Global| Nov 19 2014

Global| Nov 19 2014What's Wrong with this Picture?

Summary

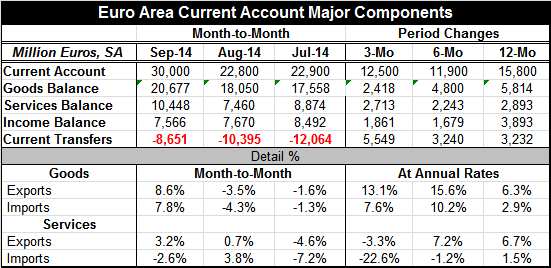

The EMU current account surplus rose to 30 billion euros in September form 22.8 billion euros in August. The EMU trade surplus increased. The balance on services trade moved to a larger surplus and the income account's surplus was [...]

The EMU current account surplus rose to 30 billion euros in September form 22.8 billion euros in August. The EMU trade surplus increased. The balance on services trade moved to a larger surplus and the income account's surplus was roughly unchanged. Current transfers, which comprise net out-payments, receded.

The EMU current account surplus rose to 30 billion euros in September form 22.8 billion euros in August. The EMU trade surplus increased. The balance on services trade moved to a larger surplus and the income account's surplus was roughly unchanged. Current transfers, which comprise net out-payments, receded.

On balance, the European Monetary Union's current account improved and its components improved up and down the line. Yet, the area's exchange rate, the foreign exchange value of the euro, has continued to slip. Why is the currency value slipping for a region that is logging the largest current account surplus in the world relative to GDP?

The chart above displays a long plot of the synthetic euro trade weighted (effective) exchange rate in real terms. It is synthetic because it uses the proper currency rates to reconstruct what the euro value would have been prior to the formation of the EMU. That allows us to take the time-series back farther in time. It is plotted against its average for the period. This line evaluates the euro area's nominal exchange rate trade weighted and adjusted for inflation differences between the EMU and its trade partners. When the real exchange rate is above its average, it indicates some overvaluation (a nominal euro valuation delated for price differences that is strong relative to its history). When the PPP measure slips below its average, the nominal euro is too weak.

Purchasing power parity (PPP) is what is being measured by the real effective exchange rate chart at the top. This is a concept that has long been used to evaluate exchange rates. It is a simple back-of-the-envelope approach that John Maynard Keynes endorsed. He not only was a great economist, but he used to make profits speculating in foreign exchange markets.

The notion of PPP is that markets should get the value of currency `right' over time. That means that the mean of the real effective exchange rate will be an estimator of its true value, a value for which the currency rate offsets past differences in inflation. PPP is a convenient and simple calculation but look at what is happening in the euro area right now.

The euro has been falling. We can see in the PPP chart that the real effective euro is dropping. The (nominal) euro is falling faster than its inflation differential with its trade partners. And the euro is still above its mean, the PPP estimator. So far this seems like all is well. The euro is headed back toward what we would consider as its true parity.

The problem is that the euro area current account surplus is massive! That surplus which continued to grow when PPP said that the euro was overvalued tells us that the euro is in fact undervalued! So why is the euro area, a place that already has the highest current account and trade surplus in the world relative to its GDP, depreciating its currency so that its surplus will grow even larger?

Similarly, we could notice that the dollar is rising in value while the U.S. has a huge current account deficit relative to its GDP. And the rising dollar will make that deficit worse!

Obviously, currency rates are not moving in a direction to cure the current account imbalances. Instead since the U.S. economy is doing relatively well the dollar is rising and to boost a sagging Europe the euro is falling (just as the yen is falling to boost a sagging Japan).The fact that currency rates are making international imbalances worse is a symptom of our times. That PPP and current account imbalances tell such a different story is a symptom of economic policies gone awry.

Current account imbalances and capital flows imbalances are being made worse too. Arguably these out of kilter capital flows were one of the main forces behind the last financial crises, as they distort the price of capital. We should beware of such developments. If we view the foreign exchange rate as medicine for the economy, medicine should not make the economy sicker. But it is.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief