Global| Aug 16 2016

Global| Aug 16 2016ZEW Reading Improves But Disappoints

Summary

The ZEW index of expectations is compiled from the survey results of German financial experts. Expectations recovered in August to post a 0.5 net reading, a positive assessment for expectations, up from -6.8 in July. July had been a [...]

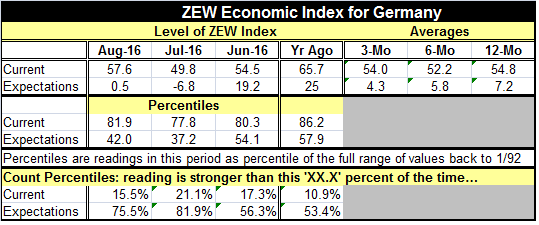

The ZEW index of expectations is compiled from the survey results of German financial experts. Expectations recovered in August to post a 0.5 net reading, a positive assessment for expectations, up from -6.8 in July. July had been a sharply lower reading, falling from 19.2 in June. So there is very little rebound after the July setback. While the Bundesbank has expressed a minimized notion of the impact of Brexit on data, growth and policy, the fact is that a lot remains to be settled and until it is done here is likely to be knock-on effects. The ZEW experts seem to understand this and they do not seem to be drinking the Bundesbank Kool Aide with their usual gusto. The Bundesbank seems mostly trying to head off Brexit as a reason for the ECB to step up stimulus. It is far from clear that it is a wise choice of action, but it is not a surprising tact from the Bundesbank.

The ZEW index of expectations is compiled from the survey results of German financial experts. Expectations recovered in August to post a 0.5 net reading, a positive assessment for expectations, up from -6.8 in July. July had been a sharply lower reading, falling from 19.2 in June. So there is very little rebound after the July setback. While the Bundesbank has expressed a minimized notion of the impact of Brexit on data, growth and policy, the fact is that a lot remains to be settled and until it is done here is likely to be knock-on effects. The ZEW experts seem to understand this and they do not seem to be drinking the Bundesbank Kool Aide with their usual gusto. The Bundesbank seems mostly trying to head off Brexit as a reason for the ECB to step up stimulus. It is far from clear that it is a wise choice of action, but it is not a surprising tact from the Bundesbank.

The current index, after a dip in July, has sprung back to an even stronger reading in August. In this measure, the Bundesbank's view of the resilience of the German economy is borne out. The current index sank from 54.5 in June to 48.9 in July but rebounded to stand at 57.6 in August.

The current index was last stronger than this back in January 2016. And the expectations index was last weaker last month. But apart from that, we go back to October 2014 to find a weaker expectations reading.

The current index is stronger than its August value only 15.5% of the time historically. The expectations index is stronger 75.5% of the time. But the current and future indexes standings are telling quite different tales about what is happening vs. what is likely to happen. This should create some policy dilemma, but it has not for the Bundesbank that wants to draw a line under all of this stimulus and just put a stop to it.

The ZEW financial experts downgraded both stocks and bonds this month, for the second month in a row. The bond assessment is outright negative while the stock assessment is modest but positive. This seems to echo the thought process we see in other national markets as well. But ZEW experts have been negative on bonds for too long. Their run of negative assessments extends all the way back to January 2009. They have left some fine bond market gains on the table.

The ZEW experts' stock market rating was negative once since 1994 that was in the month of May 2010. However, the chart run at the top of this report shows a definite connection to the performance of the DAX and the value of the ZEW expectations reading. Expectations hit a peak in 2014 and a lower peak in 2015. After the second peak, expectations have stayed much lower and the German stock market has also been in a period of consolidation. In Germany, neither the Bundesbank nor the markets seem to be too sure where things are going next. But the bloom is off the rose.in the beer garden.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief