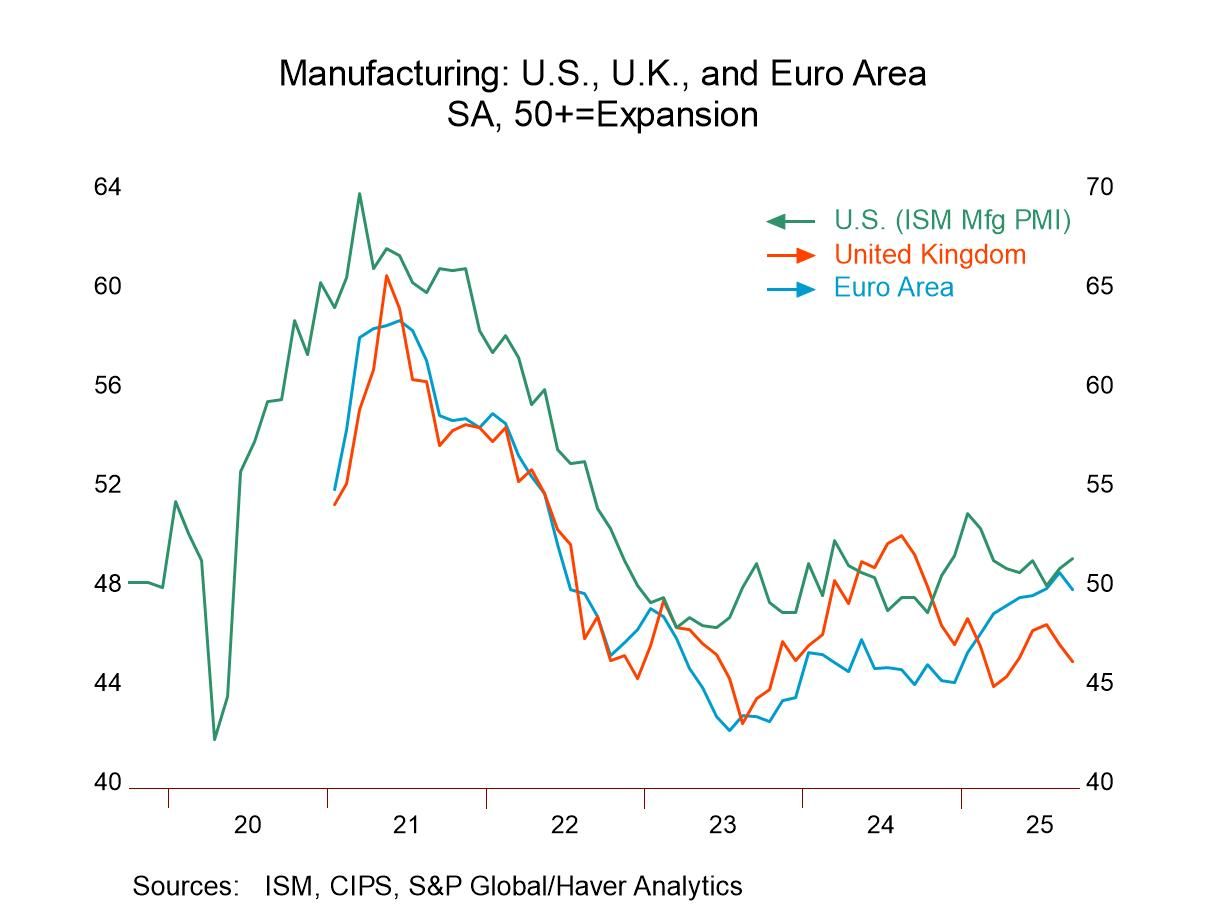

Global| Oct 01 2025Global MFG PMIs Mostly Erode in September but by Small Amounts; It’s Really a Nothing-Burger of Economic Change

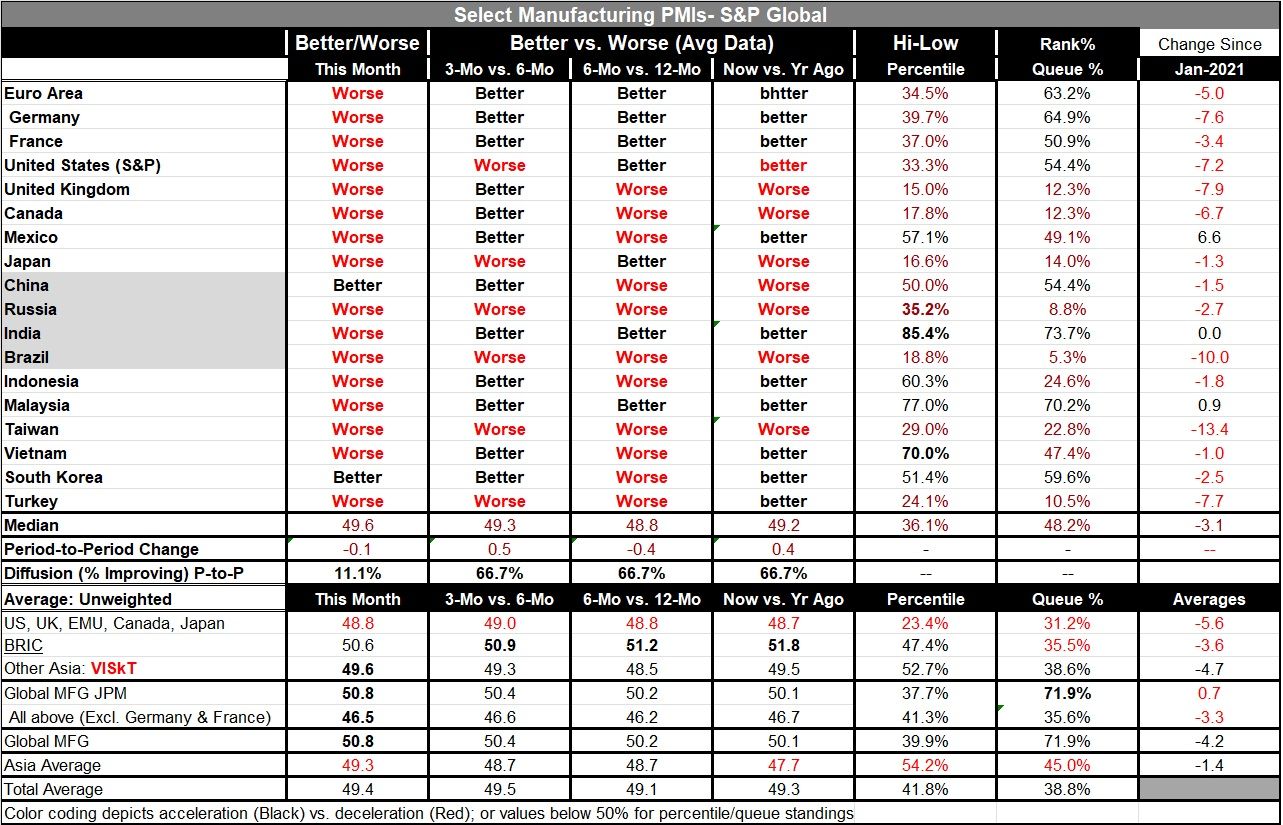

Manufacturing PMIs in September worsened for all the countries in the sample except for China and South Korea. The diffusion calculation was 11% in September but that compares to 83% in August and 55% in July; in past months improvement was much more common. Comparing the sequential results of 12-months to 6-months to 3-months, the median over 12 months is 49.2, over 6 months it's 48.8, and over 3 months it's 49.3. These are not compelling numbers in any direction and they show that output in manufacturing is simply hovering in a very slightly contractive position to 12-months ago.

The diffusion calculations that compare 3-months to 6-months, 6-months to 12-months across countries are steady at 66.7%. All those horizons regularly show improvement for two-thirds of the reporting countries over each of those horizons.

The queue rankings, however, indicate there's still a great deal of weakness with ten of the reporting countries having PMI readings since January 2021 that are below their respective medians. Output is above the respective medians for eight countries.

The bottom of the table presents statistics grouped in different ways a grouping of developed countries, the BRICs, other Asia. On that basis, there's really not much discrimination except that the BRIC countries show average readings that for the most part are above 50; other comparisons for the most part are below 50. The statistics, though, clustered around 50. The global medians call PMI values below 50 while the global averages coalesce at readings slightly above 50. And while these are differences, there's not much distinction between these differences.

In addition, we know that the queue rankings show a great deal of weakness in the current percentile standings which also leaves us with the conclusion that manufacturing is not particularly robust.

There are five countries or areas showing sequential improvement from 12-month to six-month to three-month averages and there are five of them showing sequential weakening on the same time horizon. In both cases, the transitions are small.

On balance, the conclusion for this month's manufacturing report is that there's really very little change globally. Broadly there's a slight tendency for weakness; however, the medians produce a result slightly below 50 showing contraction while the averages show values slightly above 50, indicating slight advancement in manufacturing globally.

Generally conditions remain touch-and-go clustered around a reading of 50 that implies no change. The good news is that inflation has remained moderate although it's over target in most countries. Central banks for the time being seem to be playing a wait and see game content to let inflation ride slightly above their targeted values although we have no idea how long this will last and certainly if inflation begins to move up from here central banks will have to respond to that. Conditions of global instability remain in the form of ongoing war in Ukraine; there is, however, a peace proposal up for grabs in the Middle East and it will bear watching to see how that works out.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief