Global| Apr 21 2020

Global| Apr 21 2020ZEW Experts Show Wild Swings in Expectations and More

Summary

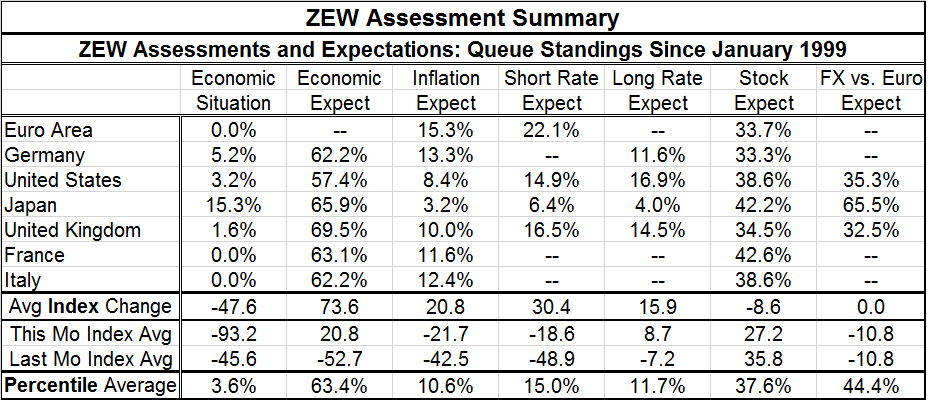

It's down, it's up, it's down, it's up...it's confused! The table below shows the percentile standings of the ZEW assessments this month on different gauges. The bottom of the table offers various summary statistics among them the [...]

It's down, it's up, it's down, it's up...it's confused!

It's down, it's up, it's down, it's up...it's confused!

The table below shows the percentile standings of the ZEW assessments this month on different gauges. The bottom of the table offers various summary statistics among them the change in the (diffusion) index on the month. These assessments have a range of +100 to -100 (everyone can think things are great or everyone can think they are rotten) with many possibilities in between. The main body of the table offers the percentile standing of the diffusion indexes in their queue of values since 1999.

This month the average index reading across table entries is -47.6 for the economic situation and +73.6 for economic expectation. Each of these is the largest swing in the history of the respective series. However, both expectations and the current situation had deteriorated sharply on a month-to-month basis one month ago. This month takes the actual current index reading nearly to its lower limit with a average reading of -93.2 (That is impressively weak for an average of seven entries with the maximum low of -100). But macroeconomic expectations that had fallen so sharply one month ago have rebounded even more sharply. That rebound has put the macroeconomic expectation reading back at a net positive reading, higher than anything we have seen on average since August 2015.

At the same time the ZEW assessment on oil is dead wrong as of mid 'mid-April' survey respondents saw oil at a 98th percentile standing of certainty looking for it to firm. Instead oil prices have collapsed to the weakest we have seen with futures prices even producing negative values for oil. Clearly the ZEW experts are grasping at straws. One month ago the virus and its spread scared the heck out of them; now all of a sudden they see a big bright light at the end of the tunnel. This is despite there being no vaccine and disparate plans for normalization that are untested as well as the fact that countries are facing a host of differing circumstances.

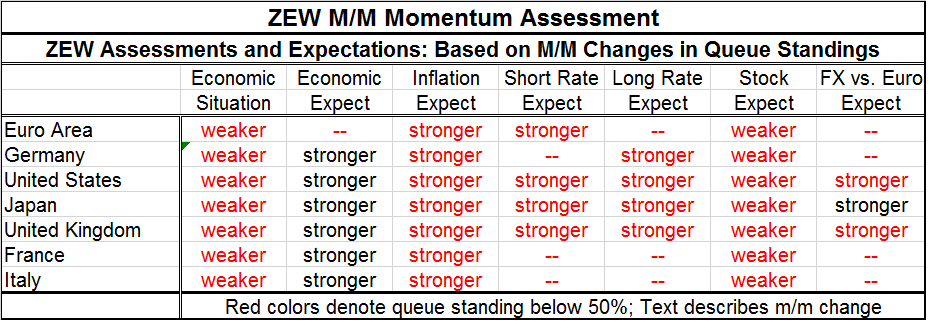

The second table below distances us (may be not quite six feet) from the particulars of the first table and shows trends very clearly. The color coding shows us that only expectations (really) have percentile standings of the diffusion indexes above their 50% mark which places them above their historic medians. This explains the jump in the stock markets. Stocks are still assessed a bit weaker month-to-month, but that assessment was cut very little month-to-month. And stock's queue standings remain well below the queue standing for expectations. Stocks are not being marked up in step with expectations for economic revival but are being marked up nonetheless and we see that in real world equity market functioning.

Not only are the so-called curves beginning to flatten rather broadly but people are getting tired of being cooped-up and the economic damage is spreading in a way that threatens to get out of control even in the face of support programs and the money that is being paid out. A change is coming; the equity market can smell it.

Expectations for 'normalization' are shifting up on a pastiche of optimism, impatience, and obstinance. WHO warns that that the transition toward normalcy must be measured.

On balance, the economic situation is still asses as poor at a horrifically weak 3.6% queue standing on average. Economic expectations at a 63.4% average are above their historic median. Inflation expectations are at their lower 10th percentile. Short-term interest rate expectations are at their lower 15th percentile with long-term rates at their 11th percentile. Stock expectations hold to their 37th percentile, still well below their median.

These, of course, are only assessments and expectations. Given that financial experts know little about the virus, we should view these metrics they offer as being unusually suspect. At the same time, these metrics go a long way to explaining why markets are acting as they are acting. There is optimism about the future despite the deep dark days of present. Will that dichotomy stand? Will the more buoyant expectations be satisfied? Stay tuned for as the world churns…

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief