Global| Jun 16 2020

Global| Jun 16 2020ZEW Expectations Jump But the Survey Continues to Point to Difficulties

Summary

The ZEW macroeconomic index 'improved' slightly in the EMU, rising to -89.6 in June from -95.0 in May. The gain on the month is small and the reading itself is still at an exceptionally weak mark. Germany improved to an -83.1 reading; [...]

The ZEW macroeconomic index 'improved' slightly in the EMU, rising to -89.6 in June from -95.0 in May. The gain on the month is small and the reading itself is still at an exceptionally weak mark. Germany improved to an -83.1 reading; the U.S. improved to a -90.4 reading. The rankings for all these readings are in their bottom 15% except for Japan that has a 25.7 percentile standing. Conditions remain weak…but...

The ZEW macroeconomic index 'improved' slightly in the EMU, rising to -89.6 in June from -95.0 in May. The gain on the month is small and the reading itself is still at an exceptionally weak mark. Germany improved to an -83.1 reading; the U.S. improved to a -90.4 reading. The rankings for all these readings are in their bottom 15% except for Japan that has a 25.7 percentile standing. Conditions remain weak…but...

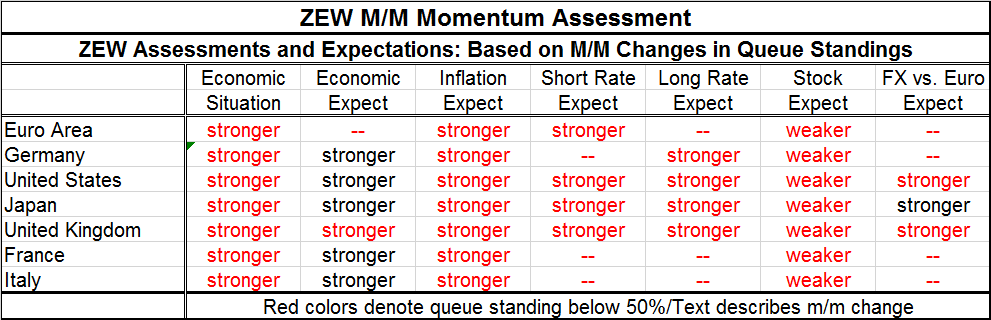

The table below shows the month-to-month change as a move that is either stronger or weaker and uses color coding to indicate values above (black) or below (red) the key value of 50% on a queue percentile standing basis (where 50% marks the historic median). The color-coding emphasizes that despite the rebound, and a proliferating of 'stronger' readings, even the broad move higher of the expectations readings leaves a lot of weakness in play. Economic expectations are broadly above their respective 50% mark, but most other readings remain below their, respective, 50% ranking markers which means they are below their historic medians as well.

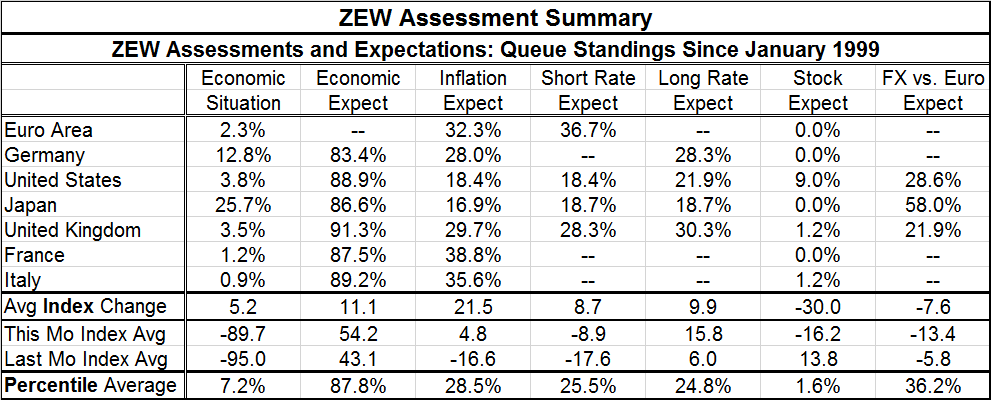

The table below gives the snapshot of the conditions across countries and the euro area; it provides the percentile standing values across a number of categories. The table shows that the average economic standing is up by 5.2 points in June, has a diffusion standing value of -89.7 and a 7.2 percentile average standing. While the economic standings improved broadly, they improved very little and remain severely impacted. That set of circumstances broadly marks this month's report: a broad improvement of small magnitude leaving conditions still quite weak.

Economic expectations averaged a change of +11 points in June with an average diffusion reading at 54.2; the average percentile standing is at its 87.8 percentile. This report is nearly the mirror image in strength of the weakness displayed in the current economy. It also stands alone in this regard on the month. These two gauges tell us broadly that economic conditions remain very weak but that the ZEW financial experts are quite upbeat on the future. The various local fiscal responses as well as the response of the ECB seem to have impressed the ZEW experts.

Inflation expectations are up and up rather strongly month-to-month with the average diffusion reading up 21.5 points month-to-month. And yet the percentile standing of the inflation gauge remains very low in its 28.5 percentile. Inflation expectations, despite the month's pop, have been lower less than 30% of the time. There is no inflation anxiety despite low interest rates and slug of stimulus.

Short- and long-term interest rate expectations are twins in their movements and standings. Both indexes rose by nearly 9 to 10 points on the month. Both have standings in the lower 30th percentile of their respective ranges. Their index diffusion values are different with short rates at a -8.9 level and long rates at a +15.8 level. But each of their values has roughly the same percentile standing in its respective queue of historic values.

The stock market is the 'odd man out' at this meeting as it has seen a net decline that averages a drop of 30 diffusion points month–to-month. In real time in the real world, of course, stock markets are performing extremely well and have been criticized for it. The ZEW experts have stock readings that average a -16.2 diffusion value and average a 1.6% percentile value for its standing.

On balance, the ZEW ratings of stocks seems a bit out of place and ZEW experts like many commentators in the U.S. seem miffed because markets have bet on recovery earlier than 'they' did and that economies are now showing a great deal of resilience. Market analysis seems torn between the reality that recovery is proceeding apace even with some restrictions still in place and the fear of a second wave that will swoop down and undermine everything. Clearly many feel that the market should not mark to the best recent economic data and should hold back because of the risk of that second wave-- a risk that grows as reopening progresses.

The U.S. is the center of the best new economic data as May showed a strong gain in jobs that appeared when a large decline was expected. Retail sales in May came back very strongly despite ongoing lockdowns in many areas and the June home builder index just shot up above its mean not just showing life but revealing actual growth and expansion.

In the ZEW framework, the average stock ranking is 1.6%, the current situation has an average ranking in the table of 7.2% and economic expectations have an average ranking of 87.8%. How do the ZEW experts square their stock pessimism with their buoyant economic optimism? The answer has to be that they are wary of the current level of equity valuations. Is this cold hard evaluation or is it sour grapes?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief