Global| Sep 25 2025

Global| Sep 25 2025Charts of the Week: Resilient Activity, Noisy Policy

by:Andrew Cates

|in:Economy in Brief

Summary

Global financial markets have remained steady over the past few days: equity volatility remains low, credit spreads remain contained and core yields have drifted rather than lurched, even as policy noise—especially around US trade—remains high. Against that backdrop, this week’s flash PMIs describe a resilient but uneven expansion: Germany has inched back into growth, while France has slipped further into contraction, a divergence echoed in bonds where the OAT–Bund spread has widened amid political and fiscal uncertainty (charts 1 and 2). Latest trade data from South Korea reinforce the idea of a tech-led floor under global activity, with semiconductor exports still advancing even as broader shipments remain choppy (chart 3). Labour demand indicators tell a similar story of moderation without fracture: high frequency data for job-postings have flattened in the US and UK and have turned up in Germany (chart 4). Stepping back, the latest US flow-of-funds report show a financing mix still anchored by heavy public borrowing absorbed by foreign investors but offset by a sizeable private-sector surplus—one reason perhaps for why the world economy has remained resilient despite persistent policy uncertainty (charts 5 and 6).

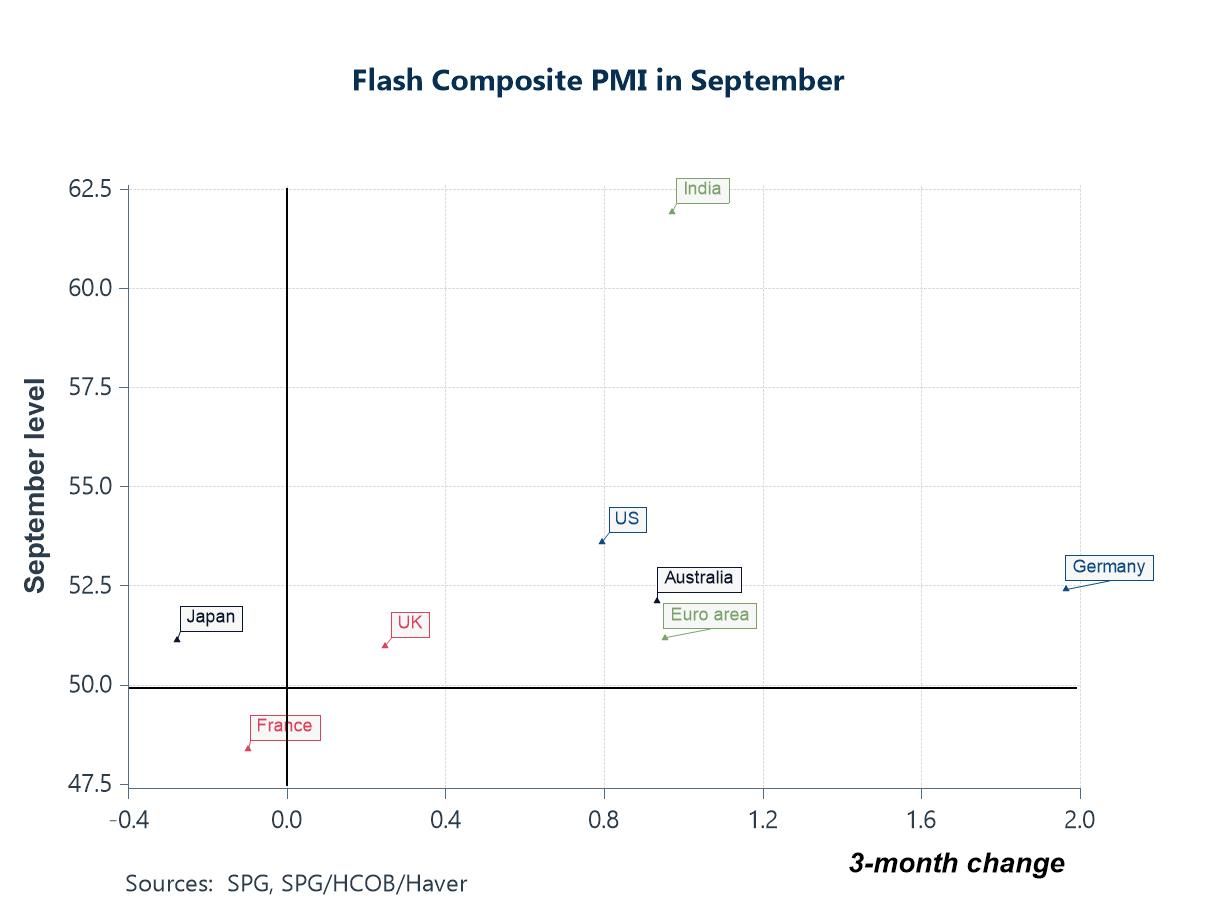

Global growth momentum – resilient but uneven This week’s flash PMIs offered a mixed but broadly resilient read on global activity. France is the clear laggard: it’s latest composite PMI remains below the 50 threshold and is one of the few economies with negative three-month momentum, pointing to a more entrenched contraction. Germany, by contrast, has edged back into expansion and registers the strongest three-month improvement, suggesting its downturn could be easing. Elsewhere, most major economies are holding up: the US, Australia and the euro area (in aggregate) sit modestly above 50 with positive impulse; the UK is hovering just over the line; Japan is softer but near neutrality; and India remains the outlier, expanding at a notably strong pace.

Chart 1: Flash PMIs — latest level and 3-month change by economy

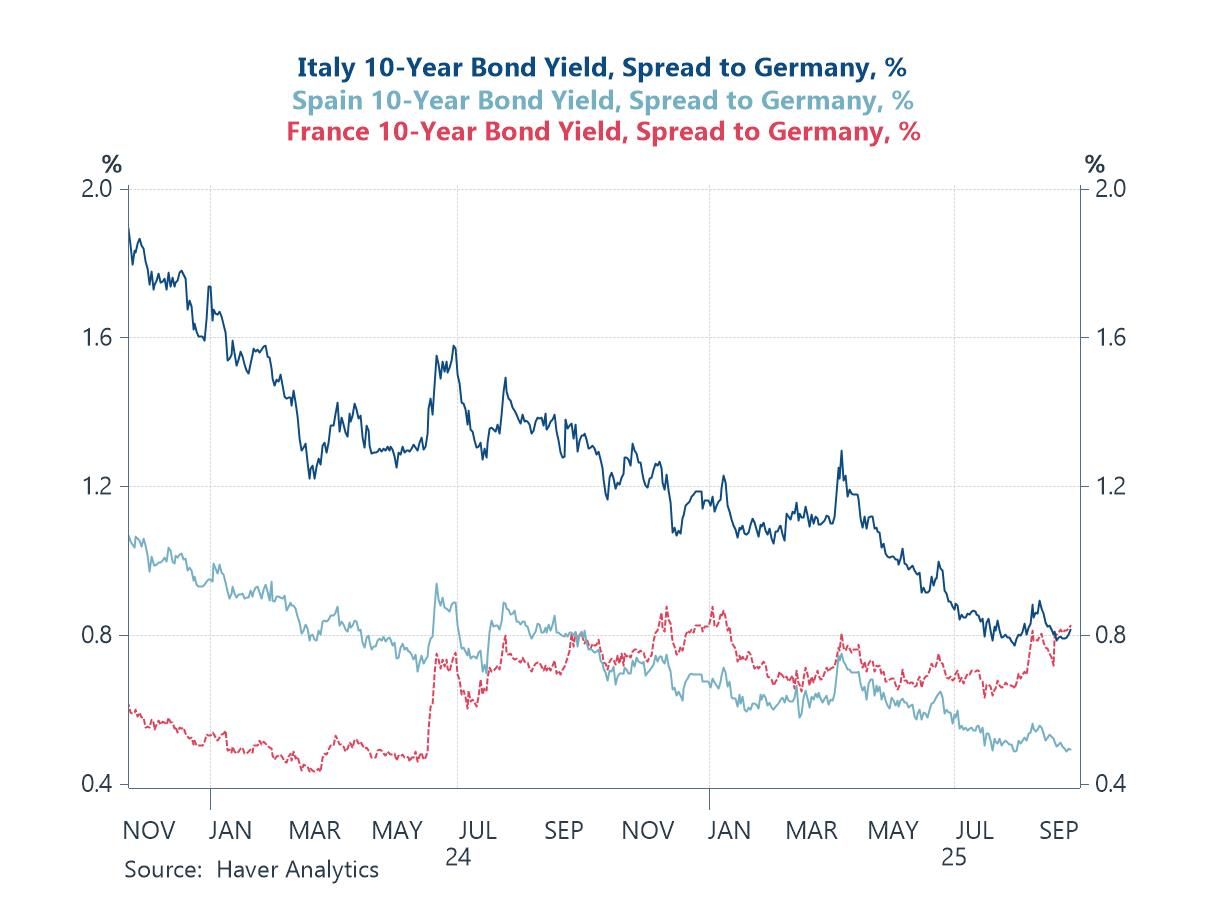

Europe’s periphery repriced: France moves toward Italy French sovereign risk has moved back into focus. The 10-year OAT–Bund spread has widened, over the past few weeks moving further away from Spain and edging toward Italy, as the chart below indicates. Investors are demanding a higher risk premium for France amid political turbulence and fiscal paralysis: a fractious legislature complicating budget passage, stalled consolidation plans, and growing doubts over the debt and deficit path. Spain’s spread has compressed on steadier politics and firmer growth and fiscal optics, while Italy’s, still the highest, has narrowed from last year’s peaks as issuance has been well absorbed and near-term policy risk has eased.

Chart 2: 10-year France–Bund spread versus Spain and Italy

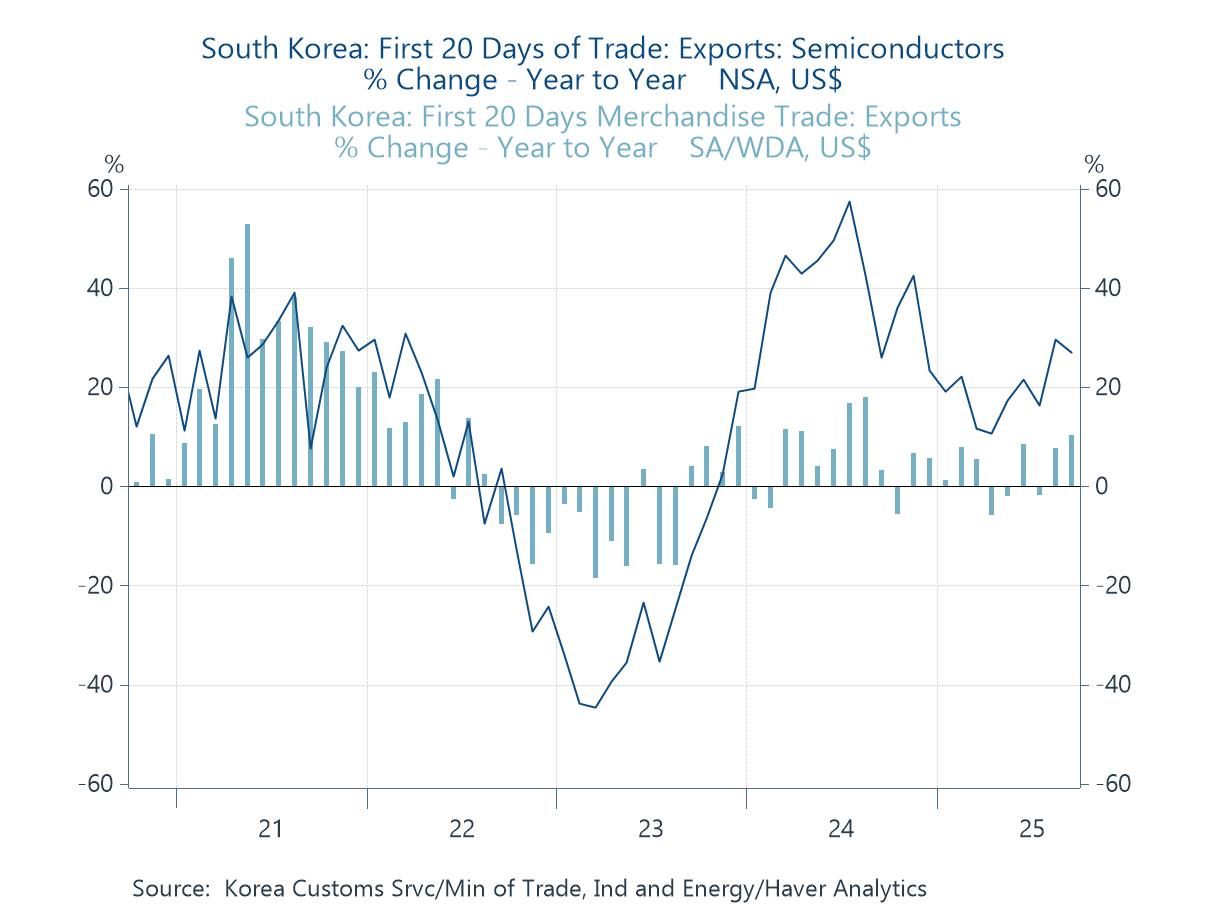

The Tech cycle – a safety net for global trade? South Korea’s latest trade data for the first 20 days of September point to a still-firm global backdrop. Semiconductor exports in the first 20 days remain up by double digits year-on-year as probably off the heels of strengthening AI-server demand. Broader goods exports have also been positive but still choppy, consistent with a tech-led upswing rather than a full-blown boom. Risks remain—tariffs, China demand, and electronics inventory swings—but for now the chip cycle is doing some of the heavy lifting for global trade.

Chart 3: South Korea early-month exports — semiconductors and total goods (y/y)

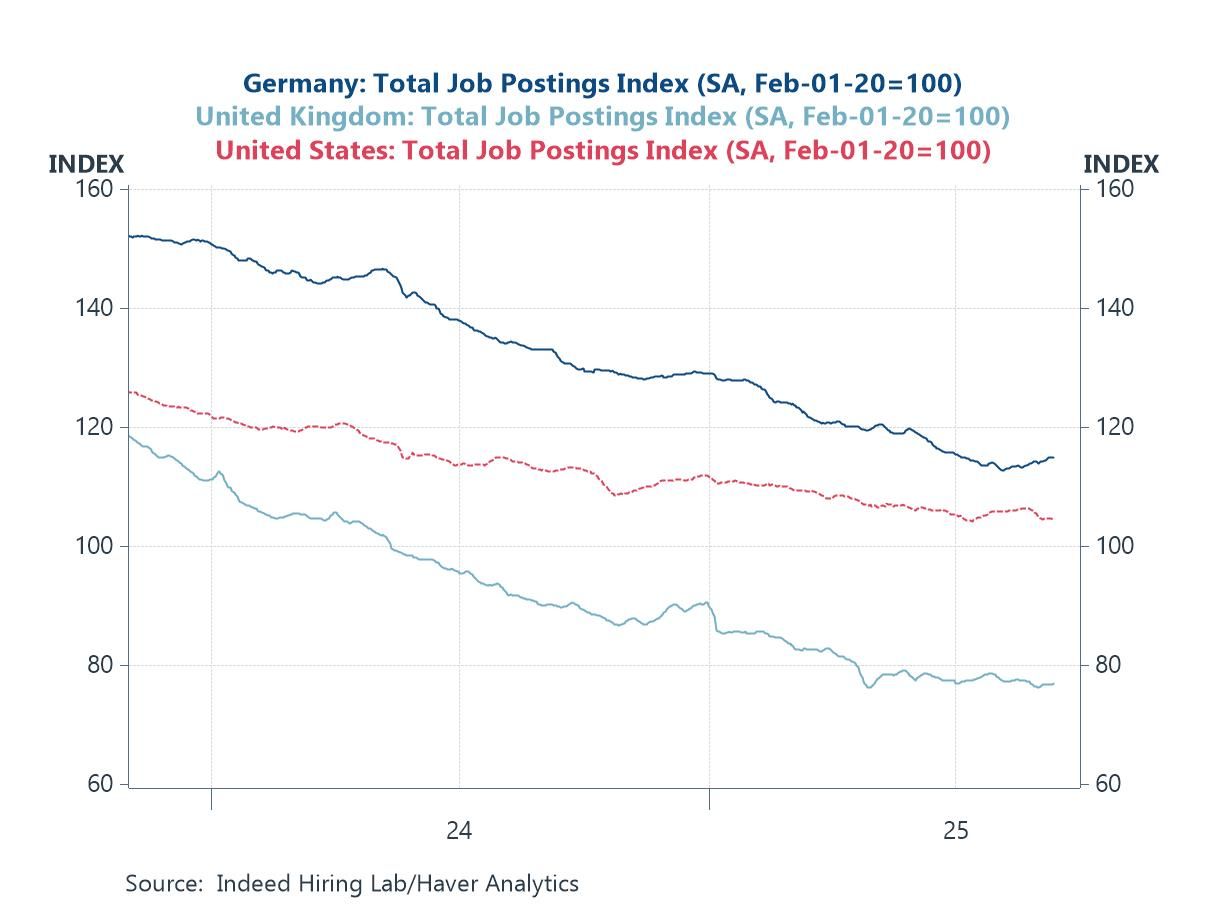

Labour demand cooling, not cracking Job postings have been trending lower across major economies for much of the past year, but that descent has recently slowed. In the US and UK the latest indices from the Indeed hiring company have flattened, suggesting demand for labour is cooling rather than collapsing. Germany has moved a step further: postings have ticked higher in recent weeks, echoing the improvement in the German flash PMI noted above and hinting more generally that a recovery phase may have begun. Taken together with broadly steady PMIs elsewhere, the picture is of a world economy that remains resilient even as hiring appetite normalises.

Chart 4: Indeed job-posting indices — US, UK and Germany

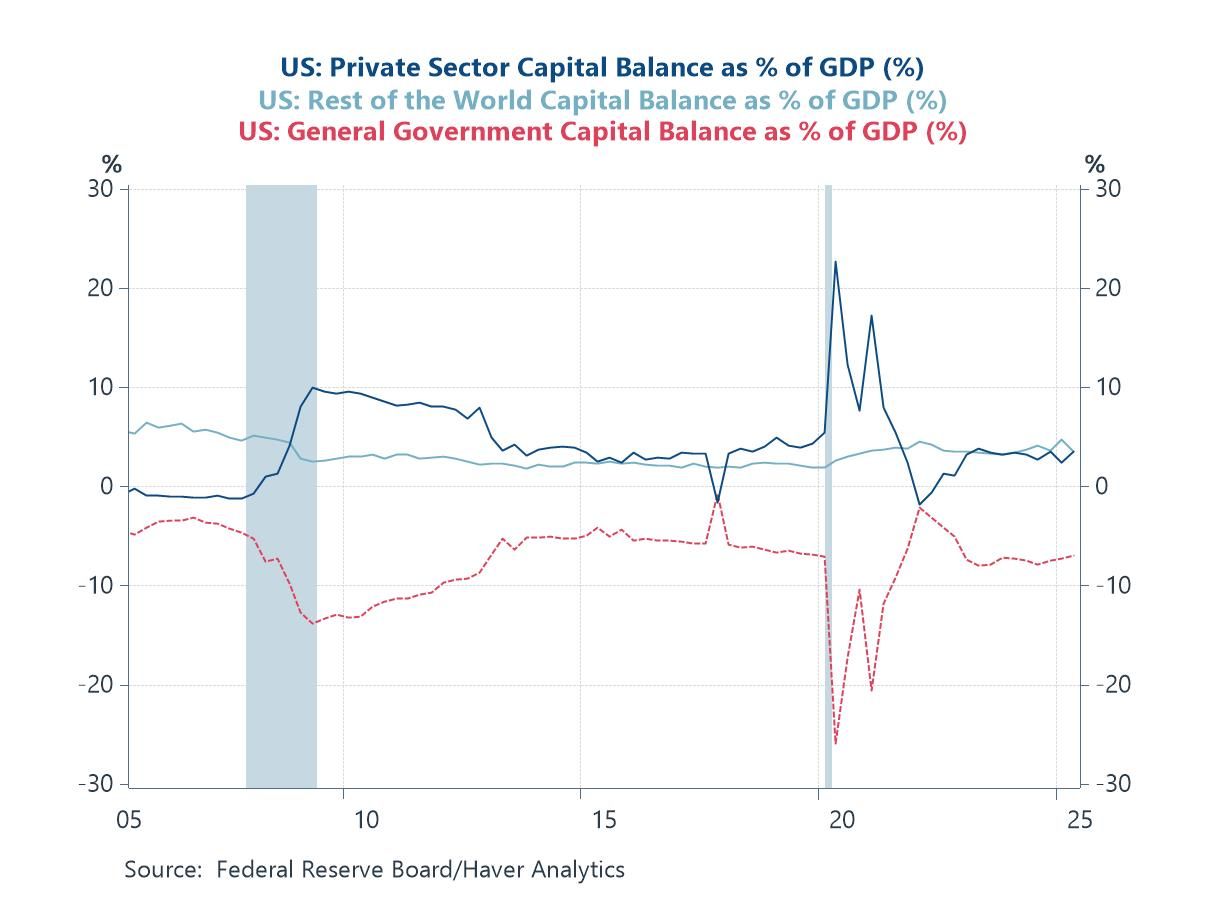

US financial balances – no change The Q2 US Financial Accounts reinforce a familiar picture of who has been doing the financing. The public sector remains the swing borrower, with general government running a large capital deficit that is still being absorbed by the rest of the world, whose net lending to the US shows little sign—so far—of retreat. There is, as yet, no clear shift away from this mix of heavy fiscal borrowing and overseas funding. Offsetting this, the private sector continues to post a sizable surplus: households and firms are, in aggregate, net lenders rather than stretched borrowers. That balance-sheet position helps explain the economy’s resilience despite relatively high interest rates and large Treasury issuance—many US (and global) recessions are preceded by excess private leverage and a painful deleveraging phase, which is not what the flow-of-funds accounts currently depict.

Chart 5: US sector financial balances — general government, private sector, rest of world

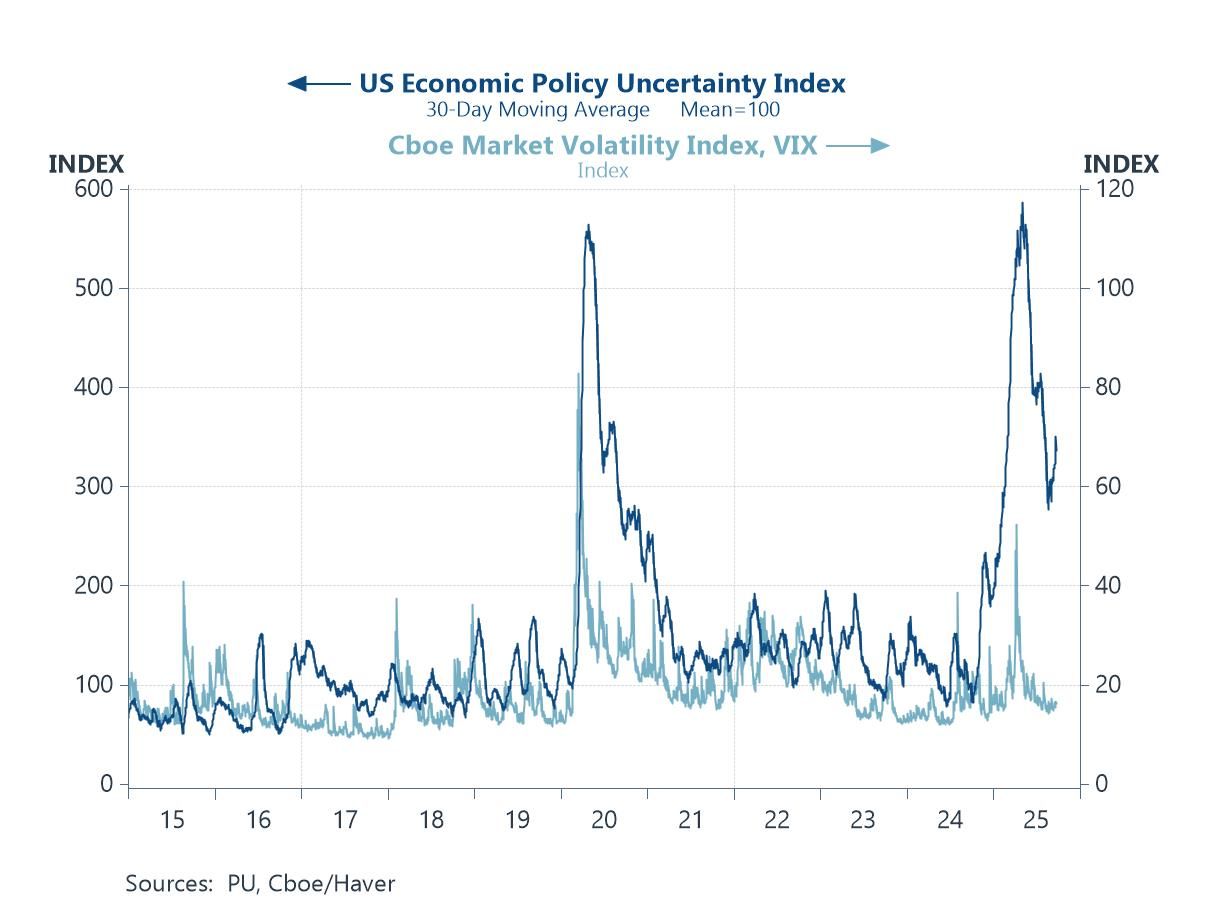

Calm markets, noisy policy — the volatility–uncertainty gap Financial markets look calm but the policy backdrop does not. The US VIX has drifted back toward low double-digits, yet the US Economic Policy Uncertainty index remains well above its long-run average. The gap reflects unresolved policy questions—most notably around trade—where shifting tariff threats, supply-chain rules and enforcement actions keep firms guessing about costs, market access and investment timing despite subdued day-to-day market volatility.

Chart 6: VIX versus US Economic Policy Uncertainty index

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.

More Economy in Brief