Global| Aug 13 2019

Global| Aug 13 2019ZEW Momentum Shows Uniform Weakness

Summary

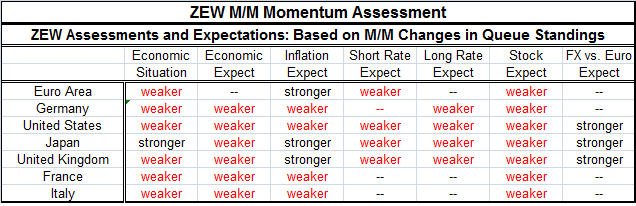

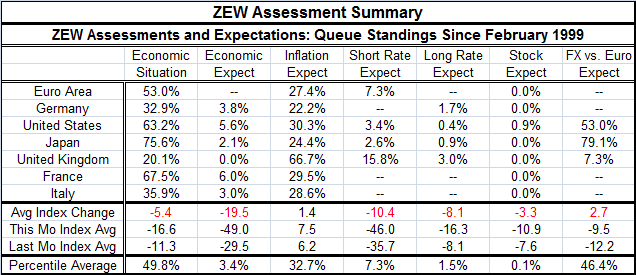

ZEW experts' macroeconomic expectations are being cut sharply again. This time the cut is from a much lower point (see Chart). The entire survey is a study in weakness as the table below shows. Its labeling is based upon month-to- [...]

ZEW experts' macroeconomic expectations are being cut sharply again. This time the cut is from a much lower point (see Chart). The entire survey is a study in weakness as the table below shows. Its labeling is based upon month-to-month changes in the individual surveyed components. Of 38 components surveyed, only seven entries are stronger and nearly half of those refer to the expectations for the value of foreign currencies vs. the euro. Among components only inflation shows any sign of getting stronger in any sort of ‘broad way'. And inflation expectations still strike an average standing near the lower one-third of their historic queue of values. Inflation is not running away; it may be nudging away…

ZEW experts' macroeconomic expectations are being cut sharply again. This time the cut is from a much lower point (see Chart). The entire survey is a study in weakness as the table below shows. Its labeling is based upon month-to-month changes in the individual surveyed components. Of 38 components surveyed, only seven entries are stronger and nearly half of those refer to the expectations for the value of foreign currencies vs. the euro. Among components only inflation shows any sign of getting stronger in any sort of ‘broad way'. And inflation expectations still strike an average standing near the lower one-third of their historic queue of values. Inflation is not running away; it may be nudging away…

The actual queue standings are presented in the table below. It shows the economic situation has declined (on average) by 5.4 diffusion points in August. Japan, France, the United States, and the euro area continue to report an economic situation score that is above their respective historic medians in these countries. The United Kingdom, Germany, and Italy report below median scores (scores below the 50% level).

Economic expectations, however, are uniformly pathetically weak. The highest expectation is the 6 percentile standing posted in France. That, of course, means that French expectations have been better 94% of the time. And that is the strongest expectation among the group of countries and the EMU region in the table! In addition to the weak standing, there was a sharp negative downturn reported for expectations this month.

Inflation expectations show a small mark up on average. But the ‘average' for expectations is still only 32.7% a value in the lower one third of all historic results. By country/region, the U.K., with its Brexit uncertainties in tow, boosts the overall strongest with a 66.7 percentile (top one third) reading. Everywhere else inflation expectations are in the lower one third of their respective distributions with Germany's 22.2 percentile standing, the weakest of all.

Short-term interest rate expectations (four observations) are low and fell by a sharp 10 diffusion points on average this month. They average a standing in their lower 10th percentile. Rate expectations are for conditions that have been lower than this only 10% of the time on average. The U.K. has the strong observation bringing the average up, but it still has a weak standing.

Long-term interest rate expectations also fell on the month and nearly as sharply as short-term expectations, at least in diffusion terms. Seeing sharp cuts in both long-term and short-term expectations underscores the perceived need for rates to move lower and is certainly consistent with the weak expectations that ZEW respondents offer.

Stock market expectations are at a zero standing (lowest ever) across most economic units. The U.S. is an exception but not much of one.

On balance, these are grim standings for the EMU region and other countries. The U.S.-China trade war has certainly poisoned the atmosphere, but there are a host of other negatives in the mix as well ranging from Iran in the Gulf to the Japan-South Korea rift and more. The long stretch of growth has left economies with few idle resources to mobilize. At the same time, low inflation has kept central bank policy easy which means that now they have little ammunition (if any) to expend in an effort to prop up growth with monetary policy. While the ZEW experts are very downbeat on stocks, bond yields are so low. And in Europe, so many bond yields are negative; it is hard to not like stocks. The adverse ‘stock market complex' showed by the ZEW experts in this survey is probably excessive and owes to too much academic training and an inability to come up with an acceptable model that explains these ‘odd-ball' times adequately. Stock market dividend yields exceed many bond yields. In this environment while stocks may seem vulnerable with economic weakness in tow and in prospect, if investors sell stocks where will they go? If they buy bonds, how much lower can yields go...and for how long? Are bonds really a safe haven? This remains an unanswered question as the world churns.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief