Global| Oct 15 2019

Global| Oct 15 2019ZEW Assessments of Conditions and Growth Remain Weak and Troubling

Summary

Growth is precarious; don't be nefarious ZEW experts are only one group with a negative and cautionary outlook. In its annual report, the IMF blamed the global slowdown on (1) trade fights, (2) Brexit uncertainty, and (3) other [...]

Growth is precarious; don't be nefarious

Growth is precarious; don't be nefarious

ZEW experts are only one group with a negative and cautionary outlook. In its annual report, the IMF blamed the global slowdown on (1) trade fights, (2) Brexit uncertainty, and (3) other geopolitical crises. The Remedy? It said there is an "urgent" need for leaders to de-escalate tensions. The IMF's over-arching banner statement of conditions declares that "The global outlook remains precarious." At only 3% global growth the IMF says “there is no room for policy mistakes.” It might have added that there are many fewer policy options (and some that are barely effective) left in the hands of policymakers. Past rate cuts leave global interest rate levels low and past debt profligance has left debt levels too high, perhaps taking many potential fiscal actions off the table. These conditions and circumstances suggest that the most effective pro-growth strategy now might be to try to remove the negative impulses rather than to try to mitigate them with policy moves of dubious value.

How do we handicap the chances of mitigation?

There has been some good news on the Brexit front and there may even be a viable, acceptable, path to an exit for the United Kingdom that is not a hard landing. But that is still a maybe. The United States and China had a trade meeting that ended with a deal… or did it? Well, the U.S. called it a deal China has not. And China says it needs more 'something' before it will actually sign it even though the U.S. ended the meeting with the clear understanding that the U.S. and China had a clear understanding, even though only a partial one. Treasury Secretary Steven Mnuchin has just said that if the China does not actually SIGN the agreement by December 15, the next round of U.S. tariffs WILL go into effect (Story here). So the U.S.-China trade news might be so good after all. As for all things geopolitical, well...Fuuggedddhabouddit! Tensions in various global hot spots are entrenched from Hong Kong to North Korea to the South China Sea to the Middle East which has become especially hot on Turkey's new madcap dash to kill Kurds, after crossing the border to Syria (we used to call such incursions an 'act of war'). And of course, Iran is still a major loose-end and Venezuela is a basket-case; South Korea and Japan are at loggerheads and so on. We sweep all that under the rug under the rubric of 'geopolitical.' But it's not all the same lump. Some of these are conditions that exist and have been lived with and others are in the midst of a dangerous escalation. I'd put Turkey and Iran in that 'lump' along with Hong Kong. Hong Kong might even be a Black Swann.

Table 1: Momentum Assessor

Apart from the growing geopolitical cancer, how is the economy doing?

Table 1 and Chart at the top of this discussion show that global macroeconomic expectations as assessed by the ZEW experts are still poor and largely deteriorating despite assessments that are in some cases already close to dire. The table shows that conditions are weak (red text flags queue standings below their median values) and weakening (see the label in the table) for most measures in most countries.

Table 2 below presents some key country recent observations on prime macroeconomic data and time series trend assessments along with the current queue standings (far right column) for the countries and variables.

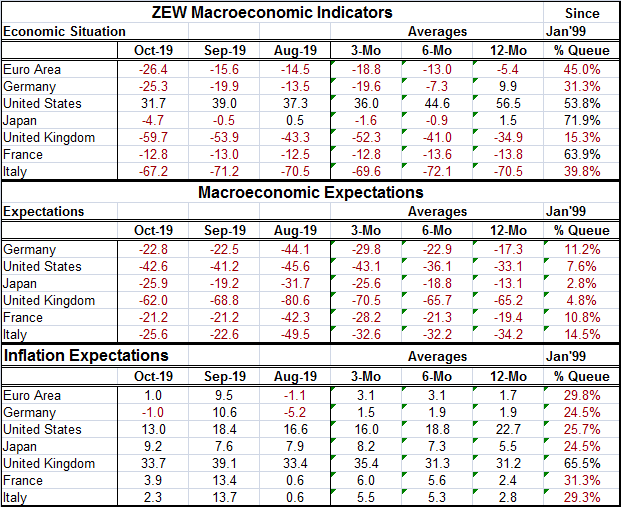

In the top segment of this three-panel table is the current situation (called the economic situation). Conditions have deteriorated in all countries month-to-month except France and Italy. Only the U.S. (the lone black value in the top panel) has a net positive assessment. On this set of panels, red values flag net negative diffusion values. Note the proliferation of red values; only U.S. still has net a positive assessment for the current situation; the U.S. assessment is black on all horizon (Germany and Japan are black for their respective 12-month averages). The average month-to-month current assessment fell by 4.2 points this month. This represents a step up in the pace of erosion as the average drop last month was -2.7 and the average over three months (compared to the six-month average) is -1.7 per month. The queue standings are below-median for the euro area, Germany, the U.K. and Italy.

The second panel is for economic expectations; these values are plotted in the graph. Expectations are red; they are net negative readings and their queue values are well below their medians and for the most part challenging the all-time lows made since early-1999. The U.K. is stronger month-to-month and the French assessment is unchanged. But conditions worsened elsewhere. Despite the dour assessments only the U.S., Japan and France have seen expectations worsen compared to their values 12-months ago (note: do not compare October to the 12-month average). However, all the three-month averages are weaker than their corresponding six-month averages; the loss in momentum is still driving the trend lower. The chart reveals some waffling in the monthly path but also clearly shows the broader trend to weaker readings.

The third panel is for inflation expectations. These values are largely positive, indicating that some pick up is expected; disinflation/deflation is not expected. Still, the queue standings underscore that there are still weak readings on inflation. The U.K. at a 65th percentile queue standing is the lone reading above its median. Among the rest, all but France are below their 30th percentile and France is not much of an exception to that observation with a queue standing at 31.3%. We can split hairs on trends here which are a bit more convoluted, but the clear message is that inflation is not a problem...unless it's too low.

Expectations for short-term interest rate declines mushroomed in July and August of this year. But in September, there was a reversal as rate cuts were less widely expected. In October, the outlook for short-term rate cuts is again diminished. The outlook for a long-term rate decline had swelled in July and August. But that enthusiasm waned with the outlook swing from net negative readings in August to net positive readings everywhere except in the U.S. In October, the outlook for long-term rates has firmed again this time across the board (the U.S. is still a net negative, but less than it was in September).

Without going into detail, stock market expectations give low largely net positive diffusion readings. The exceptions are net negative readings for the U.K. and for Italy. But all the queue standings are in their bottom 7 percentile historically or lower. The U.K. reading is now the lowest on record.

Table 2: Key Member Macro Assessments

The ZEW experts continue to see very weak conditions and there is not much encouraging in their outlook. However, this is not the low point in this cycle. The low point of expectations in this cycle came in August of this year and the ZEW expectations have generally improved from that with a bounce in September and more or less on hold on those readings in October. However, current conditions assessments are still worsening and are on their worst recent readings except for Italy that bottomed in March and France that bottomed in April. Inflation expectations are low and essentially the same range since April which marked a revival (of sorts) in inflation expectations. Expectations had collapsed in January and February in the wake of the Federal Reserve's December rate hike. Short-term interest rate expectations have been consistently low and negative since July of this year with long-term expectations negative or low since June or July depending on the country. This month's ZEW survey essentially marks time and does not seem to introduce any new direction or new fears or to represent any changed optimism. The ZEW experts seem to be marking time with a weak outlook.

Table 3: Zew assessments: The specifics

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief