Global| Nov 10 2020

Global| Nov 10 2020ZEW: A Mixed Month at a Mixed-up Time

Summary

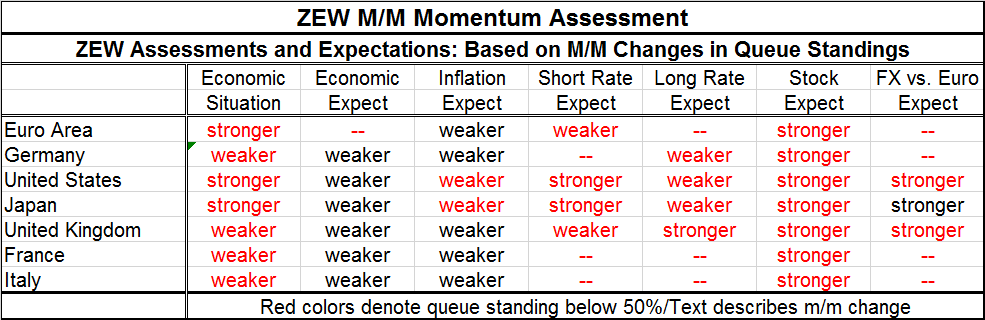

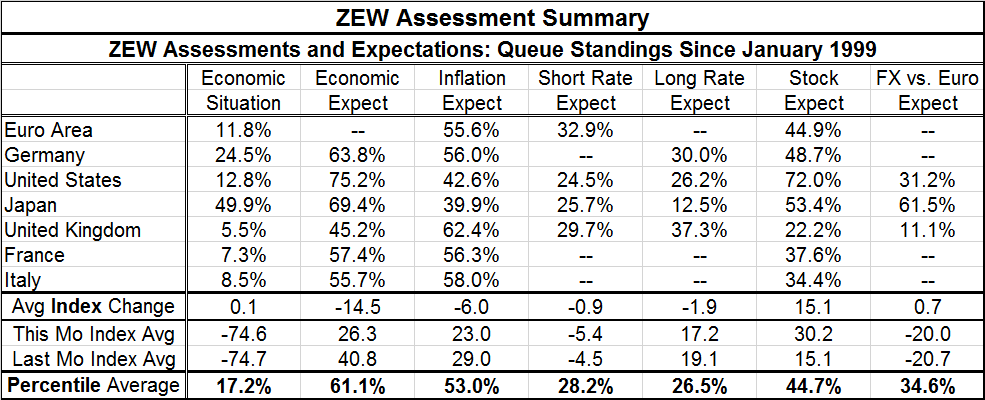

The economic situation is evaluated by the ZEW experts as a mixed situation in November. Expectations are not as fragmented and are viewed as weaker across the board. Inflation expectations are weaker everywhere as well. Interest rate [...]

The economic situation is evaluated by the ZEW experts as a mixed situation in November. Expectations are not as fragmented and are viewed as weaker across the board. Inflation expectations are weaker everywhere as well. Interest rate expectations are somewhat mixed, but the stock market is expected to improve across the board. What makes this situation ‘mixed-up’ is the Pfizer announcement yesterday that its tests show its vaccine to be 90% effective against Covid-19. On that news, stocks spiked yesterday (losing some of their gains today) and bond yields elevated. That one-day piece of news dramatically altered the landscape and may also obviate some of the ZEW assessments that we summarize here. Of course, markets reacted with a knee-jerk response. In reality even if that 90% assessment is correct, it will still take time to manufacture, roll out and inoculate all who seek it. So while the Pfizer announcement event was a watershed of sorts, it will still play out over time and is not an instantaneous game-changer. But if it holds up, it is a game changer assuming it goes over all the safety hurdles. The three key issues for a vaccine are effectiveness, the breadth of effectiveness, and safety of usage.

The economic situation is evaluated by the ZEW experts as a mixed situation in November. Expectations are not as fragmented and are viewed as weaker across the board. Inflation expectations are weaker everywhere as well. Interest rate expectations are somewhat mixed, but the stock market is expected to improve across the board. What makes this situation ‘mixed-up’ is the Pfizer announcement yesterday that its tests show its vaccine to be 90% effective against Covid-19. On that news, stocks spiked yesterday (losing some of their gains today) and bond yields elevated. That one-day piece of news dramatically altered the landscape and may also obviate some of the ZEW assessments that we summarize here. Of course, markets reacted with a knee-jerk response. In reality even if that 90% assessment is correct, it will still take time to manufacture, roll out and inoculate all who seek it. So while the Pfizer announcement event was a watershed of sorts, it will still play out over time and is not an instantaneous game-changer. But if it holds up, it is a game changer assuming it goes over all the safety hurdles. The three key issues for a vaccine are effectiveness, the breadth of effectiveness, and safety of usage.

Setting aside the issue of a vaccine we see the numerical assessments and the scattered pull-back in current assessments that is not widespread enough to push the average change lower. On the month, the German situation deteriorated by about 5 points while the U.S. situation improved by about 5 points. Japan improved by more. The U.K., France and Italy all deteriorated by small amounts leaving the net hang as a very small positive number. However, all the percentile standings on the month remain low. With only Japan essentially at its median value.

Macroeconomic expectations changed more uniformly with all assessments cut on the month, driving the average change to -14.5 diffusion points. Expectations for the European countries moved sharply lower on the spreading coronavirus. The U.S. and Japan moved lower too but not as dramatically the U.K. fell, posting an outright negative value. The average percentile assessment fell to its 61st percentile, but only the UK was below its median diffusion assessment as it continues to negotiate terms of its Brexit with the EU and fights a spreading virus as well.

Inflation expectations fell across the board along with the mixed economic conditions and reduced expectations. The U.K., France and Italy observe a generally a larger negative inflation impact. The average change for inflation expectations is a drop of 6 points on the month. The average percentile standing is at 53%, indicating essentially normal inflation expectations.

In step with the reduced economic expectations, and reduced expectations for inflation, the short-term and longer-term interest rate expectations also are slightly lower on the month although are also somewhat mixed. The average index change is small, but the percentile standings for the two series are both between the bottom one-quarter and bottom one-third of their historic ranges of value. In this environment, the average 15 diffusion point rise in stocks and the average 44.7 percentile standing are indications of an oversold condition and of markets expecting that it will be correcting itself.

On the whole, the economic situation is assessed as very weak. Yet, economic expectations are only modestly above their historic medians (a 61st percentile average standing). Inflation is not an issue with a near normal median reading at a 53rd percentile standing. Policy (short-term) and market-determined (long-term) interest rates are both exceptionally low. In this environment, some recovery and stock market pick up is expected. We saw a hint of that yesterday when the early vaccine result from Pfizer was announced. Markets are waiting on what they expect will be eventually good news. That is one of the reasons that the news of the spreading virus does not hit stocks harder. There is an overarching assumption that however bad the virus might get we will survive it and economies will eventually get back to business. Virtually no one is betting on the virus.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief