Global| Nov 13 2015

Global| Nov 13 2015Year-over-Year EMU GDP Shows Some Recovery

Summary

EMU shows year-over-year GDP in a ramp up in growth to 1.6% in Q3 from 1.5% in Q2 and 1.2% in Q1. Yet, five of ten EMU member in the table saw year-over-year GDP growth decelerate in Q3 from Q2; only The Netherlands decelerated in Q2. [...]

EMU shows year-over-year GDP in a ramp up in growth to 1.6% in Q3 from 1.5% in Q2 and 1.2% in Q1. Yet, five of ten EMU member in the table saw year-over-year GDP growth decelerate in Q3 from Q2; only The Netherlands decelerated in Q2.

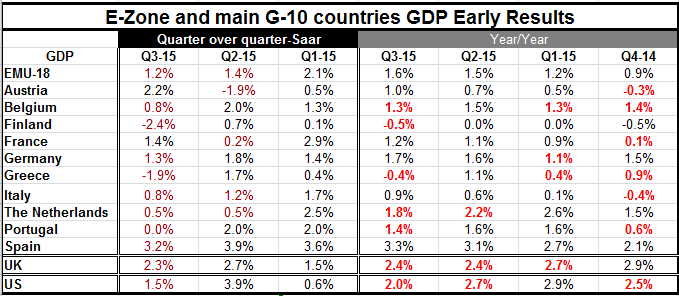

EMU shows year-over-year GDP in a ramp up in growth to 1.6% in Q3 from 1.5% in Q2 and 1.2% in Q1. Yet, five of ten EMU member in the table saw year-over-year GDP growth decelerate in Q3 from Q2; only The Netherlands decelerated in Q2.

In Q3 annualized quarterly growth in GDP posted declines in Finland and in Greece. GDP was flat in Portugal. It rose by less than 1% (annualized) in Belgium, Italy, and The Netherlands. These are six underperforming economies.

Top-rated growth comes from Spain at a quarterly pace of 3.2%. Austria is next strongest with just 2.2% growth; after that it is France, at 1.4%, and Germany, at 1.3%. Impressive growth rates are few and far between.

Year-over-year GDP managed to accelerate in five members in the table but the accelerations were mostly minor while most of the decelerations were significant.

Two of the fastest growth EMU economies Spain (the fastest) and Portugal (the fourth fastest) have political problems to deal with. Spain is fighting an independence movement from Catalan that has become more aggressive. Portugal is fighting a revolt from the left that wants to end adherence to austerity and possibly leave EMU altogether. These are serious problems that could interrupt what have been improving growth stories. While Spain still shows strong quarterly growth in Q3, Portugal's quarterly growth already has gone flat.

The growth figures for EMU and most of its members are disappointing. Already attention is being directed to the ECB and its potential to act. However, Mario Draghi's reference comments have been aimed at boosting inflation not at growth. Inflation is the ECB's only mandate. If the next inflation report in late November does not show further inflation weakness the ECB may not feel so pressured to act even if economic growth remains moribund.

Bond yields in Europe already have moved lower in anticipation that the ECB is going to do more asset accumulation and on the assumption that it will be buying sovereign debt as well. The ECB buying sovereign debt is a very controversial plan with the Germans adamantly opposed to it, seeing it as a breach of the Treaty stipulation that the ECB not meddle in member nations' fiscal affairs. Yet, markets are expecting it.

The slowdown in the Euro-Area growth is one that represents a forecast miss by the ECB itself. Yet the gain and acceleration in the year-over-year rate of growth of GDP reminds us that, as forecast disappointments go, this one is a small one. Still, the growth slowdown does put the ECB on notice at least in a political sense and does so as inflation is undershooting whether it worsens in November or not. The ECB still has plenty of reasons to try for more stimulus... if it wants to. The ECB mandate is only to reach and maintain inflation just below 2%- not near zero. So inflation will remain the ECB's titular focus. There is however, no doubt that this weaker than expected GDP report will ratchet up pressures on the ECB whether it wants to acknowledge it or not.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief