Global| Sep 13 2016

Global| Sep 13 2016ZEW Index Neither Zigs Nor Zags

Summary

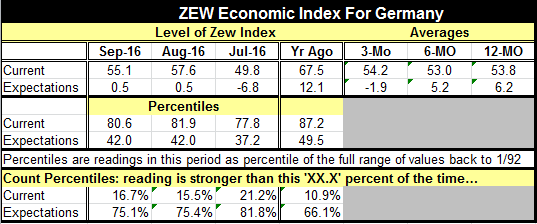

The Zew experts' expectations were dead flat at a net diffusion reading of 0.5 for the second month in row. At a level of 0.5 the expectations index is stronger 75% of the time (lower 25% of the time) and as such indicates [...]

The Zew experts' expectations were dead flat at a net diffusion reading of 0.5 for the second month in row. At a level of 0.5 the expectations index is stronger 75% of the time (lower 25% of the time) and as such indicates considerable weakening in what is expected. However, the current situation which slipped to 55.1 in September from 57.6 in July is stronger less than 17% of the time marking the economy as in pretty good shape despite decidedly weak expectations. When your economy is only better 17% percent of the time it's not too surprising that expectations see conditions as more likely to worsen ahead.

The Zew experts' expectations were dead flat at a net diffusion reading of 0.5 for the second month in row. At a level of 0.5 the expectations index is stronger 75% of the time (lower 25% of the time) and as such indicates considerable weakening in what is expected. However, the current situation which slipped to 55.1 in September from 57.6 in July is stronger less than 17% of the time marking the economy as in pretty good shape despite decidedly weak expectations. When your economy is only better 17% percent of the time it's not too surprising that expectations see conditions as more likely to worsen ahead.

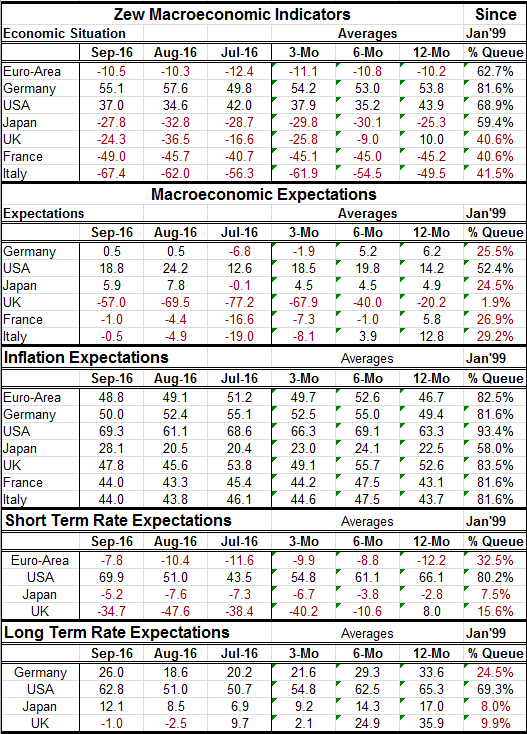

Expectations for Germany The Zew experts also form expectations for other nations on various variables. Their assessment on a pool of data back to early 1999 has Germany rated the strongest among the group in the table on their survey. Germany's economic situation is assessed at an 81 percentile standing followed by the US at its 68th percentile, while of the Euro-Area is at its 62nd percentile and Japan at its 59th percentile. The rankings for the UK, France and Italy each are below their 50th percentiles (that means below their median reading for the period) all hugging the lower 40th percentile.

Zew experts' expectations: beyond Germany

Growth expectations Expectations across this group are far lower with only the US at its 52nd percentile having a value above its median since early 1999. Most expectations hover around the 25th percentile of their respective queues of data with the U.K. in the post - Brexit environment at its bottom two percentile. The U.K. reading however is rising from its period low of July when it sank to -77.2; as of September it is back to a net reading of -57 as the experts reassess the impact and timing of the Brexit-related issues.

Inflation expectations in context Inflation expectations are at extremely high values in their 80th to 90th percentiles across all counties in the table-notably except Japan which is at a 58th percentile standing. These are assessments made since early 1999 a period in which inflation has been exceptionally low. The relatively high queue standings should be taken against that back drop.

Oil- are Zew experts behind the curve that OPEC just threw? We can also note that in separate assessments the Zew experts have oil price expectations in their 83rd percentile on this same time line - reinforcing these country-by-country measures. However, just yesterday the oil price landscape seemed to shift. OPEC produced a considerably more down beat assessment that foresaw weaker oil demand and stronger supply. Just today the IEA (International Energy Agency) reversed its own more buoyant assessment of last month to align its outlook with the much more pessimistic OPEC scenario. Reports in the U.S. have seen oil rig operations up for a number of weeks running with oil prices hovering around or above the mid-40-dollar-per-barrel mark. It appears that at this level some of the US oil supply is prepared to come back on line and unless OPEC steps back to make way for it, there will be further downward pressures on oil prices unless or until demand picks up. It is quite possible that when the Zew experts have had the time to assess the new IEA and OPEC scenarios their view on oil prices and national inflation trends will shift.

Interest rate views Short- and long- term interest rate expectations are uniformly low except in the US where the percentile rises to the 80th queue percentile for short rates and to nearly the 70th percentile for long rates. The difference in the ranking of long and short rates communicates that there are no real inflation fears as long rates are seen holding better than short rates on a relative basis. Clearly the expected Federal Reserve rate hike is what is operating here. Short rates still have outright negative diffusion values for EMU, Japan and the U.K. Long term rate expectations are not so low and have not gotten that low in this cycle as much of the rate decline appears to been unexpected. We find ourselves with very low rates and with rate expectations generally not having anticipated them in this cycle. In September only the UK has a negative expectations net reading. But Japan and the U.K. have expectations standing in the lower ten-percentile of their historic data queue. For Germany the standing is in the lower 25 percentile of its historic data queue. The US standing is in its 69th percentile. On balance, the Zew experts seem to embrace the view that has been in vogue for some time-that in Europe and Japan rates will remain low or ease in the future while rates will rise in the US. This is a definite drink of the Kool-Aide being served by central bankers. It is also a set of expectations that seems to embrace what may be an old policy at the Fed- a plan to hike rates "as soon as possible" that we can link to the views of Stanley Fischer.

Old Fed policy? While the Fed has not actually announced a plan to hike rates as soon as possible it is clear that this is an underlying Fed desire. Many Fed members whether Monetarist or Keynesian see rates as too low for too long and have fears about rising inflation, building financial excesses due to low rates or inflation flaring because of a low rate of unemployment. The Fed's low-rate policy has brought together a unique group of formerly warring factions with very different views on how the economy works.

Policy fracturing at the Fed? But US data have not permitted the Fed to engage the follow-through since it hiked rates under dodgy circumstances poorly supported by its own parameters at the end of last year. In a speech by Lael Brainard given just yesterday there is the first comprehensive attempt to reassess what policy is up to and what the risks have become by looking at the actual facts. District Bank President Jim Bullard already has gone rogue and stopped contributing a dot to the Fed funds expectations exercise. President John Williams in San Francisco called for a policy re-think but also supported the notion of a rate hike. But then the two monthly ISM indicators weakened sharply. And now many Fed officials are stuck with the words from their mouths not matching the data on the docket. This circumstance has caused some to backtrack and others to continue talk of the need to discuss the possibility of a rate hike even at the Fed's September meeting.

Fed on edge and on hold for too long Brainard's speech is the best bridge so far between understanding the actual data and how the Fed used to look at indicators; she chronicles how the Fed may have to shift its data interpretations and responses in the future. It is not clear how many Fed officials are with her on that bridge. For some it will be a bridge too far. Several Fed officials seem almost ready to jettison ISM readings in favor of incoming GDP data that suggest Q3 growth will be better - but growth has been so weak "better" is not saying much and even if it is better for one quarter it might not endure. ISMs should not be "jettisoned" lightly. All of this is mighty confusing.

What it means for everyone... The Zew experts are not the only ones who might be caught-out with an old view of the central bank's intentions or OPEC's views. There is just no telling where US policy goes next. And Brainard has made the argument that the world is more closely connected and that policy effects are more quickly and fully passed between countries. If she is right it's a very good time not to fall in love with your forecast du jour where you are.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief