Global| Jul 16 2019

Global| Jul 16 2019ZEW Experts' Assessments Dim

Summary

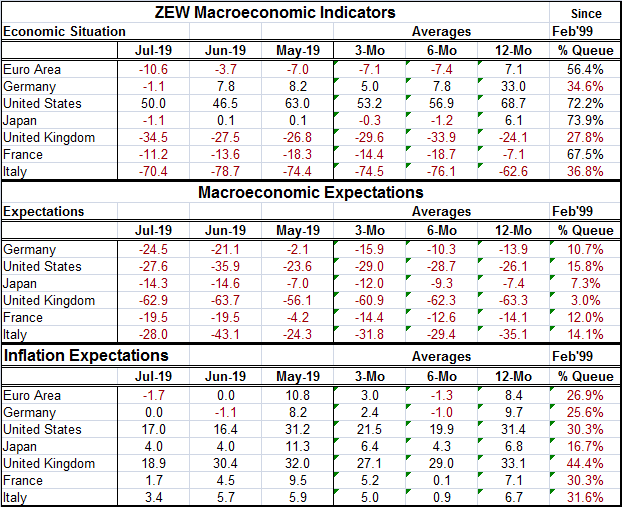

The ZEW experts' macroeconomic current assessment in July has been cut for the euro area, Germany, Japan, and the United Kingdom. The U.S. outlook stepped up in July while the weak outlook for Italy improved and the negative outlook [...]

The ZEW experts' macroeconomic current assessment in July has been cut for the euro area, Germany, Japan, and the United Kingdom. The U.S. outlook stepped up in July while the weak outlook for Italy improved and the negative outlook for France became less intense. Still, as of July, only the United States has a positive assessment of its current economic condition and that is by a wide margin. Germany, that had been clinging to a positive outlook and was neck-and-neck with the U.S. diffusion assessment just one year ago, has posted its first net negative diffusion reading of this cycle. However, Japan, the U.S., France, and the euro area all have rank standings of the current readings that lie above their historic medians (above 50) back to early-1999. Yes! That is true despite the very weak negative reading for France and the negative reading for Japan. Japan with a diffusion response this month of -1.1 and the U.S. with a reading of 50.0 find that Japan's queue standing is higher than that of the U.S.! That is a ‘statement' about how long Japan's economy has been mired in difficulty. It is reminiscent of the expression “been down so long, looks like up to me.”

The ZEW experts' macroeconomic current assessment in July has been cut for the euro area, Germany, Japan, and the United Kingdom. The U.S. outlook stepped up in July while the weak outlook for Italy improved and the negative outlook for France became less intense. Still, as of July, only the United States has a positive assessment of its current economic condition and that is by a wide margin. Germany, that had been clinging to a positive outlook and was neck-and-neck with the U.S. diffusion assessment just one year ago, has posted its first net negative diffusion reading of this cycle. However, Japan, the U.S., France, and the euro area all have rank standings of the current readings that lie above their historic medians (above 50) back to early-1999. Yes! That is true despite the very weak negative reading for France and the negative reading for Japan. Japan with a diffusion response this month of -1.1 and the U.S. with a reading of 50.0 find that Japan's queue standing is higher than that of the U.S.! That is a ‘statement' about how long Japan's economy has been mired in difficulty. It is reminiscent of the expression “been down so long, looks like up to me.”

Economic expectations

Turning to economic expectations-where all observations are negative- the U.K. has the weakest diffusion reading as its Brexit woes drag on and on. Italy, the U.S. and Germany, in that order, have the next weakest readings, followed by France and Japan, whose -14.3 reading is the highest. However, much of this is hairsplitting. The queue rankings for countries are in their lower 16th percentile or weaker across the board. The U.K. reading has been weaker only 3% of the time. On a queue basis, the U.S. reading is the relative strongest being lower historically only 15.8% of the time. Still, it's not impressive.

Inflation expectations

Inflation diffusion readings are weak across the board. Since deflation is a rare occurrence, most of the inflation assessments are low but positive with global inflation already running quite low. The euro area is an exception this month with a net -1.7 percentile reading, reflecting the expectation of inflation falling and raising the specter of deflation as a possibility. German inflation expectation readings ‘improved' month-to-month from a negative reading to zero. Japan remains at a low 4.0 diffusion reading with Italy at 3.4 and France at 1.7. The U.K. reading moved the most in July, declining from a 30.4 June reading to an 18.9 reading apparently indicting some potential for disinflationary results if there is a hard Brexit. That is somewhat confusing since a hard Brexit would seem more likely to crash the sterling that is already weak and setting new 2-year-plus low vs. the dollar. Perhaps this reading reflects the expectations that sterling has gotten most of its decline out of the way. The queue ranking for these inflation metrics are in the mid-20th to low-30th percentiles for most countries. Japan is an exception with a 16.7 percentile standing; the U.K. has the high side reading at its 44.4 percentile (despite the monthly decline in the diffusion index), that is still below its historic median.

Market outlook

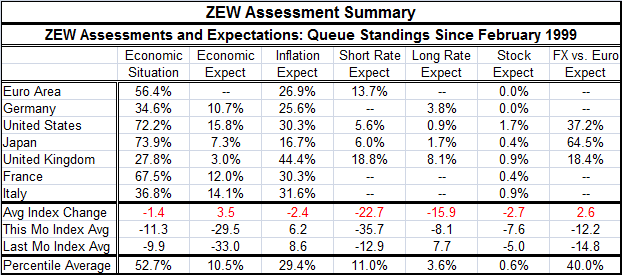

Turning to the summary table below, we see that short-term and long-terms rate expectations have very low queue standings. Short-term rate expectations fell everywhere in July. In the EMU, they plunged from a -5.4 reading to -44.3 in July. In the U.S. they also plunged from -43.6 to -72 in July with a strong knock down from -3.3 to -20.4 in July in the U.K. as well. All members have short-term rate expectations in the lower 20th percentile on a queue standing basis or lower. Long-term rate expectations also fell broadly although less sharply and has have even lower queue standings (see table).

Amid these changes, expectations foresee inflation lower, interest rates, both short and long rates lower. There are across the board deeply negative expectations and largely reduced (but somewhat mixed and clearly weak) current assessments, stock market expectations are no HIGHER than their 1.7% percentile on a queue standing basis anywhere and that top reading is from the U.S. where stocks have been moving to record highs. Germany and euro area stock expectations have not had weaker readings on this timeline. Japan, the U.K., France, and Italy all post extreme weak readings.

Summing up

Clearly the ZEW experts continue to see a lot of chaos. Their view of the stock market is worrisome. Interest rates are low and seem to be heading lower while inflation readings remain depressed and are weakening. Central banks have little ammunition left to boost growth or inflation. The lingering trade war still seems to be eating away at the foundations for growth and there is more to come. But the trade-warring parties are still talking. In Europe, the new political arrangements in the EU are being sorted out. In the U.S. violent verbal clashes mark the political scene clashes of the sort that American politics has never seen in the post WWII period. There is still about one and one-half years to the next presidential election cycle. Iran is a major sticking point with Israel freshly accusing Europe of appeasement over its attempt to keep the clearly crumbling nuclear deal in place. Turkey is playing the ‘China Card' by drilling off the coast of Cyrus despite having only a ‘disputed right' to be there that no one else supports. Meanwhile, the Middle East and Straits of Hormuz are not safe but are being patrolled. Risks abound. Uncertainties lurk. Danger is clearly present. Why does the U.S. equity market love it all so?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief