Global| Sep 17 2019

Global| Sep 17 2019ZEW Economic Expectations Largely Improve As Current Conditions Slip

Summary

Current assessments peaked around mid-2018, marking one of only four episodes of positive current assessments by ZEW experts since January 1999. Expectations had peaks just a bit earlier and have been falling steadily ever since. [...]

Current assessments peaked around mid-2018, marking one of only four episodes of positive current assessments by ZEW experts since January 1999. Expectations had peaks just a bit earlier and have been falling steadily ever since. There was a brief 'rebound' in expectations that reduced the slide in around mid-2019, but that rebound went away and was followed by new lower lows. Now, in September, there is another rebound in play that is seeing the macroeconomic expectations improve on a broad front as the table below shows.

Current assessments peaked around mid-2018, marking one of only four episodes of positive current assessments by ZEW experts since January 1999. Expectations had peaks just a bit earlier and have been falling steadily ever since. There was a brief 'rebound' in expectations that reduced the slide in around mid-2019, but that rebound went away and was followed by new lower lows. Now, in September, there is another rebound in play that is seeing the macroeconomic expectations improve on a broad front as the table below shows.

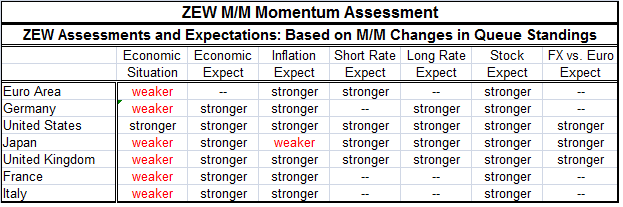

Economic expectations are stronger month-to-month for all countries/regions in the table. Inflation expectations are higher for all countries except for Japan. Rising inflation expectations are a good event since expectations and inflation globally have been so low. Inflation has been well below its targeted values in the United States, the EMU, and Japan. Unfortunately, Japan is an exception. Short-term and long-term interest rates are expected to be higher across the board. Stocks whose assessments remain very low also see improvement in their expectations month-to-month. The dollar, the yen and the pounds all are faring better on improved assessments month-to-month vs. the euro.

As ZEW survey participants were getting ready for this survey, the ECB was preparing for its new round of easing and it did deliver. That accounts for some of the rate expectations, the expected weakness in the euro and probably for some improvement in the outlook for equities as well. In the U.S., the Fed has just shifted to an easing mode that accounts for the U.S. metrics. The Bank of Japan has been quiet but is impacted by all these same forces. Meanwhile, the Bank of England is still struggling with Brexit.

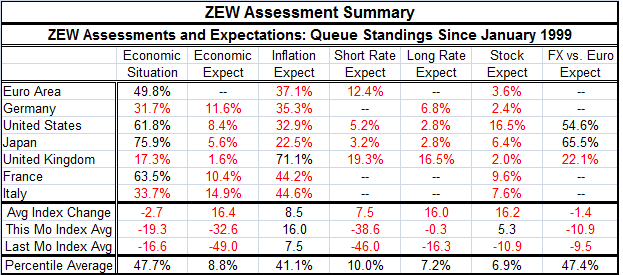

Table ZEW Assessment Summary table (below) shows the queue standings of the readings across regions. The information in this table is slightly different than Table ZEW M/M Momentum Assessment (above) since this table is a table of queue standings and the one above is bases on an assessment of CHANGES in queue standings. So this table is about the outright level of activity assessment while the one above is about momentum. Red values in this table are code for diffusion values below 50, which are indicators of activity less than its median pace (not just fading month-to-month. The latter being a momentum assessment).

The table's red-black coding shows clearly that the whole of the euro area, the U.S., Japan and France continue to show expansion at above its median pace (economic situation>50%). In contrast, Italy, Germany and the U.K. are not just showing shortfalls but showing substantial shortfalls. The columns on economic expectations show very weak values too, despite an average pick up month-to-month of 16.4 diffusion points (bottom panel of the table). The average diffusion reading 'rose' to -32.6 from -49.0, but the queue percentile reading average is still only 8.8%. That means that the individual member readings have been weaker on average less than 10% of the time. Because the net diffusion readings are negative, it means that expectations also are falling.

Inflation expectations are falling and below neutral everywhere except in the U.K. where Brexit pressures continue to foment. France and Italy have percentile standings that are relatively close to breakeven (inflation neutrality) as queue standings are in their respective 44th percentiles. The weakest inflation pressures are in Japan followed by the U.S. and then Germany.

Short- and long-term inflation expectations are extremely low and this is despite sizeable month-to-month gains in diffusion readings (+7.5 diffusion points for short rates and +16.0 diffusion points for long rates). Stock market expectations are improved across the board but with very low historic standings, again, despite month-to-month improvement.

Finally, the euro exchange rate has a queue standing above 50% vs. the dollar and yen indicating improvements for those two currencies vs. euro. But the pound is expected so sink vs. euro not just fall.

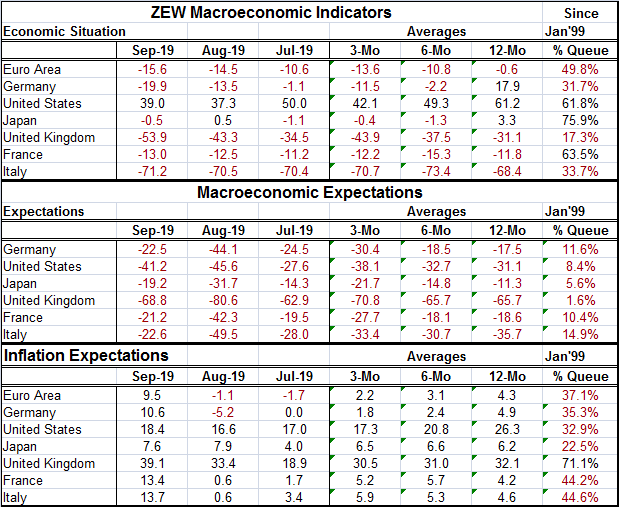

The table below shows the diffusion values and some recent progressions as well as the queue-standing metrics in the far right hand column. Negative diffusion readings imply more down than up responses have been submitted. The queue standings are not formally reflective of that and instead position the month's topical diffusion reading in a queue of historic values expressed as a percentage standing in which a value of 50% on the queue standing indicates the median value of the survey response. Compared to diffusion data from January 1999, the economic situation has been weaker than -15.9 almost half the time as it has a queue standing 49.8%. Since the queue standing is at its median at a value of 50%, this underscores how weak the ZEW experts have found the EMU over this period. There are only three substantial (four in all) periods in which the current assessment index has been positive in this period. One of them peaked in September 2000 at a diffusion value 54.6. Another in June 2007 at a diffusion value of 86.0. In May 2011, there was a modest short-lived positive reading at a diffusion value of 13.6. Then in April of 2018, there was a peak diffusion value at 57.7. The current values were negative 68% of the time over this period. ZEW survey participants have been negative on the current assessment of the EMU for a very long time. Despite this month's minor improvement, negativity remains as the overarching feature of the survey.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief