Global| Feb 17 2015

Global| Feb 17 2015ZEW Expectations Back on Top: Best in One Year

Summary

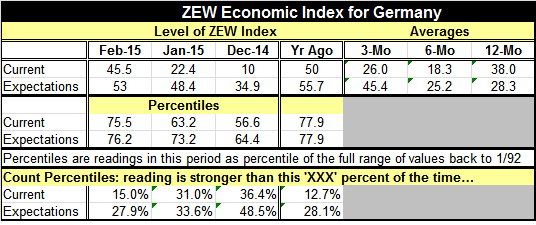

The ZEW financial experts' expectations index is back at its highest level in 12 months. Its percentile standing shows it is higher about 28% of the time while the current index, which advanced strongly to 45.5 from 22.4, is higher [...]

The ZEW financial experts' expectations index is back at its highest level in 12 months. Its percentile standing shows it is higher about 28% of the time while the current index, which advanced strongly to 45.5 from 22.4, is higher only 15% of the time.

The ZEW financial experts' expectations index is back at its highest level in 12 months. Its percentile standing shows it is higher about 28% of the time while the current index, which advanced strongly to 45.5 from 22.4, is higher only 15% of the time.

The dual ZEW readings form a strong basis for the German economy. The current index is higher only 15% of the time and expectations are better less than 30% of the time. That is a solid, if less than spectacular, pairing.

This situation has been `in the making' as the Bundesbank has hiked its outlook as did DIHK, the German Chamber of Commerce. The survey numbers themselves are, of course, the new face of reality, but the direction and acceleration is not a surprise. Most are talking about how the German economy has righted itself and how strong it is. But in 2014 when it was `struggling,' manufacturing set new marks for hours worked as well as for the number of people employed in manufacturing. That was in an `off year.' I can't tell you how many fellow EMU members would have killed for an `off-year' like that.

The German economy now is operating under a monetary framework that does not fit it either. The European Central Bank is trying like crazy to set a policy to revive the rest of Europe. But Germany has long been rigged like a German U-boat of old to run silent and deep and well. While the rest of the European economies have struggled, the German economy has been geared to perform without much fiscal or monetary help. It is an economy based on productivity gains and stocked with workers that are less than demanding on the wage front. German workers are willing to sacrifice gains to keep the corporate sector strong and to ensure that inflation stays at bay. Of course, it helped in the past few years that Germany had not developed the excesses of its fellow EMU nations and did not need to implement austerity programs when the others did.

But sanctions on Russia, a somewhat important German trade partner, did make some waves in the German economy. Like the rest of Europe, Germany also is hostage to Russian oil something that has lurked in the background and that undermines true confidence although that truly does not show up in surveys. It simply forces a different real politick on the German people as we saw when the U.S. tried - or thought out loud about - trying to arm Ukraine. Instead, Germany and France switched into overdrive to mount a peace deal one that is just not coming together.

But now with the ECB pulling out all the stops what we have is a European policy fit to try to stimulate a moribund euro area and to inject more life into an already rousing German economy. Europe's one-size-fits-none monetary policy- for once- does not suit Germany. Most articles do not present the German data that way. Instead they are looking on the bright side of strong German economic figures. And that is one view of Germany's reality. Another is that of a run-a-way vehicle gathering pace with insufficient braking power. Germany is being over-stimulated by the overly weak euro and and by overly low rates of interest and by the plan to stimulate more using QE. What onlookers miss is that `more' is not always good.

The mostly likely thing for Germany in the year ahead is to tighten fiscal policy. That means German domestic demand will not be geared to help the rest of the euro area. Germany will find its exports flying out the door as one of the most productive and efficient economies in the world. It already possesses a record current account surplus and a very high current account surplus relative to GDP. These metrics are going to gain even more notoriety. That means Germany will be trying to damp its growth by cooling domestic demand. Germany will be stimulated by its competiveness as it will suckle off the domestic demand in foreign nations using its economic strength then make its fiscal policy even more conservative to try to fight of the overstimulation of the German economy. In this mode, Germany will be taking more of exactly what the rest of the work needs (domestic demand. from others) and will providing less of it itself (as German fiscal contraction is likely to damp its own domestic demand). How can this result is good or balanced global polices? Already Germany's current account surplus is getting larger and the U.S. current account deficit is getting larger both of them boosted by exchange rate movements stimulated by domestic monetary policies gone to excess.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief